While the number of vessels allowed to transit the Strait of Hormuz has increased, a recent artillery strike by Iran on a commercial ship and the United States’ attacks on Iran in response to the strike underscored the fragility of the current ceasefire and deepened the volatility of crude oil pricing. Following the signing of a memorandum of understanding the previous week, crude oil prices had plummeted to pre-war levels, but have moved up again as crude flows from the Middle East were still constrained. No fresh base oil posted price announcements emerged in the U.S. this week, marking only the second week of price stability since the start of the U.S.-Israel-Iran war.

Once again, suppliers reiterated that blenders’ priority appeared to be access to supplies, particularly to API Group III base oils since these grades showed global shortages, and there was no indication as to when shipments from producers on the Persian Gulf would resume. But the tight supply conditions were present in all segments of the base oils market, with suppliers maintaining strict sales controls and allocations.

At the 18th ICIS Base Oils and Lubricants Conference in Singapore last week, experts also pointed out that refineries in many countries had so far been able to run at close to full rates because of existing strategic crude stocks, but these seemed to be close to depleted, which meant that refined product shortages could become even more pronounced in the coming weeks. Asia is particularly vulnerable to Middle East supply shortages as a majority of refineries — with the exception perhaps of the refinery in Malaysia and a few others — were built to run on Middle East crude slates. Some countries have managed to import crude oil from other sources, but yields varied and cargoes were being used up quickly.

While a number of crude oil producers in the Middle East that had shut down production have restarted operations, they would be unable to ship out products if the strait does not return to normal operating conditions soon. For instance, Kuwait and Iraq were heard to have ramped up oil production in the last few days, but shipments will remain trapped if additional vessels cannot traverse the strait.

There were also reports that at least one Middle East base oil producer, ADNOC, had ramped up Group II and Group III production in Abu Dhabi, hoping that shipments would resume shortly. The producer was understood to have been running its base oil plant at reduced rates to support its own downstream lubricant production since March, but was trying to build up stocks to restart export activities. Confirmation about the company’s output and operations could not be obtained directly from the producer.

Meanwhile, much attention focused on the situation at the Shell Qatar Pearl gas-to-liquids (GTL) plant in Ras Laffan, Qatar, one of the largest base oils plants in the world with the capacity to produce about 30,000 barrels per day. A fatal explosion that occurred last week at the Ras Laffan energy complex, killing thirteen people and injuring several others, appeared to have been contained to a smaller gas processing plant, but did not directly impact QatarEnergy’s liquefied natural gas facilities, according to sources. The QatarEnergy refinery supplies feedstocks to the Pearl GTL plant, and the gas supplier had shut down operations after the accident last week as a precautionary measure. Media reports suggested that QatarEnergy had extended a force majeure notice, postponing the shipment of several liquified natural gas (LNG) cargoes until early September. QatarEnergy issued its first force majeure declaration in March, after the Iranian missile attacks damaged two LNG-producing trains at Ras Laffan on March 18.

At least one of the trains at the Shell Qatar Pearl base oil plant had already been shut down following the Iranian missile strike on the Ras Laffan complex in March, and damages were anticipated to take several months to a year to be repaired, according to sources.

While the situation at the Middle East plants were more concerning to Group III market participants, they also affected the Group II segment because many blenders have resorted to using more Group II as a Group III substitute whenever formulations allowed, leading to a further tightening of Group II supplies.

Another source of concern in the U.S. was the start of the hurricane season along the U.S. Gulf Coast, which typically prompts efforts to build extra stocks to cover requirements in case of production disruptions due to severe weather. This year, both buyers and sellers have entered the season with few, if any, extra supplies, sources warned.

Participants also kept a close watch on crude oil prices, with West Texas Intermediate hovering near $70 per barrel this week, reflecting a dramatic drop from levels around $119/bbl in early March.

Group I and Group II

The pace of base oil price adjustments has slowed down, partly because of lower crude oil and feedstock prices, but also because of difficulties on blenders’ side to absorb the steep prices. Many base oil consumers faced issues in securing volumes at current levels because of credit limitations and cash flow constraints, coupled with challenges in offsetting the higher production costs as lubricant price increases have proven difficult to implement. This has led to some demand erosion. Nevertheless, suppliers also mentioned that negotiations were not so much focused on pricing but rather availability, with some sellers noting that a few buyers appeared willing to secure cargoes even at the prevailing price levels.

Some buyers preferred to postpone orders until prices stabilized, while others had no choice but secure available base oil cargoes at current prices to keep operations running. Despite the unremitting hurdles, a majority of sources reported strong demand from most lubricants and grease segments.

