Sustainability in Europe has entered a new phase. Across the base oils and lubricants industry, the conversation has matured beyond high-level targets and regulatory frameworks. The real challenge now lies in execution, and at the center of that challenge sits lifecycle data.

Sustainability is a Business Topic

Recent market developments show how strongly sustainability has moved into strategic decision-making. What was once treated mainly as a compliance topic is increasingly linked to resilience, customer expectations and long-term business performance.

This shift is also reflected in Deloitte’s 2025 C-Suite Sustainability Report. Even as stakeholder pressure has eased, 83% of executives report increasing their sustainability investments, up from 75% in 2023. Meanwhile, 66% are already seeing positive impacts on revenue, up from 52%. Sustainability, in other words, is no longer just a compliance obligation. It has become a driver of business performance.

Once sustainability is treated as a strategic priority at the executive level, it begins to shape operational decisions and create concrete expectations along the value chain. Climate targets and reporting commitments are translated into supplier requirements, and sustainability pressure moves from corporate strategy into procurement and then upstream into Tier-1 and Tier-2 suppliers.

When these expectations reach the supply chain, they usually come in two forms. First, the demand for transparency. Suppliers are asked to provide product carbon footprints, life cycle assessments and data that support corporate sustainability reporting. Second, the demand for reduction. Suppliers are expected not only to report emissions but also to show credible targets and measurable progress over time.

For lubricants and greases, this means lubricant suppliers often sit directly in this Tier-1 position. They are expected to support customer reporting and reduction targets while relying heavily on upstream data themselves. This is where lifecycle data stops being only a reporting topic and becomes an operational challenge.

When regulation meets operational reality

Inside lubricant supplier organizations, the pressure coming from customers and regulators rarely arrives as one clear, harmonized requirement. Instead, it comes through a growing number of parallel requests: product carbon footprints, corporate sustainability disclosures, customer-specific emissions data requests, recycled-content declarations, digital product information and the substantiation of environmental claims.

Many of these requirements follow different methodologies, system logics and timelines. In practice, companies often prioritize the request with the most immediate business or regulatory relevance. This is understandable from an operational perspective, but it also highlights the need for data structures that can work across multiple frameworks.

This is why primary unit-process data matters so much. A robust internal data foundation connects operational reality with external reporting needs. If unit-process data is clean, structured and reusable, companies can respond more efficiently to changing methodologies and disclosure requirements. While rules may continue to evolve, a strong data foundation remains the basis for consistent adaptation.

Just as importantly, clean primary unit-process data connects internal operations with the upstream supply chain.

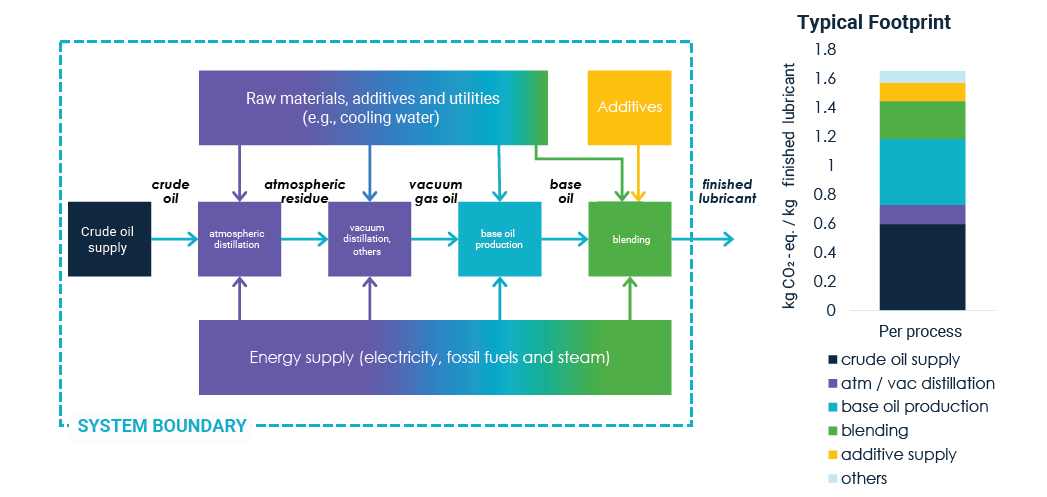

Figure 1. Calculating Lubricant Cradle-to-gate Product Carbon Footprint

Source: Carbon Minds

Relevance of Supply-Chain Emissions in Product Carbon Footprints

This becomes especially important when looking at the emission profile of lubricants in product carbon footprints for customer reporting. For many lubricants, the dominant share of the carbon footprint sits upstream rather than in blending operations, site energy use or other on-site activities. This means that even if internal data is well organized, robust PCFs still depend primarily on supply-chain emissions.

