Still Holding Our Breath

Despite initial optimism that ongoing negotiations would bring an end to the United States-Israel-Iran war and the reopening of the crucial Strait of Hormuz, no conclusive agreement had been achieved by early June. Hopes were quickly shattered when it became apparent that the U.S. and Iran would be unable to agree on several terms, and both countries launched renewed attacks on military and telecommunications facilities in the Middle East.

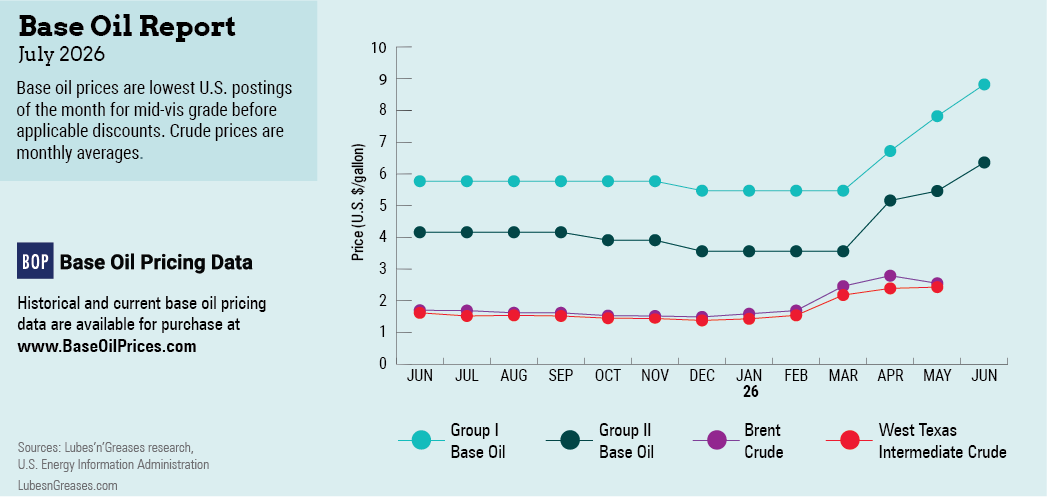

Not surprisingly, base oil prices remained exposed to upward pressure from soaring crude oil prices as oil flows from the Persian Gulf remained constrained. Posted price increase announcements from base oil producers had emerged in the U.S. almost on a weekly basis since the beginning of the war on February 28. However, by early June, it appeared that the pace of adjustments had slowed. Participants speculated that this was because base oil values had peaked and buyers seemed unable to absorb further markups. Suppliers were worried about demand destruction as some blenders reduced purchases and a few even considered temporarily idling operations because they faced credit limitations that prevented them from acquiring additional base oils.

Despite tempered demand from some segments, most base oils remained in tight supply. The API Group III category showed the most blatant market imbalance as supplies from the Middle East were trapped in the Persian Gulf and a couple of plants shut down production after suffering Iranian drone attacks. Asian and North American supplies were not sufficient to fill the gap left by the absence of Middle East products.

In response to the rapid increase in the price of base oils, additives, packaging and transportation, lubricant manufacturers communicated lubricant and grease price increases to offset the mounting production costs. Suppliers reported robust lubricant consumption, inventory building and reduced buyer resistance to the increases, which could be partly attributed to concerns about potential shortages and even higher prices in the coming months.

While the arrival of the summer driving season typically signals an increase in base oils and lubricant consumption, the rising price of both fuels and finished lubricants coupled with inflation, cash flow constraints and economic uncertainties led to more limited consumer spending and reduced automotive maintenance. Independent repair shops, dealerships, and parts suppliers reported signs that consumers were postponing preventative maintenance, including oil changes, to cope with tighter household budgets, according to several media outlets.

The maintenance slowdown was somewhat exacerbated by supply restrictions affecting parts and fluids, particularly synthetic engine oils. Some automakers warned dealerships and service centers about shortages involving specific service materials. Toyota and Nissan were heard to have issued letters indicating that supplies of 0W-8, 0W-16 and 0W-20 motor oils were becoming strained as they require Group III in their formulations.

The tight Group II and Group III base oil supply might be exacerbated in the U.S. by a plant turnaround scheduled to start at Chevron’s Pascagoula, Mississippi, Group II/Group III plant in June.

The longer the conflict in Iran remains unresolved, the more dire the situation for Group III buyers in the U.S., as close to 44% of Group III supplies originate in the Middle East. Only ADNOC was understood to be able to ship isotank-sized cargoes of base oils from ports on the Red Sea.

The balance of supplies in the U.S. typically comes from Asia and Canada, but Asian refiners had reduced output due to curbed refinery production rates triggered by a lack of Middle East crude oil shipments. Some refineries were also required to prioritize fuel production over that of other refined products to protect fuel supplies for the general population. However, the situation appeared to be gradually improving as several Asian countries tapped into strategic emergency crude stocks, or imported crude oil from alternative sources. A key South Korean supplier was heard to be able to continue running well and produce base oils to fully meet contract commitments as it has diversified its crude sources over the last few years.

Additional Group III volumes might be moving to the U.S. from South Korea in the coming months, but the additional shipments might take several weeks to arrive.

Meanwhile, domestic Group III producers were trying to run plants at close to full rates to meet contract obligations, with expectations that those Group II producers who can also manufacture Group III base oils would increase production to cover some of the current supply gaps and take advantage of the elevated Group III prices.

On the naphthenic base oils front, prices were mostly stable, following several increases since March, although there continued to be upward pressure due to steep crude oil prices and a tight supply and demand balance, particularly of the light grades. The heavy grades have seen improved demand with the start of the summer driving season, with more consumption coming from the rubber, tire and grease segments.

Some base oil postings have almost doubled since the beginning of the Iran conflict, but there were signs that they may have reached a ceiling. However, if the war remains unresolved and the global crude supply situation worsens, then oil futures could climb further and base oil producers may have to reassess their pricing strategies. Even if the critical strait were reopened tomorrow, and crude oil and other refined products started to flow from the Persian Gulf again, it has become increasingly evident that the disruptions would persist for several months and continue placing pressure on prices. Industry insiders noted, however, that for many market participants, the main concern was not so much a matter of pricing, but of being able to secure enough raw materials to keep plants running.

Gabriela Wheeler is base oil editor for Lubes’n’Greases. Contact her at Gabriela@LubesnGreases.com