API Group II base oil will face the most pressure as global capacity additions in Asia and the Middle East exacerbate an already oversupplied global market. Among Group III projects, more than 600,000 tons/year is scheduled to come online across India, China, the United States and Saudi Arabia in 2026.

Group I will find the most balance as shuttered capacity that played key roles in export markets has left structural shortages, particularly with bright stock.

New Capacity Coming

Refiners have embarked on a wave of capacity additions spanning new projects and expansions or conversions at existing sites to address evolving base stock needs by region. The bulk of global capacity growth is happening in Asia, where about 3.4 million t/y of Group II and III capacity has started to come online. (See Figure 1.)

Figure 1. Wave of Asian Group II/III Capacity Additions Capacities from H2 2025

Thousands of metric tons/year

Note: Figures in ‘000/year

Source: ICIS Supply and Demand Database

ExxonMobil’s million-ton-per-year Group II expansion in Singapore, which came onstream in the fourth quarter of 2025, is the largest of these projects. Alone, the expansion represents 5% of 2025 global Group II capacity, according to ICIS’ Supply and Demand Database. The ExxonMobil site also addresses some of the structural bright stock shortage. The new Group II extra-heavy neutral base stock that ExxonMobil is now producing should be a suitable substitute for Group I bright stock in some applications.

India is also a key driver of growth, as its evolving demand needs prompted construction of two new plants and two expansions totaling 1.3 million t/y, mostly for Indian Oil Corp. Ltd.

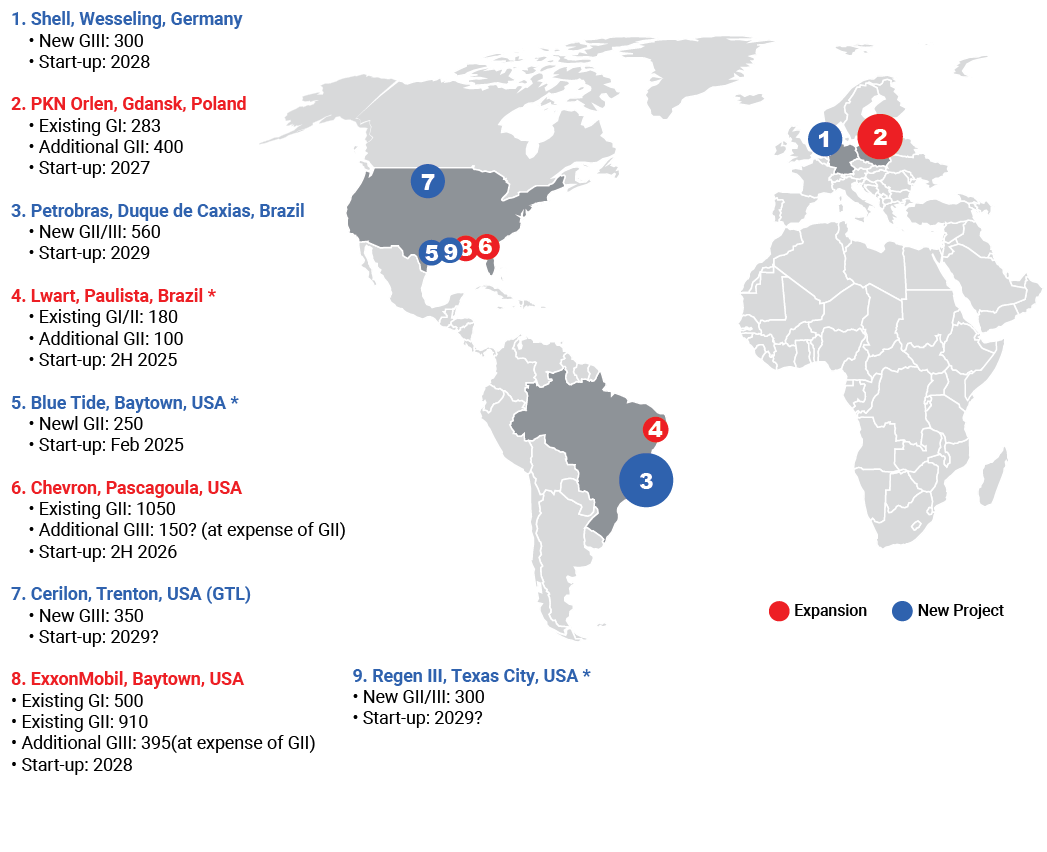

Fewer capacity additions or changes will happen in the Atlantic Basin, but projects will be more targeted to regional needs for localized supply. (See Figure 2.) In the U.S., upgrades now underway for Chevron and ExxonMobil are designed to add 545,000 t/y of Group III capacity, based on ICIS’ estimate of the size of Chevron’s project, which Chevron has not disclosed. Greenfield projects by Cerilon (gas-to-liquids) and ReGen III (rerefining) would bring the total increase to 1.2 million t/y but have not yet received final investment decisions. North American Group III consumption is about 2.2 million t/y, while current capacity in the region is around 575,000 t/y.

Figure 2. Wave of Atlantic Basin Group II/III Capacities Capacities from 2026

Thousands of metric tons/year

The U.S. will remain a net importer of Group III, but the need will be reduced with growth in domestic production. The impact of increased domestic production can be traced back to 2022, which at 2.6 million tons represented the high-water mark for U.S. base oil imports, most of which are Group III. In 2023, there was an 8% decline in import volumes compared with 2022. Full-year 2024 imports fell 2% from 2023, and 2025 imports were running 5% down through October.

