Our Industry’s Own Odyssey

“The Odyssey,” a highly anticipated film adaptation of Homer’s Greek epic poem, is due to hit movie theaters in July. The story highlights the trials and tribulations of Odysseus, who spends 10 years at sea trying to return to his family and home in Ithaca after fighting in the Trojan War. Odysseus is forced to sail through unfamiliar oceans and fight sea monsters and divine creatures such as Poseidon, the god of the sea.

While base oil industry participants have not had to contend with mythical figures, they have had to navigate uncharted waters as the United States-Israel-Iran war and its ramifications have presented perplexing and unexpected challenges.

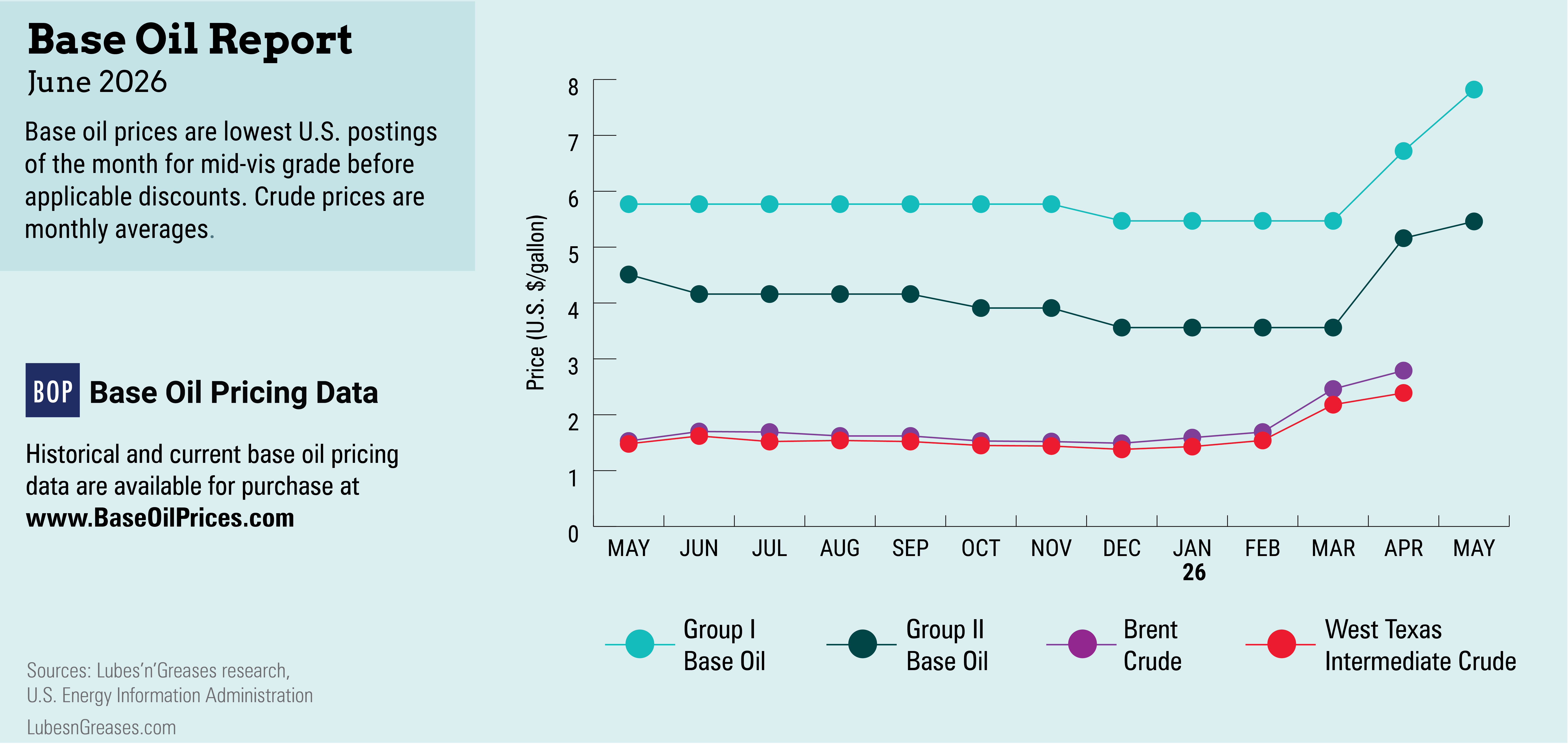

The conflict was still unresolved in early May and the Strait of Hormuz remained closed to most vessel traffic, leaving a fifth of the world’s oil exports unable to reach their destinations and sending crude oil prices to historic highs. Iran’s chokehold on the crucial passageway also kept shipments of other refined products such as base oils captive in the Persian Gulf, while Iranian drone and missile attacks damaged base oil facilities in the region, leading to prolonged shutdowns and significantly reduced global base oil supplies amid soaring prices. The API Group III segment was the most affected because almost a third of the world’s Group III capacity is located in the Middle East, but Group I and Group II grades were also experiencing extremely strained conditions.

A large share of global Group III volumes is also produced in Asia, but several Asian producers were forced to cut operating rates due to a shortage of Middle East crude oil, given that most refineries in Asia were built to run on Dubai/Oman, Murban and Arab sour crudes. Some countries started to import crude oil from other origins or resorted to using strategic emergency reserves, but many refiners had to prioritize fuel production to protect supplies for the general population, leading to reduced base oil output.

Demand for U.S. crude oil exports also increased as Asian refiners looked to diversify procurement given the disruptions in Middle East oil shipments. A tanker carrying U.S. crude oil arrived in Japan in late April, marking the first oil shipment from the U.S. since the Iran war began in late February. Mexico also agreed to supply Japan with one million barrels of crude oil.