While buyers had hoped that the softer crude oil prices would exert downward pressure on base oil prices, the extremely tight supply and demand fundamentals were expected to continue placing upward pressure on prices, particularly as some suppliers and consumers were striving to build inventories during the hurricane season. Refiners also noted that there was a need to maintain a certain price level to justify base oil production versus that of fuels.

A majority of U.S. suppliers have implemented strict sales controls and allocations for contract customers and were able to offer very few spot volumes, with some inquiries from Europe and Latin America having to go unfulfilled. At the same time, Group I and Group II availability in Asia has improved, and spot offers were heard to have emerged from Northeast Asia, Southeast Asia and India.

There continued to be reports of very tight fundamentals for the Group I SN500-600 and bright stock, particularly as the latter is a difficult grade to replace and there has been strong offtake from industrial and marine applications. A key producer was heard to have encountered some difficulties in supplying bright stock for export to Mexico.

On the other hand, the light grades were the ones that exposed the tightest conditions in the Group II segment, particularly as some blenders have increased the use of Group II light grades to replace Group III cuts in some applications.

Recent and ongoing scheduled turnarounds have exacerbated the tight supply situation in the U.S. Chevron’s Pascagoula, Mississippi, Group II plant was expected to have started a turnaround in early June and restart the plant by the end of the month. The producer was anticipated to have built inventories to meet contract commitments ahead of the outage, restricting its spot availability. No confirmation was available from Chevron as the producer does not comment on its plant operations.

Rerefined base oils have attracted the spotlight in recent weeks as many buyers have turned to rerefined oils whenever virgin base oils were unavailable. Sources said that this has allowed for more consumers to try rerefined oils and realize that their quality is on par with virgin oils, leading to increased acceptance.

Buying interest from South America and Mexico, as well as from Europe and Africa, continued to crop up, but spot supplies from the U.S. were very limited. Offers from South Korea, China and India have emerged as supply in Asia has grown, but steep freight and complicated logistics posed some issues.

Group I grades in Brazil remained snug as a production outage at Brazilian producer Petrobras’ plant back in February continued to be felt, particularly on the heavy-viscosity base oils and bright stock. A planned turnaround that started in mid-June may compound the ongoing supply tightness. Domestic prices have edged up in line with international prices and to reflect the current tight conditions.

In Mexico, there was significant interest in the heavy-vis grades and bright stock, but players expressed frustration at the difficulties locating product as spot supplies were minimal in the U.S. and prices were soaring. Some buyers said they hoped that additional offers from Asia might help fill some of the supply gaps, but high freight rates and long delivery times were still seen as potential roadblocks.

Group III

Given the lack of supplies of Group III base oils from the Middle East, Group III shortages caused much anxiety among blenders as these grades are difficult to replace. Some options such as polyalphaolefins were also tight and prices have skyrocketed, sources noted. The situation seemed to affect Group III consumers worldwide, but in the U.S., supplies were particularly tight because domestic production is small compared to demand. Group III suppliers from Asia and Canada were trying to fill the vacuum left by Middle East Group III supplies, but exports from these sources were not deemed sufficient to bridge the gap left by the absence of Middle East base oils, which meet almost 43% of U.S. demand. South Korea supplies roughly 30% of U.S. premium base oil imports.

Additional Group III capacity in the U.S. was not expected to come on-stream until later this year. Chevron has announced that new API Group III+ base oil capacity at its base oils plant in Pascagoula, Mississippi, will come to the market starting in the fourth quarter of 2026. ExxonMobil also expects to bring a major Group III base oil expansion on stream at its Baytown, Texas, complex, but not until 2028. No further details were forthcoming from either producer.

Despite the fact that additional vessels were heard to have transited the Strait of Hormuz over the past week following the memorandum of understanding and a 60-day ceasefire, most tankers remained trapped in the Persian Gulf, and ship owners and operators were still concerned about potential attacks and mines in the channel. This situation was not expected to improve overnight, delaying base oil shipments from plants in Abu Dhabi, Qatar and Bahrain even if those units were running at full rates. As it is, some of the facilities suffered damages from drone attacks and at least one train at the Shell Qatar Pearl unit was not expected to come back online for several months.

The ADNOC plant in Abu Dhabi was understood to have started ramping up production as mentioned above, but it may take some time for the producer to build inventories and for regular export shipments to resume. The U.S. distributor of ADNOC base oils had continued to partially meet contract commitments because it had been able to ship out a large cargo from Abu Dhabi before the conflict broke out, and it had placed customers on strict allocation. The supplier continued to ship product from alternative locations, and was working on receiving permission for a vessel to traverse the strait, but its stocks were expected to be low until fresh cargoes arrived.

