The base oils market was understandably quiet during the last few days of the year, with the recent posted price decreases having been implemented for the most part, and participants enjoying some downtime before activity picks up again in January. While base oil and lubricant demand was not anticipated to improve overnight, there were expectations that orders would start to inch up in late January and show a more defined uptick in February in preparation for the spring lubricant production cycle. Crude oil prices were somewhat volatile during the week, swayed by tensions in the Middle East and hopes that a Ukraine-Russia peace deal would attained.

Crude oil prices were generally expected to remain under pressure in 2026 as the global market is likely to face a sustained supply surplus, according to a report by ING Bank. The peak of the surplus was likely to occur in the first half of 2026.

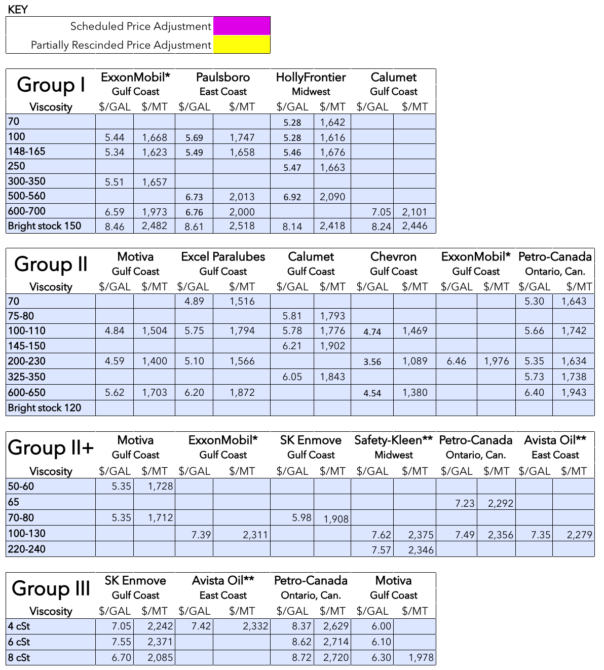

Several base oil producers announced posted price decreases in December, a change from a fairly uneventful year in terms of posting adjustments. There were only six separate instances when producers communicated price revisions in 2025, and most of these initiatives originated from individual companies and did not apply across the board for a particular base oil group. One posted price adjustment was rescinded shortly after being communicated to customers.

The latest posted price decreases, which went into effect in December and affected mostly contract customers whose agreements are indexed against postings, were thought to have been triggered by sluggish demand, mounting inventories, a desire to encourage additional orders and bring posted prices more in line with actual transaction prices. While some participants argued that posted prices had lost relevance and suppliers had therefore chosen not to embark on price revisions any longer, other insiders speculated that there may be a return to more regular posted price adjustments in the new year.

Earlier this month, Chevron had been the first out of the gate with the announcement of a 30 cents-per-gallon and 35 cents/gal posted price decrease on its API Group II base oils that went into effect on December 2.

ExxonMobil and Paulsboro Refining Co. decreased all of their Group I postings, with the exception of bright stock, by 30 cents/gal on Dec. 16 and Dec. 19, respectively. ExxonMobil also marked down its Group II and Group II+ grades by 15 cents/gal.

HollyFrontier (HF Sinclair) communicated a posting decrease of 30 cents/gal on its Group I grades, with the exception of bright stock, which remained unchanged. The adjustment went into effect on Dec. 24. The producer also noted that there were no posting changes on its other base stocks.

Another strategy that producers implemented during the last few weeks of the year to manage inventories and release the extra barrels held during hurricane season, which officially runs from June 1 to November 30 in the Atlantic and Central Pacific basins, was to lower export spot prices and entertain opportunities into Mexico, Brazil, West Coast South America and the Middle East. As was the case with U.S. business, buying interest from export outlets wound down as the year drew to a close.

Group I

There continued to be mixed conditions reported in the Group I segment, with the lighter grades remaining in tighter supply than the heavy grades. The SN500 cut and bright stock saw some lengthening, which placed downward pressure on spot pricing throughout the month, although bright stock was likely to tighten again shortly because production capacity has diminished globally on Group I plant rationalizations, while demand remains generally robust, particularly from marine and heavy-duty applications.

Given waning domestic demand, suppliers had also explored export opportunities to manage inventories and maintain their customer base. A recent uptick in buying appetite for U.S. base oils in Brazil emerged in November due to the unplanned shutdown of key producer Petrobras’ base oils plant since October. The outage was prolonged beyond the dates that had originally been estimated, and the producer faced some difficulties in meeting all of its commitments. The tightening of local spot supplies–and bright stock in particular—drove domestic prices of bright stock to higher levels for January transactions. The remainder of the Group I grades experienced some softening in the realm of 1-2% for January business. Some buyers opted for using Group II grades instead of Group I cuts whenever applications allowed.