While the United States seemed to be partly insulated from crude oil supply disruptions as local refineries are mostly able to process domestic crude and oil from other nearby origins such as Canada, Mexico and Venezuela, the base oil market was still affected by shortages in other regions because foreign buyers were eager to obtain U.S. products, and diesel prices also surged globally. U.S. base oil export prices rose quickly, pushing domestic values up as a result. Domestic producers noted that although U.S. production had not been “hit as hard” by Middle East oil supply disruptions, base oils were still very tight in the U.S.

Most U.S. suppliers were unable to offer volumes beyond those needed to fulfill contractual commitments, and spot supplies appeared to dry up as existing inventories were depleted. Concerns also emerged about the need to build inventories ahead of the hurricane season starting in June, with participants questioning whether they would be able to secure additional barrels to keep extra product on hand.

Since crude oil prices are determined by global supply and demand dynamics, geopolitical events and sentiment, U.S. base oil producers were not immune to the sharp price fluctuations brought on by the Iran conflict. In early May, West Texas Intermediate futures were hovering above $106 per barrel and Brent prices vaulted over the $110/bbl mark.

The sky-high crude oil values and significantly strained base oil supply and demand fundamentals led paraffinic and naphthenic base oil producers to implement almost weekly price increases since the start of the war on February 28. Some of the increases reached historic highs, with Group I grades at one point seeing individual hikes of over 70 cents per gallon, bright stock of 95 cents/gal, Group II cuts of $1.80/gal and Group III base oils of $2.50/gal in late April/early May.

Naphthenic base oil prices also saw several hefty increases, with markups of up to 70 cents/gal driven by regional supply and demand imbalances and volatile feedstock prices. Recent plant turnarounds also exacerbated tight supply fundamentals.

Lubricant and finished products manufacturers inevitably found themselves compelled to pass the mounting cost of base oils, additives, packaging and transportation down the supply chain, with most suppliers communicating price increases with implementation dates between March 11 and May 20. Blenders noted that given economic uncertainties brought about by rising energy prices, which affected businesses and consumers alike, and the fast pace of market changes, it has been very challenging to plan inventories and make pricing decisions.

At the time of writing, talks between the U.S. and Iran were at a standstill, and experts warned that even if hostilities were to cease overnight, the disruptions to crude, base oil and shipping markets were likely to last for several months, possibly well into 2027.

Gabriela Wheeler is base oil editor for Lubes’n’Greases. Contact her at Gabriela@LubesnGreases.com