At the same time, detailed information on supply-chain emissions does more than improve reporting credibility. It also helps companies identify optimization opportunities in sourcing and reduce the impact of their products.

In other words, a large share of the footprint sits outside the direct operational control of the lubricant manufacturer. This changes the nature of carbon transparency in the sector. If most emissions come from upstream, and therefore lie outside direct control, how can lubricant suppliers provide credible carbon data, especially when regulatory requirements and methodologies continue to evolve?

From Complexity to Credibility in Supply-Chain Emissions Data

This question is difficult to answer in practice because upstream complexity starts at the crude oil level. Crude oils differ significantly in properties such as API gravity, sulfur content and composition. These physical differences translate into different energy requirements and emission profiles during exploration and refining. As a result, baseline emissions can vary substantially from the outset.

This complexity continues at the base oil level. Base oil footprints depend not only on base oil group but also on feedstock, energy supply and processing configuration. Even within the same base oil group, emission ranges can overlap significantly. This makes simple technology-based assumptions unreliable for robust carbon reporting and decision-making.

Regionalization adds another layer of complexity across the upstream system. Feedstocks, energy mixes, process conditions and transport distances can differ significantly by region, resulting in different upstream emissions even for similar products. Regionalization is therefore not a minor detail. It often defines the starting point of the carbon profile and strongly influences how useful the data is for decision-making. Without regionalized data, companies risk working with baselines that may be formally compliant but less representative in practice.

This is also where the answer to the earlier question begins to emerge. Credible carbon data depends on using the most specific upstream data available: supplier-specific datasets where possible and otherwise specific secondary data, such as highly regionalized and technology-specific datasets. Both come with trade-offs. Secondary data may not reflect the profile of a specific supplier but often provides greater consistency across the dataset. Supplier-specific data can be more representative, especially at Tier 1, but in practice it is often still a combination of primary supplier information and secondary background data, introducing different methodological approaches into the calculation.

This is why governance and consistency matter more than perfection. The goal is not perfect data in every case but a robust and transparent data foundation that makes carbon footprints credible, comparable and useful for decision-making.

Life Cycle Data for Pathways to Net Zero

Lifecycle data in lubricants is not relevant only for upstream transparency and product carbon footprints. The same data foundation also supports a broader question: how can lubricant suppliers identify credible pathways to net zero across the supply chain, use phase and end of life?

Upstream emissions are a critical part of the picture, but they are only one part. A credible path to net zero in lubricants also requires attention to circularity, the use phase and end of life. This matters because the sector’s contribution to decarbonization is shaped not only by the footprint of supplied materials but also by performance in application.

Circularity is one important pathway in this context. Rerefining can reduce supply-chain emissions by lowering demand for virgin base oils while helping to mitigate end-of-life emissions by keeping material in use longer.

Product performance is another essential pathway. Lubricants can contribute to sustainability goals through efficiency gains, extended service intervals, equipment protection and other use-phase benefits. At the same time, capturing this contribution is not straightforward from a lifecycle data perspective. Once the focus shifts downstream, the picture becomes more complex. Use-phase effects depend on the specific application, operating conditions, product lifetime, maintenance patterns and the methodological rules used to account for avoided or reduced emissions.

This means a credible sustainability strategy in the sector should connect three perspectives: robust upstream lifecycle data, circularity and end-of-life thinking and a clear understanding of performance-driven value in application.

What This Means in Practice

So what does this mean for lubricant suppliers in practice?

It means building a lifecycle data foundation that is robust enough to serve several purposes at once: supporting evolving disclosure requirements, improving the credibility of product carbon footprints, identifying better upstream decisions and enabling broader net-zero pathways across the supply chain, use phase and end of life.

In practice, this requires clean and structured unit-process data internally, the most specific upstream data available and a perspective that extends beyond upstream emissions alone. It also requires governance over perfection. In a fast-evolving environment, consistency, transparency and scalability are often more valuable than one-off precision.

With this foundation, lubricant suppliers can move beyond reactive compliance. They gain the ability to adapt to evolving requirements while maintaining credibility in both their carbon data and their sustainability strategies.

Ultimately, lifecycle data is no longer a background detail. It is the infrastructure that underpins meaningful decision-making in the transition to net zero. For Europe’s base oils and lubricants sector, progress will depend not only on setting ambitious targets but also on building the data systems capable of delivering them.