Market attention turned to surging crude oil and feedstock prices this week, as the higher values were anticipated to place upward pressure on base oil postings. This condition fueled expectations that buyers would try to beat potential price revisions and place fresh orders over the next few days. However, activity remained disappointingly sluggish given uncertainties in downstream lubricant segments, with most base oil requirements being met as supplies remained plentiful. Participants agreed that any price adjustments would be premature as values lacked demand-driven support.

Oil prices surged early in the week given new international sanctions on Russian crude oil shipments and tankers–measures that were expected to curb supply to China and India, as well as shipping operations to other destinations. According to Reuters, the U.S. Treasury imposed sanctions on Russian oil producers Gazprom Neft and Surgutneftegas and on 183 vessels that have shipped Russian oil, in hopes of cutting the revenues Moscow has used to fund its war on Ukraine. These measures will likely force Chinese and Indian refiners to source more crude from the Middle East, Africa and the Americas, pushing up oil prices and freight costs, according to analysts. Colder than normal weather in the Northern Hemisphere is also driving an uptick in heating fuels demand.

At the same time, the oil upswing was somewhat offset by the potential negative impact on global demand from trade tariffs promised to be imposed by U.S. president-elect Donald Trump. According to a Bloomberg report, the Trump administration is considering gradual tariff hikes after declaring a national economic emergency. The plan would start off with low-level tariffs to mitigate any immediate inflationary shock, but would then see monthly increments. The 25% tariff originally discussed was considered to be a major inflationary trigger for the U.S. and would derail any Federal Reserve room for additional interest rate cuts this year, analysts said.

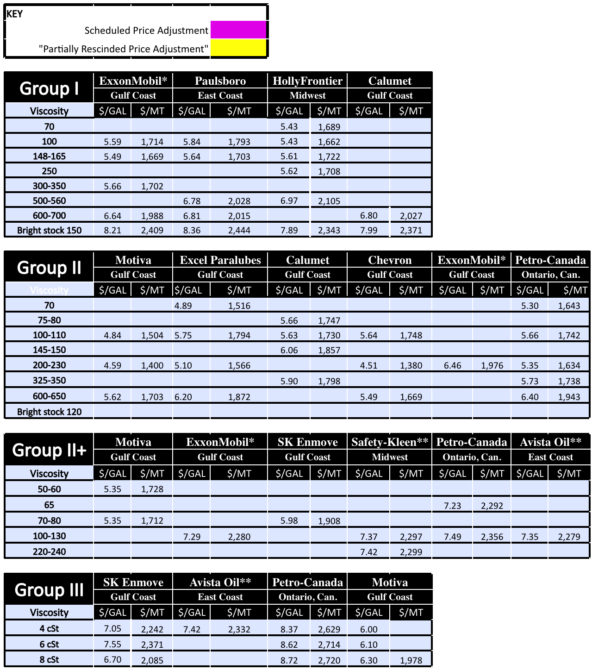

Despite pressure from the feedstock side, base oil postings remained stable. The API Group I grades were on the tight side given current domestic capacity against steady demand from both the local and export fronts. Bright stock values were particularly firm given strained supply levels.

While there had been some expectations of increased buying interest for most grades after the holidays, suppliers acknowledged that they had not observed much renewed activity this week, but rather anticipated demand to gradually ramp up ahead of the start of the spring season in late February or early March.

Group II supplies were deemed more than adequate to cover the current call for product, but a couple of suppliers indicated low availability of Group II 100N. At least one supplier maintained balanced conditions on 600N and had some length on 220N.

There could be tighter conditions ahead as a couple of plant turnarounds were on the horizon. There was also some concern about freezing weather along the U.S. Gulf Coast, which had forced some producers to reduce operating rates last week and may also have an impact this week as another extreme cold front approached.

Chevron was expected to start building inventories to meet requirements during a scheduled three-week turnaround at its Pascagoula, Mississippi, Group II plant, starting in March 2025. The turnaround may lead to a tightening of spot Group II supplies, sources speculated. The producer does not disclose details about its plant operations.

Calumet will also be completing a two-week maintenance program on one of its units in Shreveport, Louisiana, in the second half of February. The Shreveport refinery produces Group I and Group II base oils. The producer plans to have ample inventory to cover orders during maintenance, a company source said.

