A Spring Full of Contrasts

The spring season was rather atypical for base oils and lubricants this year. Demand traditionally peaks during this timeframe as lubricant suppliers build inventories ahead of the summer driving season, unofficially kicking off on Memorial Day in the United States. Base oil and additive producers usually see a significant uptick in demand and a tightening of supply, which in the past had sometimes encouraged price increase initiatives.

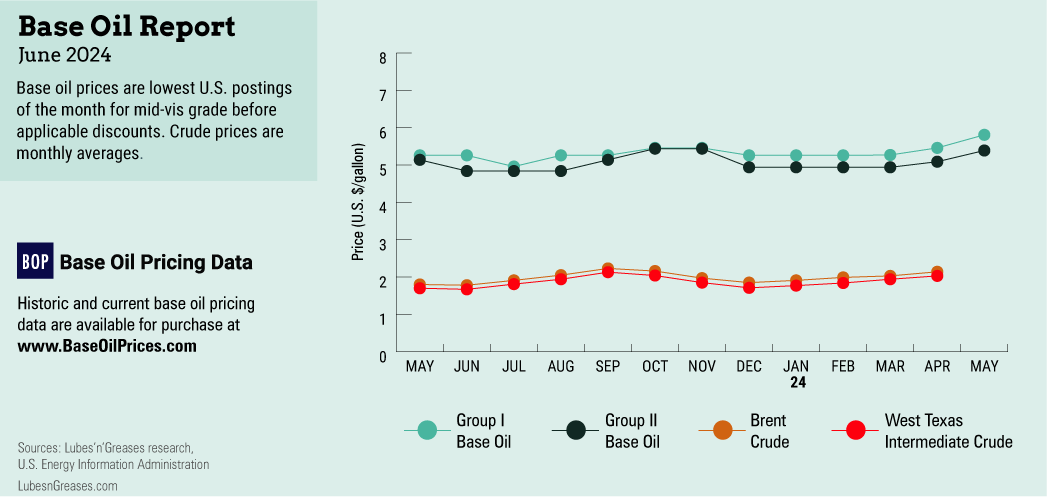

This year, too, consumption has increased but not as strongly as suppliers had hoped. Prices have gone up for most grades, but they stood on precarious ground, as one of the forces driving the increases was a surge in crude oil and feedstock prices, which started to fizzle by early May.

Most Group I and Group II suppliers communicated price increases in April, with the initiatives lifting API Group I, Group II and Group II+ postings by 20, 30, 35 and 40 cents per gallon—depending on the grade and the supplier—between April 11 and April 19. Petro-Canada also raised its Group II+ 100N grade by 35 cents/gallon, but the company’s 65N grade remained unchanged.

The April initiatives came on the heels of a previous round of increases that was largely implemented between March 15 and April 1, although a couple of producers had announced increases in February, and these finally saw implementation in March. A U.S. producer and a South Korean supplier did not communicate any price increases in February, March or April.

While there were reports of temporary value allowances (TVAs) and special discounts having been granted when the increases were first announced, it appeared that the initiatives were by and large implemented as planned.

In contrast with these rounds of posted price increases, in early May, Motiva surprised the market with a price decrease on its Group II+ and Group III base oil grades. There was speculation that the producer was lowering its posted prices to bring them more in line with actual transaction levels, as prices within these segments had succumbed to downward pressure. Most participants agreed that the move was not a reflection of the general market fundamentals that impacted other grades.

Shortly after Motiva’s announcement, SK Enmove also communicated that it would be lowering its Group II+ and Group III prices, signaling once again that supply in these segments had lengthened and had started to surpass demand. While U.S. Group III supply and imports were deemed plentiful, most Group I and Group II base oil cuts were fairly tight on improved domestic demand and brisk export business, once again showing a diverging price path from the Group III grades.

Motiva reduced its two Group II+ postings by 15 cents/gallon, while the company’s Group III 4 cSt was lowered by 50 cents/gallon, and its 6-cSt and 8-cSt grades by 30 cents/gallon, effective May 1. SK Enmove informed its customers that the company would be lowering its posted prices retroactively, with an effective date of May 1. The price of SK’s Group II+ 70N grade was reduced by 15 cents/gallon, its Group III 4-cSt grade by 20 cents/gallon, its 6 cSt by 10 cents/gallon and its 8 cSt by 50 cents/gallon.

On the naphthenic front, Calumet, Ergon, Process Oils and San Joaquin Refining raised naphthenic base oil prices by 30 cents and 35 cents/gallon, between April 15 and April 22, driven by similar fundamentals to those that fueled increases on the paraffinic side. Suppliers were standing firm by these initiatives, and the increases were reported to have been applied.

A fairly tight supply and demand balance supported the naphthenic price increases, particularly as the light grades used for transformer oils saw healthy demand on the back of recent plant turnarounds. Buying interest for the heavy-viscosity grades from the industrial, rubber and tire segments also ramped up ahead of the busy summer season.

Despite heightened activity during the spring lubricant production season, suppliers on both sides of the business agreed that base oil demand was less robust than in the spring of 2021and 2022 and had not reached anticipated levels by April.

Crude oil and feedstock price volatility also added a layer of uncertainty to the market. By early May, crude oil futures had slipped back to levels seen before the base oil price increases were announced. The slide in crude oil values was triggered by hopes of a possible ceasefire agreement between Hamas and Israel, which mitigated fears of a more widespread conflict in the Middle East that could bring oil supply disruptions.

Hefty crude oil inventories in the United States were also seen as a sign of slowing demand. On May 7, West Texas Intermediate (WTI) June 2024 futures settled on the Nymex at $78.38 per barrel, compared to $83.47 per barrel for April futures on March 19.

With the start of the driving season just around the corner at the time of writing, it will be interesting to see whether the contrasting currents roiling the base oils market will slowly subside, or whether they will become even more pronounced as lubricant consumption reaches its denouement.

Gabriela Wheeler is base oil editor for Lubes’n’Greases. Contact her at Gabriela@LubesnGreases.com