Time to Shift Gears?

Despite the fact that 2025 proved to be a challenging year for the base oils and lubricants industry, most market players remained optimistic about the future. At the ICIS Pan American Base Oils and Lubricants conference in Jersey City last December, several presenters talked about the rerefining segment–which has gained importance in recent years because of global sustainability goals–and about the developing technologies that might absorb a large portion of API Group III base oils supply in the future.

While there have been plant rationalizations on the Group I side over the last two decades, and additional plants may be decommissioned, Group II and Group III capacity in the Americas is expected to continue growing and many worry that the market will become oversupplied, pushing prices down.

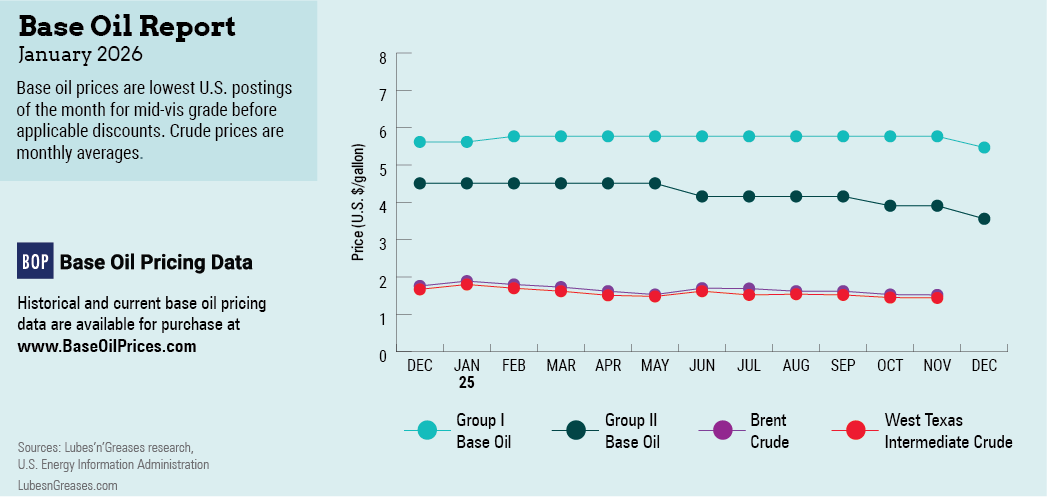

The last month of 2025 certainly reflected this trend as most suppliers faced soft demand and ample inventories, which exerted downward pressure on prices. It came as no surprise, then, that Chevron stepped out with a posted price decrease initiative in early December. The producer lowered the price of its Group II 100R grade by 30 cents per gallon, and its 220R and 600R by 35 cents/gallon on December 2. While no other producers reduced postings at that time, there was plenty of talk behind the scenes about the need for posted price adjustments to better reflect actual market prices. While some participants might be reluctant to disclose private discussions about pricing, others said that postings had always helped determine price direction and seemed to convey transparency to a complicated market picture, allowing buyers and sellers to use these prices as a coherent benchmark during contract negotiations. Some ventured to guess that there may be a general shift in the New Year whereby many producers might revise posted prices to use them more effectively during their contract negotiations.

Given sluggish domestic demand, several U.S. producers focused on finding opportunities to export base oils, although consumption in other regions had also slowed down ahead of the holidays. Spot export prices succumbed to downward pressure because of ample availability, coupled with producers’ efforts to lower inventories ahead of year-end tax assessments.

Crude oil futures fell to one-month lows early in December as analysts accounted for the possibility of a peace deal between Russia and Ukraine, which would potentially lift sanctions on Russian oil exports and increase global oil supplies. Aside from crude oil price fluctuations, however, refiners were watching the price of diesel as it was influencing refining decisions. Diesel prices had shot up because of a global tightening of supplies given sanctions on Russian diesel exports, along with Ukrainian attacks on Russian energy infrastructure. Russia is one of the largest exporters of diesel and a reduction in export volumes had a significant impact on global prices. If this continued to be the case, then it could prove to be more profitable to stream additional vacuum gas oil towards diesel production versus base oils, resulting in reduced base oil output.

In the meantime, paraffinic base oil availability was anticipated to remain plentiful because most plants were running at top rates, and the Excel Paralubes Group II/Group III unit resumed production in October, following a turnaround and catalyst change, which allowed the producer to maximize output. On the naphthenic side, a similar situation emerged as Ergon restarted its plant following a comprehensive maintenance program and additional volumes were introduced into the supply stream. Demand for the light pale oils was healthy, particularly from the transformer oil segment, which supported prices at a time when crude oil futures were slightly volatile.

While paraffinic posted prices remained largely unchanged, consumers did not give up hopes that suppliers would adjust values down before December 31, or in the first few weeks of 2026 as they might try to incentivize orders. Historically, there have been many instances when producers adjusted prices at this time of the year, but this year may be an exception. Producers explained that lowering prices would not necessarily trigger increased sales because demand was not likely to improve as fundamentals in downstream segments lacked strength. Steep diesel prices also limited the potential of refiners lowering base oil values.

Looking ahead, there were expectations that demand for automotive lubricants, particularly from the PCMO segment, would continue to decline due to improved fuel efficiency standards and prolonged drain intervals in new car models. However, experts believe that demand for Group II and Group III base oils would see an uptick as these premium grades gain ground in marine and heavy-duty applications, as well as in dielectric fluids used in immersion cooling for bourgeoning data centers. Base oils producers need to have an open mind and look for fresh opportunities in new, perhaps more specialty-type markets, as well as in developing economies in Latin America as conditions and requirements keep shifting on a global scale.

Gabriela Wheeler is base oil editor for Lubes’n’Greases. Contact her at Gabriela@LubesnGreases.com