Halfway into January and business was scant. Participants were still optimistic that activity in the domestic market would gradually pick up over the next few weeks and considerably improve as the spring production cycle began. Many participants finished the year with lean inventories to avoid tax repercussions and were expected to replenish inventories as well.

For the time being, producers reported that business was still “relatively slow,” with demand at anticipated levels and customers taking projected volumes under contract. Spot business remained thin, but suppliers were heard to be in negotiations for export transactions.

Supply of most grades was deemed sufficient to cover current requirements, but API Group I showed tighter conditions than the other grades because of steady demand against a global decline in Group I production, together with fairly brisk United States export business in late 2024.

Group II cuts also entered the year on slightly strained conditions given an unplanned shutdown at the Excel Paralubes Group II/III unit in Lake Charles, Louisiana, last November that led to a temporary tightening of short-term spot supply. The producer has limited its spot volumes and seemed to be less active on the export front.

Chevron scheduled a three-week turnaround that at its Group II plant in Pascagoula, Mississippi, starting in March, according to market sources. The turnaround may also contribute to tightening the supply/demand ratio in the Group II segment. The company was expected to start building inventories to cover commitments during the outage and perhaps reduce its spot availability, although there was no company confirmation about the shutdown details.

Calumet will also be completing a two-week maintenance program on one of its units in Shreveport, Louisiana, in the second half of February. Shreveport produces Group I and II base oils. The producer plans to have ample inventory to cover orders during maintenance, a company source said.

Expectations were that the Group III segment would remain well-supplied, as domestic producers have increased Group III production rates at their Group II/III facilities, although there is talk that Group III output may be dialed down. There were also regular incoming shipments to North America from the Middle East and South Korea over the next few weeks, with volumes shipped from South Korea in December falling compared with previous months.

Naphthenic values stayed fairly level despite some crude oil price fluctuations over the last few weeks. A balanced-to-tight supply scenario of the light-viscosity grades offered support to pricing, even though a seasonal slowdown in demand for the heavy-viscosity pale oils from segments such as the tire and rubber industry placed some pressure on values. Most segments should see revived buying interest in the spring, according to sources.

Naphthenic base oil producers hoped that the incoming U.S. administration’s policies would support demand for drilling fluids, solvents, transformer oils and other applications that require naphthenic base oils in their formulation and were careful about product allotments moving into the new year.

Paraffinic U.S. suppliers were in negotiations for export transactions, with several players discussing business into Mexico. Business was still slow despite some fresh inquiries earlier this week, but was expected to pick up steam next week, according to sources.

Sellers were also looking into opportunities to ship base oils to Brazil, a trading partner that had imported significant volumes last year. Domestic output in Brazil declined during the last quarter of the year, but consumers were in possession of ample inventories given strong imports during the preceding months. While demand in Brazil typically increases after the Carnival holidays at the end of February, it was expected to be slightly dampened by the need to work down existing stocks, although Brazilian suppliers may also resort to regional exports to lower inventories. Details of a 2,000-metric ton cargo of base oils for shipment from Houston, Texas, to Rio in mid-December emerged this week, and there were also reports of a South Korean parcel expected to reach Brazilian shores in January.

A number of U.S. base oil cargoes were also concluded for shipment during the month of December to Nigeria and South Africa. Whether these transactions would be repeated remained to be seen, as sellers had been more inclined to put forward competitive pricing at the end of the year to reduce inventories before tax assessments and seemed reluctant to reduce their offer levels now. Nevertheless, export prices were heard to have continued to slide week-on-week by a few cents per gallon as some sellers were eager to capture new business.

In other export news, it was heard that about 37,000 tons had been booked for shipment from the U.S. Gulf to Antwerp, Belgium, between January 22 and 25. A 4,000-ton lot was mentioned for shipment from Pascagoula, Mississippi, to Singapore in the second half of January. A number of cargoes were also finalized for shipment from the U.S. Gulf to Mumbai, India, in December. Export business to India has been less vibrant than anticipated as domestic production in India has increased, making Indian buyers less dependent on imports.

In other business in the Americas, a 7,500-ton cargo made up of three base oil grades was quoted for shipment from La Plata, Argentina, to Hamriyah for January dates. Shipments to West Coast South America have seen delivery disruptions due to a powerful surge of unusually large waves that have caused fatalities and port closures.

