Seldom has it been clearer that supply chains in the lubricant industry are vulnerable to disruptions from geopolitical conflicts. But how did the industry become susceptible to the type and scale of turmoil now buffeting base oil markets? Consultant H. Ernest “Ernie” Henderson explores the question in a two-part series. Part 1 recounts the formation of API base oil base oil categories and the rise of merchant

base oil suppliers.

The conflict in the Middle East is an excellent example of the ramifications arising in geopolitics. These occur in many instances with little or no warning and can last for a brief to extended period.

It has become apparent that the Strait of Hormuz is a critical corridor for the movement of goods and services, particularly in the petroleum sector. From crude oil to liquefied natural gas, fertilizers to specialty products including lubricant base oils, the implications here are significant, and the end to this turmoil is still not in clear site.

To better understand the lubricants industry and the impact of geopolitics, one needs to go back to earlier times to see how the industry has evolved. In the 1980’s, many regions — like North America, including the United States — were self-sufficient in terms of base oil supply, demand and quality requirements. Lubricants themselves represent a recipe where base oils serve as the foundation or building block. They are then complimented with a variety of chemical additives whose role is to elevate the properties of the base oil to that required for the finished application.

During the ’80s and into the ’90s, performance requirements were somewhat stagnant with most automotive and industrial products dependent on solvent refined base oils and conventional additive packages. Synthetic products were unique and formulated specifically to operate under severe conditions. These were typically formulated with chemically synthesized base oils like polyalphaolefins and/or esters and contained a complimentary additive system. Solvent processing accounted for most of the paraffinic base oil production in North America, and domestic refiners met nearly all of domestic base oil demand.

However, during the 1980’s, the processing technologies used to manufacture base oils began to change in North America. Hydroprocessing was introduced by Chevron in Richmond, California, to replace solvent extraction, and later solvent dewaxing was added. Petro-Canada leveraged Gulf severe hydrocracking technology in Mississauga, Ontario, Canada, while Sunoco in Yabacoa, Puerto Rico, developed a combined technology approach using partial solvent extraction and mild hydrotreating. Sunoco’s technology approach was later advanced and introduced commercially by Exxon at its Baytown, Texas, refinery where it was called raffinate hydroconversion, or RHC. Pennzoil also introduced hydroprocessing technology during this period at its facility in Westlake, Louisiana.

