The Winding Road Ahead

The first two weeks of Donald Trump’s presidency were hectic and tumultuous. Along with a fusillade of executive orders, the U.S. president made good on his promise that he would impose tariffs on imports, starting with a round of levies on Mexican, Canadian and Chinese goods scheduled to take effect on Feb. 4.

This action was immediately met by retaliatory measures from China and saw a one-month postponement in the case of Mexico and Canada amid ongoing negotiations with the countries’ leaders.

While it was not yet evident what the exact repercussions of the tariffs would be on the lubricants industry, what was clear was that the tariffs would upend current trade patterns, have a significant impact on crude oil and feedstock prices—since Canada is the top oil exporter to the U.S.—and possibly lead to an increase in the price of imported base oils and related articles. Trump’s initial executive order specified that crude, energy and refined products imported from Canada would be subject to a 10% levy, but there were questions about which specific products would fall under this category. The first reaction to the tariff news was a spike in crude oil futures, with West Texas Intermediate values trading near $75 per barrel on Feb. 3. However, prices slipped once it was announced that the tariff implementation on Canadian and Mexican goods would be delayed until March.

The automotive segment could suffer significant impact from tariffs on Mexican goods, as the price of vehicles manufactured in Mexico would likely increase, and this could depress car sales in the U.S., ultimately hurting the fuels and lubricants industry. Several major U.S. automakers operate manufacturing facilities in Mexico.

In the case of China, a 10% import tax on products from the country was still scheduled to take effect on Feb. 4. U.S. lubricant manufacturers were concerned about a likely price increase in raw materials and packaging imported from China, which they said would be difficult to pass on to consumers as competition among suppliers remained strong.

China announced retaliatory tariffs on several U.S. exports, with a 15% tariff to be implemented on coal and liquefied natural gas products as well as a 10% tariff on crude oil, agricultural machinery and large-engine cars. The tariffs would take effect on Feb. 10.

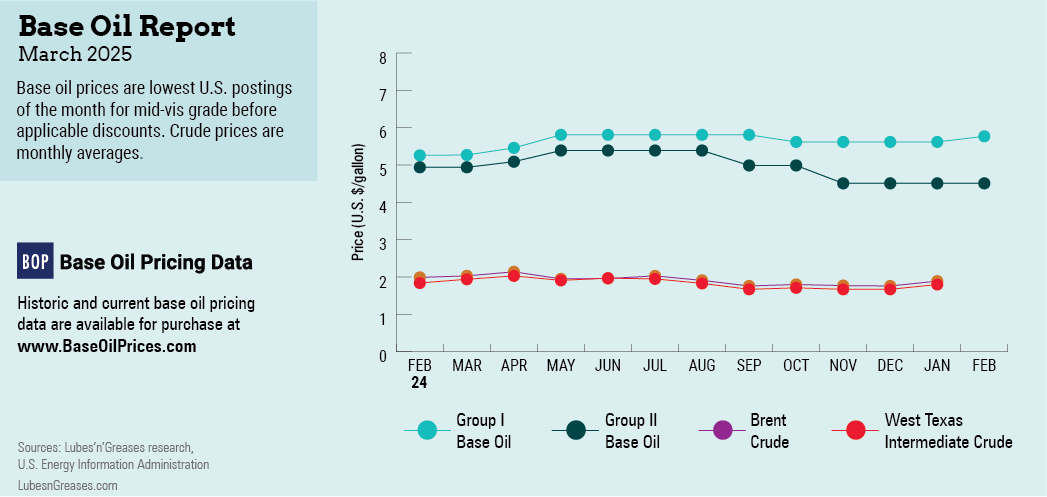

The emerging economic uncertainties, steeper crude oil and feedstock prices, compressed margins and an improved supply-demand balance drove several base oil producers to step out with posted price increases in early February.

According to reports, ExxonMobil communicated a posted price increase of 15 and 25 cents per gallon on its API Group I grades, 15 cents/gal on its Group II cut and 25 cents/gal on its Group II+ grade, effective Feb. 1.

Other Group I, Group II and Group II+ producers, including HollyFrontier Sinclair, Calumet, Paulsboro and Safety-Kleen implemented similar initiatives between Feb. 1 and 7.

Some buyers had secured additional base stock volumes in late January and early February to beat potential price increments given crude oil price volatility, but base oil consumption was not anticipated to show a significant change until the spring, when it typically improves because of heightened lubricant production ahead of the summer driving season. In some segments of the market, fundamentals were weighed down by oversupply, while in others, they were more balanced.

Upcoming plant turnarounds and an expected demand surge in the spring might tighten base oil supplies as the market moves into March. Availability of Group I cuts was likely to remain strained because of structural deficits and healthy demand in the domestic arena, as well as from the export market. Bright stock was described as enjoying robust demand against cramped supplies.

Chevron was expected to commence a three-week turnaround at its Pascagoula, Mississippi, Group II plant in March. The turnaround may lead to a tightening of spot Group II supplies, but contractual obligations were likely to be fully met, sources speculated. The producer does not disclose details about its plant operations.

Calumet will be completing a two-week maintenance program at its Group I and Group II units in Shreveport, Louisiana, in the second half of February. The producer has assured customers that it plans to have ample inventory to cover orders during maintenance.

The Group III sector was fairly quiet, with 6-cSt and 8-cSt grades showing tighter conditions than 4-cSt cuts and supporting slightly higher spot pricing as a result.

On the naphthenic side, San Joaquin Refining scheduled an annual maintenance program at its naphthenic base oil plant in Bakersfield, California, which started on Jan. 31. The program will last up to three weeks, but the producer was expected to continue meeting contractual obligations during the shutdown.

Naphthenic prices were largely stable, supported by balanced supply and demand conditions, particularly for the light-viscosity grades. Producers said that they were monitoring crude oil and feedstock values closely, and if higher costs were to be sustained for a few weeks, they would likely trigger price revisions, although none had emerged at the time of writing.

Market players tried to divine whether the balance of the Group II producers would seek price increases as their inventories were deemed balanced-to-long and prospects of a short-term demand recovery were nebulous. Some suppliers may be recalling temporary value allowances granted in the fourth quarter instead of adjusting posted prices. Whether additional price initiatives would emerge remained to be seen, but this was just one of many curves that market participants must negotiate on the road ahead.

Gabriela Wheeler is base oil editor for Lubes’n’Greases. Contact her at Gabriela@LubesnGreases.com