What a Difference a Day Makes

Base oil market fundamentals were rapidly changing as this article went to press in early March. Crude oil and feedstock prices surged to multi-month highs after the United States and Israel launched a coordinated attack over the March 1 weekend against Iranian targets, killing key officials and damaging military facilities. However, oil analysts were concerned that a quick de-escalation of the conflict would erase the fresh gains, which is what happened in June 2025 when the U.S. struck Iranian nuclear facilities. Conversely, a prolonged war would likely help support prices and offset a planned OPEC+ output increase.

Similarly, base oil producers were evaluating global market conditions to determine whether any price adjustments were warranted in the long term. They cited growing concerns that the conflict in the Middle East would result in production and shipment disruptions as facilities in the Persian Gulf came under attack and ship operators suspended activity in the region after Iran closed the Strait of Hormuz. The situation did not only affect crude oil shipments, but diesel, gasoil and jet fuel movements as well. Freight and insurance rates surged due to the heightened war risk premiums.

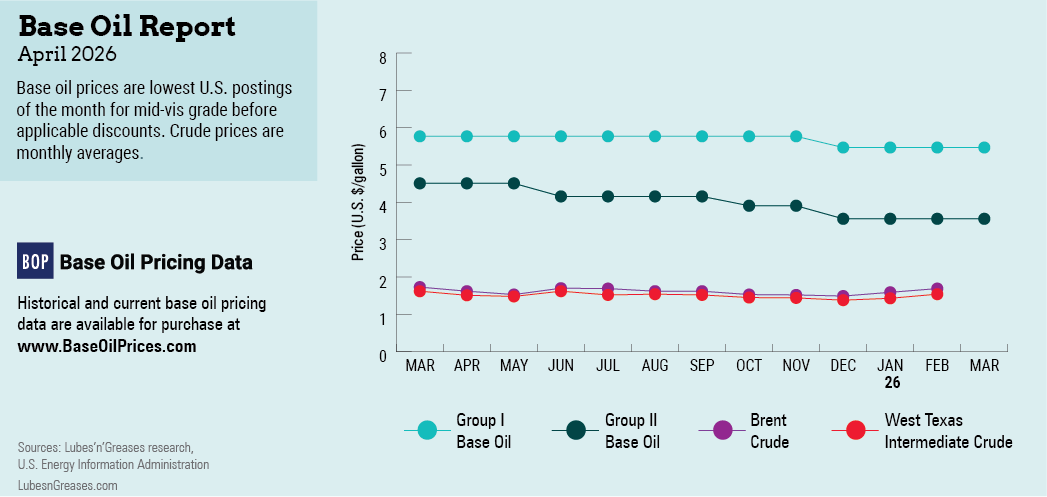

A number of base oil producers responded almost immediately by increasing prices, with hefty hikes sought for most base oils in Asia, and posted price increases announced in the U.S.

SK Enmove increased its Group II+ and API Group III U.S. base oil postings by 10 cents per gallon on March 1. Prices for Group III base oils were the most likely to be impacted by the situation in the Middle East as close to half of all U.S. Group III imports originate in that region, but South Korean products were also affected as refiners process Middle Eastern crude oil.

The SK price increase followed a couple of initiatives that emerged in February but that were unrelated to the situation in the Middle East. Two producers adjusted postings in late February — ExxonMobil and Motiva. Interestingly, the price revisions took prices in opposite directions, with one involving an increase and the other a decrease.

According to reports, ExxonMobil increased the price of its Group II+ EHC 45 grade by 25 cents per gallon on Feb. 20. Sources commented that this price increase was not so much a reflection of market conditions for standard grade Group II/II+ products, but rather an indication of high demand for Group III 4 centiStoke base stock. ExxonMobil has obtained Dexos approval for its EHC 45 product in passenger car motor oil applications, and it can be used in lieu of an approved Group III 4 cSt. Group III 4 cSt remained tight from most suppliers while demand was strong, with particularly healthy growth in Mexico as the quality of the country’s PCMO products is improving, driving prices up.

Meanwhile, Motiva lowered the posted price of its Group II, Group II+ and Group III grades by 50 cents per gallon on March 1. The company’s price revision was likely driven by a desire to get postings aligned with actual market values. But participants also said that not all accounts would be impacted by the price revisions, since the producer uses many different price formulas for contracts — some include postings and some do not. According to sources, there might be a drive by producers this year to return to the traditional practice of using posted prices as primary indices in price formulations.

The base oil market continued to be described as slightly long, with suppliers focusing on attaining a balanced supply and demand inventory position. In general terms, the Group I and Group II light grades were less readily available than the heavier grades, with spot prices for the latter being exposed to downward pressure as a result.

Prices for naphthenic oils had been stable since May 2025, with some support coming from the crude oil side as values had moved up in February on growing U.S.-Iran tensions. The more recent developments in the Middle East and surging crude oil prices were expected to exert additional upward pressure on pricing.

A tightening supply and demand scenario for the light pale oils, coupled with three plant turnarounds and efforts by the producers to build inventories to ensure all contract commitments were met during the outages offered additional price support. San Joaquin Refining completed a three-week scheduled turnaround at its refinery in Bakersfield, California, in early March. Cross Oil began a three-week turnaround at its plant in Smackover, Arkansas, on Feb. 20. Calumet planned to have a turnaround at its naphthenic plant in Princeton, Louisiana, in the first half of April.

The rapidly evolving fundamentals were expected to have a larger impact in other countries that are more reliant on base oil shipments from the Middle East, but North America was unlikely to remain immune given that markets nowadays do not function in isolation. Some refineries may reduce run rates to produce more distillates if prices for these products continue to climb. Steeper crude oil and feedstock values and higher freight rates affect all market participants one way or another.

Gabriela Wheeler is base oil editor for Lubes’n’Greases. Contact her at Gabriela@LubesnGreases.com