There was also competition from Asian suppliers, who offered attractive spot pricing into Brazil. A 3,500-metric-ton cargo of base oils was heard to have been shipped from Malacca, Malaysia, to Santos, Brazil, on the Southern Owl between Dec. 14-17. Discussions to move U.S. products to Brazil abated with the approach of the year-end holidays.

U.S. exports have also been moving regularly to Mexico, where earlier challenges related to transportation disruptions and difficulties renewing base oil import licenses had slowed down the pace of shipments. Some of the disruptions appeared to be mostly linked to protests by Mexican farmers and truckers in northern Mexico. Mexican buyers had also held off on commitments in hopes of attaining more competitive pricing as U.S. suppliers strove to reduce inventories. As was the case with other export destinations, negotiations largely came to a halt due to the Christmas and New Year’s interstice.

Group II

Chevron and ExxonMobil decreased Group II posted prices in December, reflecting market fundamentals, with ample supplies, slowing demand and softer crude oil prices exerting pressure on pricing. Domestic demand was not likely to improve substantially until February or March, with suppliers hopeful that blenders would start to prepare inventories for the spring production season.

U.S. Group II producers had also managed to place products into several export destinations in Latin America, Europe and Africa. India was also the recipient of several U.S. cargoes, but business was more muted than in years past when significant amounts of U.S. base oils moved to India in the fourth quarter. Plentiful regional availability in Asia and difficulties in making numbers work when freight rates hovered at steep levels were some of the roadblocks hampering the conclusion of deals.

Rerefiners also mentioned fairly steady domestic demand and a sudden tightening of some cuts, with a few cargoes also having made their way to Mexico. An upcoming maintenance program at a rerefinery in the first part of 2026 was anticipated to strain availabilities since the producer plans to build inventories to meet contract obligations during the shutdown.

Group III

Prices of the Group III heavy grades were exposed to downward pressure because of lengthening supplies in the U.S. as several import shipments from Canada, Asia and the Middle East arrived in December or were scheduled for arrival in January. Demand was not keeping up with supplies as activity in the PCMO segment has slowed down and was not anticipated to improve over the next few weeks. Nevertheless, participants said that most cargoes had found a home as suppliers had offered attractive pricing to promote orders. The 4 cSt continued to be described as less available than the 6 cSt and 8 cSt grades.

Meanwhile, domestic production of Group III grades and rerefining output were steady, but most producers were using their Group III base oils for downstream lubricant production and these barrels did not seem to impact the general market trends.

Naphthenics

Naphthenic base oil prices were generally stable, but a number of accounts have seen lower pricing because contracts are indexed against diesel prices, which had fallen in the previous weeks. Demand for the heavy grades from the rubber, tire, grease and process oil segments remained lackluster as was expected for this time of the year, and prices were under pressure. Consumption of the light grades, which had so far been healthy due to ongoing demand from the transformer oil and infrastructure segments, has declined, but was still stronger than for the heavy cuts.

Export activity has also weakened, depriving suppliers from opportunities to place their products in other regions and reduce inventories at home. Additional downward price pressure emerged from the paraffinic side as paraffinic supplies, which remained abundant, competed in some applications with naphthenic oils.

San Joaquin Refining plans to embark on a three-week routine turnaround at its refinery in California in mid-January and was expected to start building inventories to keep customers supplied during the shutdown, which could lead to reduced spot availability.

Crude Oil

Crude oil futures slipped on Tuesday in thin holiday trading as markets tried to digest news of disappointing prospects for a ceasefire in Ukraine. Growing tensions between key oil producers Saudi Arabia and the United Arab Emirates also added a degree of uncertainty. Russian oil production was expected to grow in 2026, fanning concerns about global oversupply.

- West Texas Intermediate February 2026 futures settled on the Nymex at $57.95 per barrel on Dec. 30, down from $58.01/bbl for front-month futures on Dec. 22.

- Brent futures for March 2026 delivery were trading on the ICE at $61.33/bbl on Dec. 31, down from $62.14/bbl for front-month futures on Dec. 24.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $59.34/bbl on Dec. 29. Spot prices had settled at $59.40/bbl on Dec. 22, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, Dec. 29 (Dec. 22), EIA

New York Harbor: $2.16 per gallon ($2.18/gal)

Gulf Coast: $2.00/gal ($1.97/gal)

Los Angeles: $2.11/gal ($2.06/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices December 31, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format. *ExxonMobil prices obtained indirectly.

**Rerefiner