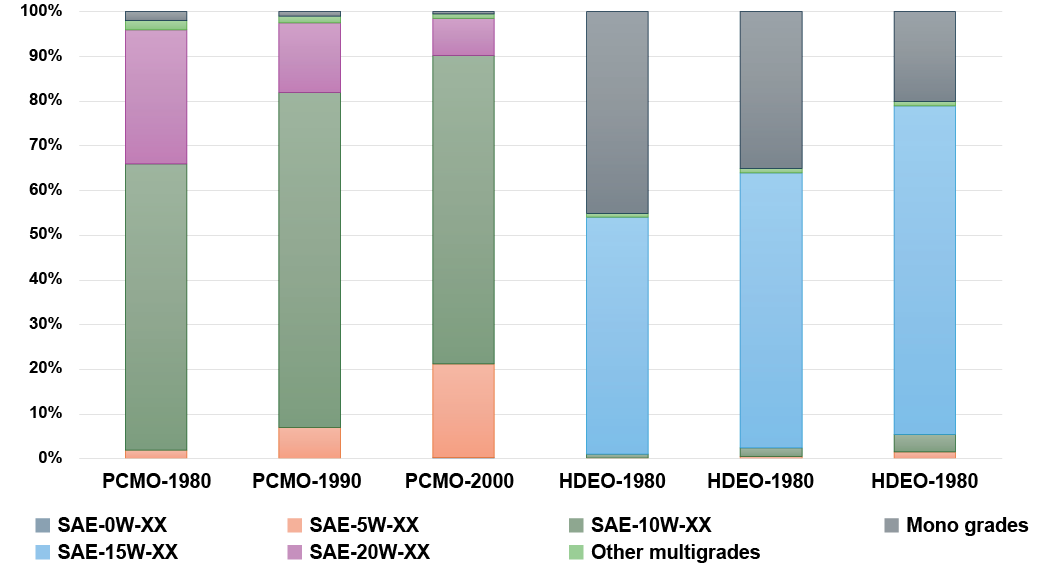

Figure 1. SAE Grade Profile of North American Automotive Engine Oils

These new hydroprocessed base oils were different in that they lacked color and odor and had very low levels of sulfur, which historically had been considered to provide a level of natural antioxidant performance, albeit less than chemically produced antioxidants additives. Automotive manufacturers were skeptical of these new “water-white” base oils delivering the required performance in finished engine oils to meet existing warranty claims. Accordingly, the American Petroleum Institute was asked to establish a set of engine-based protocols to ensure that lubricant formulations could be designed using either solvent refined or hydroprocessed base oils while maintaining consistent engine performance.

This was the framework for the API base oil groups and interchange guidelines where engine data combined with statistical analysis and technical judgement formed the basis for API 1509. This was reviewed and sanctioned by key stakeholders in the industry including but not limited to base oil manufacturers, additive companies, lubricant manufacturers and marketers, engine testing laboratories and original equipment manufacturers.

Definitions for API Group I and II base oil categories were developed in the early 1990s and initially published in 1992. A second updated release in 1995 by API included the introduction of the Group III category that exists today, along with Group IV for polyalphaolefins. Group III was not a major U.S. initiative from a manufacturing standpoint but was recognized in Europe as a new, higher viscosity index alternative to base oils normally produced by hydroprocessing.

Testing and analysis were conducted and reviewed by API and its key stakeholders to determine if these higher-VI hydroprocesed base oils were equivalent to PAO, which was normally marketed at a significant premium to conventional base oils. Although equivalency was not adequately demonstrated, API did recognize the performance differences between regular and higher-VI hydroprocessed base oils. This was the dawn of the Group III category.

During this period, North American refiners were focused on the production of lower VI hydroprocessed base oils as they provided higher yields from readily available crudes and were ideally suited for a changing automotive industry. Heavy-duty engine oils were transitioning from monogrades to multigrades, and the high yield of the medium-viscosity 220 neutral cut — the most produced cut in most cases — fit nicely with SAE 15W-40 formulation requirements. (See Figure 1.)

For passenger car engine oils, the market had yet to embrace ultra-low viscosity grades like SAE 0W-XX (except for a few specialty synthetic products) but was beginning to see increased demand for SAE 5W-30 grades. The typical base oil VI for an SAE 5W-30 engine oil is approximately 112 to 117 depending on additive technology used, and this fits nicely within the API Group II definition of 80 to 119 providing maximum use of Group II interchange rules. Companies like Exxon, Petro-Canada, Chevron and Motiva capitalized on this development, and the unofficial Group II+ category was created as a marketing tool primarily for Group II 110N oils with VI in the range of 110 to 119.

By the end of the 1990’s, the North American base oil industry was rapidly transitioning from solvent to hydroprocessing but was more focused on Group II than Group III. There was limited production in the region and relatively little demand for Group III oils, which required special feedstocks and/or processing adjustments. This would change, however, in the 21st century thanks to two important events.

The first was a 1999 ruling by the National Advertising Division of the U.S. Council of Better Business Bureaus that gave “synthetic” credibility to Group III base oils. The ruling came out of a case in which Mobil challenged Castrol’s use of Group III as a replacement to Group IV PAO in engine oils marketed as “synthetic.” The ruling allowed Group III based formulations to be marketed as synthetic, creating a new and lower cost marketing opportunity in the synthetic and semi-synthetic area for PCMO and HDEO products.

The second event was investment in the Far East by base oil manufacturers to produce large quantities of Group III for limited domestic demand and more importantly export opportunities. One of the target markets for the new production was North America, as it was considered to be deficient in Group III production capacity. Supply chain was the initial market entry obstacle as U.S. companies were not willing to purchase Group III cargoes from the Far East and manage the shipping and handling costs combined with the excess inventory from each purchased cargo. U.S. blenders were more accustomed to receiving on-time, on-spec deliveries while leaving it to suppliers like base oil producers to manage inventories and support costs. These stumbling blocks were eventually resolved, and the Far East quickly became a reliable supply source for Group III base oils into the North American marketplace. This was the birth of the merchant base oil marketer.

