Trying to Stay One Jump Ahead

As the clock struck midnight on New Year’s Eve, people in Denmark climbed onto chairs or sofas and jumped off. This symbolic leap is believed to bring good luck, leave bad vibes and negativity behind, and ensure a fresh start for the new year. Well, the base oils market hopped into 2026 carrying ample supplies, lusterless demand, soft crude oil values and several posted price decreases, reflecting difficult market conditions. While several of the challenges presented by 2025 were anticipated to continue impacting business in 2026, there were also many bright spots on the horizon.

Market participants were expected to use their experience over the past five years to look for solutions to ongoing problems and take advantage of shifting supply chain trends and trade flows — many of which were profoundly altered by the COVID-19 pandemic and more recent geopolitical developments such as the Ukraine-Russia war, the Israel-Hamas conflict, terrorist vessel attacks in the Red Sea, and a new United States tariff regime — to jump at fresh opportunities and move in new directions.

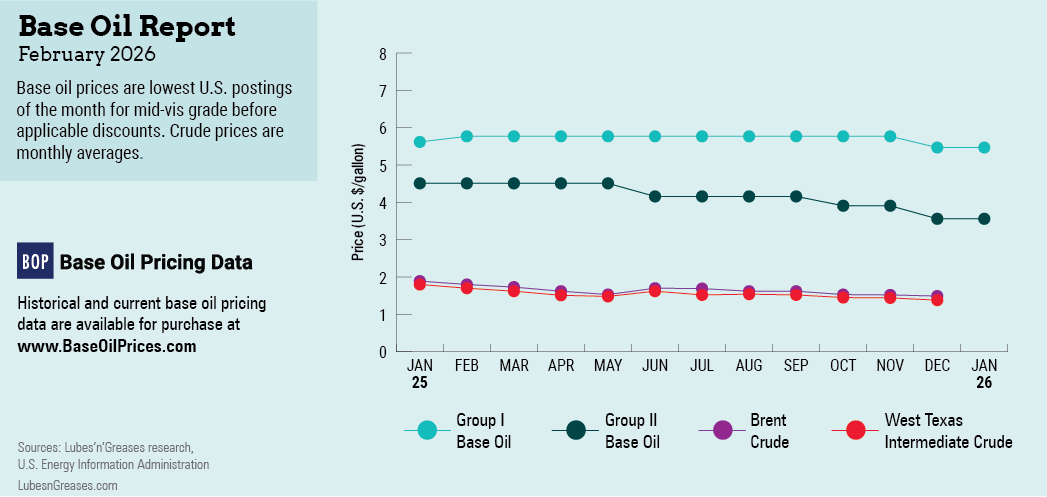

Several North American base oil producers announced posted price decreases in December — a noteworthy change from a fairly uneventful year in terms of posting adjustments. There were only six separate instances when producers communicated price revisions in 2025, and most of these initiatives originated from individual companies and did not apply across the board for a particular base oil group. One posted price adjustment was rescinded shortly after being communicated to customers.

The decreases that went into effect in December and affected mostly contract customers whose agreements are indexed against postings were likely triggered by sluggish demand, mounting inventories and a desire to encourage additional orders and bring posted prices more in line with actual transaction prices. While some players argued that posted prices had lost relevance and suppliers had therefore given up on posting revisions, other insiders predicted that there may be a return to more regular posted price adjustments in the new year.

Posted prices are widely used as a crucial pricing tool in the industry and serve as an initial benchmark for negotiations and contracts, rather than the exact final transaction price. Publicly announced posted prices enhance market transparency by providing a common reference point known to all buyers and sellers. This shared information helps participants understand market trends and price direction.

In early December, Chevron had been the first out of the gate with the announcement of 30 and 35 cents-per-gallon posted price decreases on its API Group II base oils, which went into effect on Dec. 2.

ExxonMobil, Paulsboro and HollyFrontier (HF Sinclair) decreased all of their Group I postings, with the exception of bright stock, by 30 cents/gal on Dec. 16, Dec. 19 and Dec. 24, respectively. ExxonMobil also marked down its Group II and Group II+ grades by 15 cents/gal, while HF Sinclair had no posting changes on its other base stocks.

Spot prices had been under downward pressure for a few weeks as well, with export numbers being strategically adjusted down as producers tried to manage inventories and release the extra barrels held during hurricane season into various destinations in Latin America, Africa, Asia and the Middle East.

Buying appetite for U.S. base oils had experienced an uptick in Brazil since November due to the unplanned shutdown of key producer Petrobras’ base oils plant in October. Demand from Mexico was weaker than earlier in the year, although regular contract cargoes continued to move south of the border, with some shipments affected by railway and trucking disruptions mostly linked to protests by Mexican farmers and truckers in northern Mexico.

Domestic paraffinic and naphthenic base oil demand was not anticipated to improve overnight, but there were expectations that orders would start to inch up in late January and show a more defined uptrend in February in preparation for the spring lubricant and grease production cycle.

Naphthenic base oil supply may see a temporary tightening in January as San Joaquin Refining has scheduled a maintenance program at its California refinery, although the producer plans to meet contract obligations during the outage.

Several base oil expansion and upgrade projects in Asia and the Middle East came on stream in 2025, and the increased production from these was anticipated to tip the global supply and demand balance towards overcapacity, causing continued downward pressure on prices. Growing rerefining rates were also expected to contribute to the oversupply conditions. While some key downstream segments such as traditional passenger car motor oil were not likely to show massive growth in the U.S., other sectors such as industrial, marine and heavy-duty oils have the potential to remain significant. Even though the adoption of electric vehicles seems to be slowing, EVs create new lubricant opportunities in the shape of e-motor fluids and thermal management. Ongoing industrialization will also bring steady consumption of hydraulic oils, metalworking fluids and process oils in manufacturing and energy sectors, while AI development and data centers will generate emerging demand for high-efficiency immersion cooling fluids.

Aside from economic trends and global geopolitics, one wild card that might partly determine base oil pricing in 2026 — although it will be less influential than supply and demand factors — is crude oil. Sentiment in crude markets was bearish during the last few weeks of the year on abundant supplies and prospects of reduced demand from key importing countries such as China. Futures were generally expected to remain under pressure in 2026 as the global market is likely to face a sustained supply surplus, particularly during the first half of the year.

Gabriela Wheeler is base oil editor for Lubes’n’Greases. Contact her at Gabriela@LubesnGreases.com