Motiva will be conducting a two-month turnaround at its refinery in Port Arthur, Texas, starting January 21. But the overhaul will only affect the fluid catalytic cracker and alkylation unit and should not impact base oil production, sources said.

It was also reported that while the fires raging in Los Angeles, California, had not directly threatened refineries in that state, several pipelines might be shut down, cutting off supplies of crude oil, natural gas, gasoline and diesel to not only California, but other states as well. This could also lead to a buildup of products at refineries, which might be forced to reduce their operating rates to control inventory.

Meanwhile, availability of Group III grades was adequate to long in North America, with the 4 cSt grade still deemed the most plentiful compared to the 6 cSt and 8 cSt cuts, exerting downward pressure on price ideas. This base oil category is particularly exposed to the weakness associated with automotive lubricant demand, and was therefore less likely to see a significant increase in consumption levels in the short term.

U.S. suppliers continued to look for export opportunities, but business was partly dampened by increased offer levels as producers felt less pressure to lower inventories because many had managed to do so in the fourth quarter of 2024. “We are starting to see export offers from the U.S. rise in price just a little, not near enough to cover the higher crude costs,” a source noted.

There was some buying interest noted in Mexico and Brazil. Buyers in both countries were expected to return to the market to replenish stocks, which had likely been depleted in the run-up to the year-end holidays. However, unlike their Mexican counterparts, Brazilian consumers had the option to secure domestic product as most base oil plants were running in Brazil and buyers would be less exposed to currency exchange fluctuations against the dollar. A 2,900-metric ton cargo was mentioned as having been booked from the U.S. Gulf to Rio de Janeiro, Brazil, between January 1 and 5, and discussions about other cargoes were ongoing.

Buying appetite for Group I cargoes was also seen in Europe and Africa, but tight domestic availability thwarted the conclusion of business, following some transactions in December.

On the naphthenic base oils side, producers were also keeping an eye on crude oil prices. Pale oil values remained steady, with additional support for the lighter grades coming from robust demand from the transformer oil and other segments servicing current infrastructure projects. The heavier grades were longer due to a seasonal slowdown, but there was still buying interest from export markets.

In industry-related news, a potential strike of the International Longshoremen’s Association that was due to start on January 15 and threatened to shut down ports along the East and Gulf coasts appears to have been averted as the union and the U.S. Maritime Alliance of ports and shipping companies reached a tentative agreement for a six-year contract on January 8.

Crude and Diesel

The U.S. Energy Information Administration (EIA) revised up its forecast for crude oil prices for 2025 as it weighed the impact of relatively lower global oil inventories in the first quarter of the year, given ongoing OPEC+ production cuts. The agency forecasts that declining global oil inventories will push up crude oil prices by $2 per barrel from their December 2024 average to an average of $76/bbl in the first quarter of 2025.

Crude oil futures were largely steady on Wednesday morning, after falling the previous day, as slipping U.S. crude stockpiles and expectations of supply disruptions from sanctions on Russian exports and tankers lent support to prices, counteracting expectations of softer global fuel demand.

On January 14, West Texas Intermediate February 2025 futures settled on the Nymex at $77.50/bbl, compared with $74.25/bbl on January 7.

Brent futures for March 2025 delivery were trading on the ICE at $79.83/bbl on January 14, from $77.33/bbl on January 7.

Louisiana Light Sweet crude wholesale spot prices were hovering at $82.07/bbl on January 13, from $76.56/bbl on January 6, according to the U.S. Energy Information Administration (EIA).

Low sulfur diesel was at $2.53/gal at New York Harbor, $2.45/gal on the Gulf Coast and $2.58/gal in Los Angeles on January 13, compared with $2.36/gal, $2.28/gal and $2.42/gal, respectively, on January 6, according to the EIA.

Contact Gabriela Wheeler directly at gabriela@lubesngreases.com

Posted paraffinic base oil prices: January 15, 2025 (FOB basis, USD/gallon and USD/metric ton)

Lubes’n’Greases Publications shall not be liable for commercial decisions based on this report.

Archived reports are here. Historic and current base oil pricing spreadsheets available to buy here.