The applications for Group III grew rapidly during this period. The passenger car oils market required the highest VI and lowest kinematic viscosity base oil profile and became the major outlet for Group III base oils. Heavy-duty oils remained well suited for Group II, while industrial lubricants leveraged both Group I and Group II depending on performance needs, supply chain management and overall formulation costs. The low SAE 0W-XX passenger car grades had yet to appear in the marketplace to significant degree, but it was quickly realized that one could duplicate the Group II+ quality and VI required for SAE 5W-30 (and later SAE 5W-20) engine oils by blending Group III with Group II to Group II+ VI targets. This led to increasing interest and growing demand for Group III.

During the next two decades, investments in new base oil production capacity exploded, primarily in the Far East and the Middle East where distillate hydrocrackers leveraging Arab Light and similar crudes provided an ideal quality and inexpensive vacuum gas oil feedstock to produce hydroprocessed Group II and Group III base oils. North America did see one major project, by Chevron in Pascagoula, Mississippi, during this period, but this was designed for Group II quality as an export facility. Group III investment remained sparse regionally, although a few refiners converted Group II capacity to Group III at the expense of yield, throughput and product cost. This created a supply-demand imbalance and increasing demand for imports to support a growing market for ultra-low-viscosity engine oils. This period also marked the introduction of an unofficial Group III+ category with higher VI.

Development of API Base Oil Groups

The introduction of the base oil groups by API in the 1990s represented a significant milestone in the lubricants industry that was achieved through the efforts of many key participants. The five categories have weathered the test of time and remain relevant 3 decades following their creation.

The use of compositional properties like sulfur and saturates to differentiate API Group I (those produced using solvent refining) from Group II and Group III (by hydroprocessing) was simple in concept but was carefully considered during the group development process. At the time, there were three primary base oil producers in North America that used hydroprocessing technology, namely Chevron’s plant in Richmond, California; Petro-Canada in Mississauga, Ontario, Canada; and Sunoco in Yabucoa, Puerto Rico. Processing technologies and operating conditions differed amongst the three refiners, yet the intention by API was to define a base oil group that would embrace the new processing route to base oil manufacture.

Sun Yabucoa had the highest sulfur content at approximately 200-250 parts per million, in addition to the lowest saturates content — approximately 92% by weight. The boundaries for hydroprocessed oils were therefore set at a maximum of 300 ppm (or 0.03 wt%) for sulfur and a minimum of 90 wt% for saturates. At the same time, solvent refined base oils could not achieve either of these requirements, thus confirming the compositional guidelines as appropriate.

The subject of viscosity index was the next point of discussion, both in terms of establishing a minimum limit for Group I and Group II and to differentiate hydroprocessed base oils with nominal and high VI properties. VI of 80 was selected as the lower boundary as there were lower VI paraffinic base oils made from South Louisiana crude and similar crudes used as diluent oil or solubilizer for several additives used in engine oil formulations. On the higher end, an analysis of 117 commercially produced base oils of different kinematic viscosities, qualities and processing histories was conducted with a histogram of VI generated to determine the appropriate break point between conventional (Group II) and higher VI (Group III) qualities. As evident from the attached figure, 120 was deemed an appropriate point of separation, becoming the minimum requirement for Group III.

Part 2 in this series will look at the changing landscape in the global and North American automotive market, the growth in demand for high-VI base oils and how geopolitical conflicts restricted access of some markets, such as the U.S., to higher quality base oils.

H. Ernest “Ernie” Henderson is president of K&E Petroleum Consulting LLC, of Oklahoma City, Oklahoma, U.S. He has nearly five decades in the industry, including stints with Exxon, Imperial Oil and Petro-Canada, in research, marketing, logistics and technical services. K&E’s expertise ranges from base stock management and strategic planning to supply chain optimization, formulation cost control, raw material

sourcing and patent litigation.