Rising domestic production underpins these reductions, but slowly declining demand plays a role. While Group III demand is rising in North America, ICIS anticipates a net demand drop because these higher-quality oils are consumed more slowly, requiring less oil overall to fulfil downstream needs. A switch to Group III production by some domestic refiners is expected to cut into light Group II yields, as has been ongoing, but N100 is not expected to run short of contract requirements.

Utilization Rates Dropping

ICIS sees global base oil plant utilization rates between 60-70% in 2025, with Group I at the low end of that range and Group II and III closer to 70%. (See Figure 3.) Group I rates are expected to stay relatively flat for the next several years as the global capacity loss has exceeded the demand loss, but a gradual decline is then expected in the early 2030s as supply requirements fall in emerging markets.

Figure 3. Global Base Oil Capacity Utilization

A 3% drop in global Group II utilization rates is expected in 2026 because of the wave of new capacity coming online, but there should be recovery closer to 2030 as emerging demand catches up to supply. Group III utilization was close to 80% post-pandemic amid the demand surge, but it is expected to continue on a downward trajectory through 2035.

The five-year period to 2030 will be marked by global base oil oversupply as capacity is added before downstream demand appears in the 2030s in emerging markets. Global finished lubricant demand is expected to grow at a cumulative annual rate of 0.7% through 2030, driven by these emerging markets. (See Figure 4.) India is the leading driver, accounting for the bulk of Asia-Pacific’s 2.5% growth, followed by Africa, Latin America, the Middle East, Russia and other Baltic states.

Figure 4. Emerging Markets Drive Global Lubricant Demand Growth

India and Brazil are adding capacity of higher viscosity index oils to support this growth, but localizing their supply will cut into some import need. Growth in emerging markets will be offset by declines in mature markets of North America, Europe and northeast Asia.

These shifts in global lubricant demand are expected to drive compound annual growth of 1.8% for Group III (+0.7 million tons) and 0.4% for Group II (+0.3 million tons) and compound annual loss of 1.3% for Group I (-0.9 million tons) in the five-year period to 2030.

As global capacities grow, the U.S. is expected to continue to have surplus Group II despite any yield cuts from Group III production. U.S. exports soared to record heights in the last few years, consistently outpacing U.S. demand and driven by a surge in volumes to Mexico.

Overall U.S. base oil exports were also down in through the first 10 months of 2025 compared with the same period in 2024, driven by declines in volumes to key destinations: Mexico, Brazil and Europe. Exports to Africa, Middle East and Asia were up.

New Group II capacity in the Middle East and Asia may challenge these flows in years to come. Global capacity growth has potential to limit export options for the U.S., particularly areas where Asian-based refiners are more likely to compete: India, the west coast of South America, other parts of Asia and East Africa.

Upstream Price Drivers

ICIS analysts expect crude prices to fall through March 2026 and on average to be lower in 2026 compared with 2025, keeping feedstock costs lower for base oil producers. Geopolitical tensions in crude-producing regions have eased, reducing the risk premium and shifting sentiment to the expectation of oversupplied fundamentals curbing crude price rises.

While crude prices are expected to be down, diesel margins remain elevated, supported by supply disruption concerns. Tensions with Russia continue to constrain regional diesel flows, keeping margins higher than pre-pandemic levels due to tight supply. In turn, this raises the price floor for base oils.

U.S. Group II export margins largely align with diesel hydrocracker margins except in times of tight supply.

While domestic Group II margins have been compressed, they sit in healthy territory — above $150/t in the second half of 2025. As global Group II oversupply builds, these margins will remain challenged. At odds with the strong diesel dynamic, sluggish industrial activity and subdued consumption of transportation fuels observed over the past three years weighs on demand and limits upside for refiners.

Diesel margins are eventually expected to return to normalized (pre-pandemic) levels as geopolitical tensions fade and weak demand fails to support the elevated margins. Reduced diesel profitability would then incentivize refiners that also make base oil to prioritize the more stable and profitable refined product, which exacerbates oversupply.

Key Sensitivities

The ICIS outlook could change based on three wild cards that would affect the global supply-demand landscape. First, electric vehicle adoption is playing out very differently depending on region. The potential slowdown in Europe could bolster demand for base oil, while continued rapid adoption in China could have the opposite effect and accelerate demand decline in that country.

Second, the Russia-Ukraine conflict continues to affect the global base oil market. Ukraine’s effectiveness with strikes to Russia’s refineries will pressure diesel supplies to the global market, in turn potentially tightening base oil should refiners opt to produce diesel in the absence of Russian barrels.

Third, structural overcapacity of Groups II and III could accelerate the Group I decline rate. Group I-reliant regions like Africa are already turning to Group II out of necessity because it is more readily available and inexpensive relative to Group I.

Global demand growth will flatten toward the 2030s. China’s rapid road electrification will offset steady demand growth in India. Demand growth will be outpaced by supply additions, with Asia dominating the expansions. European and U.S. additions will address Group III demand growth.

In the U.S., that will mean less Group II, but not to a structural shortage. ICIS does not anticipate further Group I closures despite declining demand. Some new heavy Group II should fill heavy Group I voids.

In global trade, self-sufficiency is the key theme with regions localizing their supply. Most notably, U.S. onshoring of Group III production will drive an import decline from either South Korea or the Middle East. Trade trends indicate that imports from the Middle East have grown to account for more than half of total U.S. base oil imports, while imports from South Korea are declining.

Group I trade is likely to rise, primarily from Europe as local usage declines. Better balance is expected in the 2030s as emerging market demand rises.

Amanda Hay is senior editor manager for Base Oils Americas at ICIS, Independent Commodity Intelligence Services, a London-based provider of information and analysis on commodity markets.