Most customers that have contracts with South Korean suppliers continued to receive product, but allocations were in place and spot supplies were unavailable. A South Korean Group III supplier has received several inquiries for product from buyers who are not regular customers, but it was unable to supply all the extra requirements and has had to turn business away.

Asian plants have increased output rates since refiners have been able to import crude from sources outside the Middle East, but refining yields were not expected to be optimum as most refineries in Asia were built to run on Arab crude slates, with the exception of a few refineries. A key South Korean Group III producer has been able to continue running its plant at high rates, even after the start of the Iran war, as it has diversified its crude sources over the last few years and is able to source crude oil from Southeast Asia and other origins.

Some blenders have turned to rerefined Group III base oils to meet their requirements, and rerefiners were mostly sold out as well, but rerefined capacity is still comparatively limited in the U.S. and many blenders have strict approvals linked to specific suppliers so they cannot easily replace base oils.

While U.S. Group III producers were running plants at high rates, their current capacity does not have a significant impact on the general market because most of their output is used for internal lubricant production or has been allocated for contract business. Chevron started a turnaround at its Pascagoula, Mississippi, Group II/Group III plant in June, and the producer was anticipated to have built inventories ahead of the outage.

Naphthenic Base Oils

Naphthenic base oil prices were steady, despite sharp crude oil price fluctuations over the last two weeks. Several increases had emerged since the start of the Iran war, but no adjustments have surfaced in recent weeks, with producers noting that they had attained reasonable margins and would continue to monitor conditions in crude markets, hoping that an end to the conflict in the Middle East would help stabilize oil futures. Since conditions were still fragile, they felt that any small incident could tilt prices in either direction and adjustments may prove to be premature.

While the base oil supply crunch seen on the paraffinic side appeared to be less pronounced on the naphthenics side, suppliers said that demand for the light grades had been robust and at least one refiner was heard to be sold out of the pale 40, 60 and 100 grades. Most suppliers noted balanced conditions for the remaining grades, with no shortages noted. Suppliers also mentioned an uptick in consumption of pale oils to replace paraffinic grades given supply shortages, but added that unfortunately, naphthenic grades could not alleviate the shortage of base oils used in automotive applications.

Importers in Asia also said that naphthenic base oil cargoes from the U.S. continued to be shipped regularly and no disruptions had been noted. Most refineries in the U.S. have been partly insulated from crude supply shortages as they run on domestic crude oil, unlike most Asian refineries which were built to run on Middle East crude slates, although some refineries on the West Coast, East Coast and U.S Gulf Coast do require medium-sour grades from Saudi Arabia, Iraq, United Arab Emirates, and Kuwait.

Lubricant Increases

Lubricant manufacturers have implemented price increases to offset rising production costs over the last four months. Some suppliers have been successful at achieving the full intended amounts given concerns of potential shortages due to recent and ongoing supply disruptions. Some manufacturers have faced resistance, particularly as buyers were dealing with cash flow constraints and credit limitations against a backdrop of demand uncertainties in downstream markets.

Lubricant manufacturers have announced three round of increases, with effective dates peppered between April and the end of May. The markups have been driven by the mounting costs of base oils, additives, packaging and transportation over the last two months. Participants underscored that given current uncertainties and the fast pace of market changes — not to mention the escalating production costs — it remained very challenging to plan inventories and make pricing decisions.

Among the manufacturers that have announced various lubricant, grease and finished products increases were TotalEnergies USA, Highline Warren, Martin Lubricants, Omni Specialty Packaging, AOCUSA/Amalie, Calumet, CAM2, Castrol, Shell/SOPUS, PennStar, Chevron, ExxonMobil, Citgo, Phillips 66, Reliance Fluid Technologies, Consolidated Brands/ZXP Technologies and Valvoline. During the first two rounds of increases, suppliers had announced lubricant and grease increases of up to 9% to 35%, depending on the product, with some lubricant increases ranging 48 cents per gallon to $5/gal, and $0.07-0.11/lb for greases. The third round called for increases of up to 26% for most products from one supplier, and markups of $3.00/gal-$3.70/gal for synthetic oils, $2.40/gal-$2.60/gal for other oils, and $0.25/lb-$0.29/lb for greases from the rest of the suppliers.

