Lessons from Formula 1

Over the first weekend in April, the Japanese Formula 1 Grand Prix took place in the Suzuka circuit, with ten teams vying for the title. It was an exciting event for the home crowd because Yuki Tsunoda, currently the only Japanese Formula 1 driver, was promoted to the Red Bull team to race alongside World Champion Max Verstappen.

Unfortunately, the race was rather uneventful and Tsunoda did not finish in a point-scoring position, which was rather disappointing for his fans.

Similarly, base oil demand was off to a somewhat slow start despite expectations of requirements gathering speed at the start of the spring season. Wavering lubricant consumption tied to economic uncertainties in the United States and neighboring countries prompted consumers to remain cautious in terms of purchased volumes. In Mexico, buying interest was somewhat hasty as buyers were hoping to replenish inventories or beat the potential implementation of tariffs. Volatile crude oil and feedstock prices amid geopolitical tensions and a budding trade war stirred up additional concerns.

Crude oil prices had been on a downward trajectory for most of March but showed an unexpected uptick at the end of the month on optimistic economic data from the industrial segment and retail sales in China—the world’s top crude oil importer.

However, the upward trend was short-lived, as U.S. president Donald Trump’s sweeping tariff announcements in early April led to a stock market crash and plummeting crude values on fears that the escalating trade war between the U.S. and other countries would spark a global recession and dampen energy demand. West Texas Intermediate crude futures closed at $69 per barrel on March 25 and dropped to $59.58/bbl by April 8.

On April 2, Trump issued an executive order calling for a 10% tariff on goods imported into the U.S. from all countries, effective April 5, and varying duties or “reciprocal measures” of up to 50% on imports from specific trading partners with trade deficits with the U.S., effective April 9. Certain goods, such as copper, pharmaceuticals, semiconductors and some energy products were exempt from these high reciprocal tariffs. Trump also imposed a 25% levy on passenger vehicles, light trucks and automobile parts imported from all countries in March, with some exemptions for Mexican and Canadian goods.

U.S. manufacturers who purchase components and raw materials from China were facing soaring costs as Trump announced steep tariffs totaling 104% on Chinese imports, effective April 9, as China did not withdraw the retaliatory tariffs it imposed on U.S. products.

Governments around the world rushed to schedule phone calls and meetings with the administration in Washington, hoping to discuss proposals that involved lowering their import duties to avoid the tariffs. Amid all of this turmoil, it was unclear what products would be subject to tariffs and which would be exempt. Base oil market participants said that more time was required to ascertain the impact of the new regulations.

While many companies that are involved in base oil trading and source products overseas attempted to make sense of the tariffs, other market participants tried to focus on the day-to-day business minutiae ahead of the start of the summer driving season.

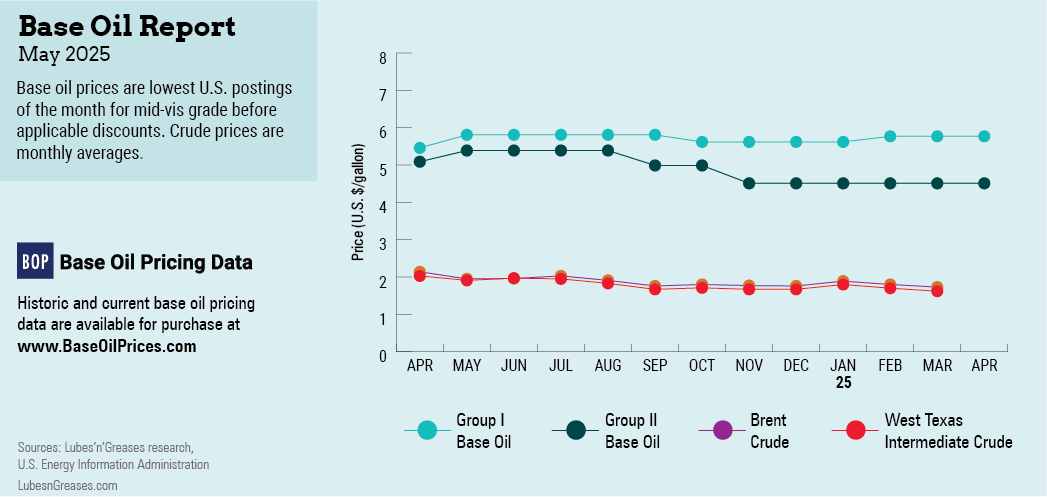

Domestic base oil demand was described as steady but not particularly strong. Given a fairly tight base oil spot supply-and-demand scenario, spot prices were on firm ground or edged up slightly, depending on the grade, while posted prices were stable.

Most API Group I cuts found strength from ongoing buying interest and adequate availability, but spot prices for bright stock climbed because of limited global supplies and heightened export opportunities.

A similar situation applied to the light and heavy-viscosity grades in the Group II segment given strained supplies on the back of plant turnarounds and improving consumption, despite a general downturn in automotive demand for the Group II and Group III grades.

Several base oil units were scheduled to undergo turnarounds in March and April, including those of Calumet, Chevron and Ergon. All the suppliers assured customers that they had built ample inventories to cover contractual requirements during the outages, but spot supplies were expected to tighten.

Similarly, spot prices for Group III base oils also moved up because of curbed supplies on the back of plant turnarounds. Domestic producers had trimmed Group III output and increased Group II production in the previous weeks, and import volumes had declined slightly. The turnarounds were scheduled between March and June, both in the Americas, as well as in Asia and the Middle East, including those of Petro-Canada, SK Enmove and Bapco.

On the naphthenic side, prices for light pale oils were supported by a snug supply-and-demand ratio. Consumption from the transformer oil sector, ongoing demand from other segments and a recent plant turnaround resulted in tight conditions. Producers were keeping a close eye on volatile crude values and explained that they would consider base oil price adjustments only if crude remained at a certain level for an extended period.

Just like in a high-speed race, with all the trade upheaval and geopolitical tensions, market conditions may switch from one minute to the next, and participants need to be ready for any slick spots on the track

Gabriela Wheeler is base oil editor for Lubes’n’Greases. Contact her at Gabriela@LubesnGreases.com