Downstream, demand continued to be described as lackluster, and participants did not expect too many changes until after the inauguration of the next U.S. president on January 20. Trump has promised to impose tariffs on imports and there have been many uncertainties regarding how the new policies might affect the base oils and lubricants industry.

With market conditions remaining dull, lenders resorted to granting discounts to protect market share against a backdrop of increased competition and steep production costs, despite base oil price decreases in the last quarter of 2024. Some additive suppliers granted discounts into select accounts in late 2024 too, but not all customers enjoyed this benefit, while a majority of lubricant and grease manufacturers continued to deal with steep energy and raw material values.

As previously reported, given a drop in lubricant demand from key segments such as the automotive industry, competition among independent and major lubricant manufacturers has mounted and suppliers granted decreases throughout 2024, with four announcements made during the year – although not all suppliers implemented decreases at the same time and the amount of the price reductions varied.

Crude and Diesel

Crude oil futures extended their recent rally on Tuesday on an expected drop in U.S. crude inventories last week, but there were lingering concerns about global demand levels. Traders continued to keep an eye on economic developments in major oil importing countries such as China to evaluate demand trends, as well as possible supply disruptions in the Middle East and Africa.

In China, a fire was reported at Sinopec’s Zhenhai refinery in one of its crude distillation units. The blaze was extinguished late on Tuesday, with no casualties or injuries reported. The incident took place during the commissioning of new units in a major expansion at the refinery, media reports said.

On January 7, West Texas Intermediate February 2025 futures settled on the Nymex at $74.25 per barrel, compared with $71.72/bbl on December 31.

Brent futures for March 2025 delivery were trading on the ICE at $77.33/bbl on January 7, from $74.64/bbl on December 31.

Louisiana Light Sweet crude wholesale spot prices were hovering at $76.56/bbl on January 6, from $74.03/bbl on December 30, according to the U.S. Energy Information Administration.

Low-sulfur diesel was $2.36/gal at New York Harbor, $2.28/gal on the Gulf Coast and $2.42/gal in Los Angeles on January 6, compared with $2.28/gal, $2.22/gal and $2.32/gal, respectively, on December 30, according to the EIA.

Correction: A previous version of this report stated that a 5,000-ton base oil cargo had been loaded in Pascagoula to Mumbai and/or Hamriyah, UAE. This has now been removed.

Contact Gabriela Wheeler directly at gabriela@lubesngreases.com

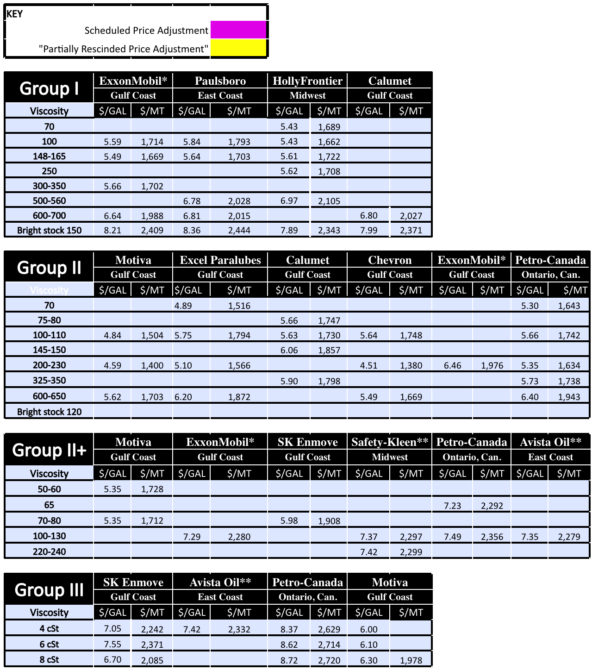

Posted paraffinic base oil prices: January 8, 2025 (FOB basis, USD/gallon and USD/metric ton)

Lubes’n’Greases Publications shall not be liable for commercial decisions based on this report.

Archived reports are here. Historic and current base oil pricing spreadsheets available to buy here.

*ExxonMobil prices obtained indirectly

**Rerefined