Some manufacturers have been forced to reduce output given difficulties in transfering the higher production costs down the supply chain, coupled with base oil shortages, particularly of Group III cuts. Several OEM dealers were understood to be bracing for difficulties in fulfilling genuine motor oil demand given the current conditions. Dealers and distributors of a number of major automotive manufacturers received notifications of temporary motor oil supply shortages “due to production and logistics constraints within the global petrochemical supply chain,” one letter read. Even if the Strait of Hormuz were reopened tomorrow, the repercussions of the current supply disruptions were expected to be felt until next year. Some small blenders were considering closing their doors because of financial difficulties and credit limitations to purchase raw materials to keep operations running.

Middle East Base Oil Capacity Shutdowns

According to reports, Shell/Qatar Petroleum has halted production at one train of its Pearl GTL Group II/Group III facility in Qatar after sustaining damage during Iranian aerial attacks on March 19. The plant, which can produce 300,000 metric tons of Group II base oils and 1,072,000 tons of Group III base oils per year, was expected to remain offline for an extended period, possibly one year or longer as the specially designed equipment at the plant may be difficult to repair and may need to be replaced, according to sources. The explosion at a gas production unit in Ras Laffan Industrial City on June 21 has reportedly not impacted production at the QatarEnergy LNG refinery or the Shell Qatar Pearl unit, although QatarEnergy shut production down as a precautionary measure and has adviced customers of a delay in LNG shipments. QatarEnergy supplies feedstocks to the Pearl GTL unit.

Abu Dhabi state oil giant ADNOC shut part of its Ruwais refinery complex in response to a fire that broke out on March 10, following a drone strike. Sources indicated that while the Ruwais West refinery was shut down for inspection and safety reasons, other operations within the massive complex continued at reduced capacity. The trimmed base oil output was utilized for the company’s downstream lubricant production. The Ruwais complex houses a 600,000-tons-per-year Group II and Group III plant. According to reports, ADNOC was expected to ramp up base oil production in the next few days.

In Bahrain, fire erupted at BAPCO’s refinery in Maameer on March 5 following an Iranian attack, forcing the refinery to declare force majeure on production. BAPCO operates a 400,000-tons-per-year Group III base oil facility in Sitra, within the BAPCO refinery complex. BAPCO originally indicated that base oil production had been unaffected, but it was later heard that the producer had trimmed supply levels.

Crude Oil

Crude oil futures closed the month of June with significant declines on Tuesday, as traders monitored the potential resumption of negotiations between the U.S. and Iran in Qatar. Brent posted its biggest monthly decline since March 2020 (during the COVID pandemic) hovering near $72 per barrel. Analysts also worried about the drawdown in U.S. crude stocks, with estimates pointing at refiners drawing 4.5 million barrels of crude from storage last week.

- West Texas Intermediate August 2026 futures settled on the Nymex at $69.50 per barrel on June 30, down from $73.21/bbl for front-month futures on June 23.

- Brent September 2026 futures were trading on the ICE at $72.25/bbl on July 1, down from $73.47/bbl for front-month futures on June 24.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $73.12/bbl on June 29. Spot prices had settled at $76.15/bbl on June 23, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, June 29 (June 23), EIA

New York Harbor: $3.32 per gallon ($3.17/gal)

Gulf Coast: $3.30/gal ($3.16/gal)

Los Angeles: $3.38/gal ($3.24/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

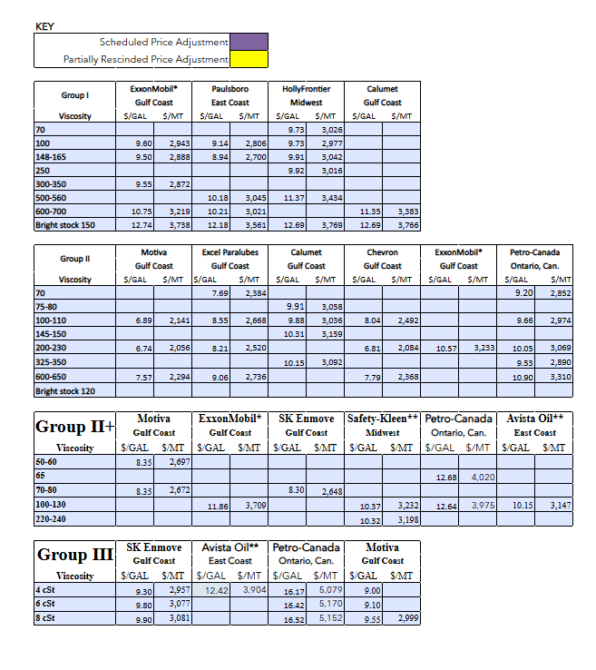

Posted Paraffinic Base Oil Prices

July 1, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner