The memorandum of understanding signed by the United States and Iran over the weekend ignited renewed hopes that ongoing hostilities in the Middle East would end and that the Strait of Hormuz would finally reopen. Crude prices immediately reacted to the news, with West Texas Intermediate falling to three-month lows below $80 per barrel–a sharp drop from levels around $119 in early March. However, the situation was still volatile, with reports that only a small number of vessels were allowed to transit the strait. Discussions at the 18th ICIS Base Oils and Lubricant conference taking place in Singapore this week focused on the current base oil supply constraints and the difficulties that the industry is likely to encounter before returning to more “normal” conditions.

U.S. base oil producers have implemented several rounds of posted price increases since the start of the Iran war, but no fresh announcements surfaced during the week. At this juncture, most participants acknowledged that the main market concern appeared to be availability, and not pricing, as most grades remained extremely tight, with API Group III grades expected to show the most critical deficiency on a global scale. Other grades were also tight and spot supplies were largely unavailable, while strict allocations were still in place.

Despite the fact that U.S. receives Group III base oils from several sources outside the Middle East, including Asia and Canada, these volumes are not sufficient to make up for the lack of Middle East Group III exports. Group III production remained trapped in the Persian Gulf due to the closure of the strait and damages at base oil plants following Iranian drone and missile attacks.

The situation could be potentially exacerbated by an explosion that occurred at the Rass Laffan energy refinery complex which housed the Qatar Energy refinery that supplies liquid natural gas (LNG) to the Shell Qatar Pearl GTL unit. Thirteen people were killed and dozens injured in an explosio at a gas processing facility inside the industrial complex, Qatar’s energy minister said on Monday. Qatar Energy’s liquefied natural gas facilities were not impacted by the blast, the minister added, but production had been shut down after the accident as a preventative measure.

At least one of the trains at the Shell Qatar Pearl base oil plant had already been shut down in March due to damages from Iranian strikes, and they were anticipated to take several months to a year to be repaired, according to sources. Rumblings also circulated that the company had scheduled a shutdown at the remaining train in September. On the other hand, ADNOC was heard to be preparing to restart base oil production in Abu Dhabi.

Even if the refineries in the Persian Gulf start to produce base oils in the next few weeks, there will be many logistical challenges to overcome, sources commented. Shipowners and operators are still hesitant to commit to voyages as mines have to be cleared from the Strait of Hormuz, and vessels are supposed to receive permission from Iran to cross the strait. U.S. President Donald Trump said that a “hotline” would be set up for that purpose. Nevertheless, issues such as gathering a crew willing to sail to the Middle East, insurance availability for both the vessels and the cargoes, and rising costs were some of the challenges that producers and buyers were likely to face in the coming weeks.

Group I and Group II

The barrage of posted price increase announcements witnessed over the last four months seemed to have abated, with a number of suppliers implementing increases last week and no fresh announcements emerging this week. The slowdown was partly attributed to lower crude oil and feedstock prices, but also to the fact that buyers were not as eager to secure product at the current price levels. However, participants also admitted that the focus of negotiations was not pricing but rather availability, with some suppliers still noting some panic buying as blenders worried about shortages in the coming weeks.

Yet some blenders have already had to reduce base oil purchases and operating rates because of credit limitations and cash flow constraints, coupled with difficulties in offsetting the higher production costs through lubricant price increases. Sources said that the high base oil prices were stifling demand. Some buyers were deferring orders until a steadier price scenario emerged, while others had no choice but secure available base oil cargoes at current price levels to keep operations running. A majority of sources reported strong offtake from the lubricants and grease segment.

Buyers were hoping that the falling crude oil prices seen of late would exert downward pressure on base oil prices, but the extremely tight supply and demand ratio was likely to continue placing upward pressure. Refiners also need to justify base oil production versus that of fuels by ensuring that margins remain robust.

Base oil suppliers mentioned concerns about not being able to build stocks to cover potential output disruptions during hurricane season. The first severe weather system, Tropical Storm Arthur, hit areas along the U.S. Gulf Coast last week, but fortunately did not cause substantial damage. Spot supplies continued to be minimal, with only a few cargoes heard to have been offered to Europe and Latin America in recent weeks, and U.S. suppliers maintaining strict sales controls and allocations for contract customers.

Within the Group I category, bright stock and SN500-600 reflected the tightest conditions. A key producer was heard to have encountered some difficulties in supplying bright stock for export to Mexico. Group II light-viscosity cuts were generally limited as well, particularly as Group II light grades were being used as a substitute for Group III cuts in some applications.

There have been reports of South Korean and Chinese suppliers offering cargoes to the U.S. and Latin America as supply levels have started to improve in Asia, while the steep prices had resulted in some demand destruction as the region is very price sensitive. Offers for Group II and Group III shipments from India have also emerged, even though Indian domestic production is not deemed sufficient to meet the country’s base oil demand.

Despite the possibility of importing Asian material, recent and ongoing scheduled turnarounds may exacerbate the tight supply situation in the U.S. Chevron’s Pascagoula, Mississippi, Group II plant was expected to have started a turnaround in early June and restart the plant by the end of the month. The producer was anticipated to have built inventories ahead of the outage, restricting its spot availability even further. No confirmation was available from Chevron as the producer does not comment on its plant operations.

Rerefined base oils were also tight given strong demand from contract customers and from buyers who were unable to receive extra supplies from virgin base oil suppliers, although rerefiners have mentioned very limited spot availability.

There continued to be buying appetite for Group I grades in Brazil as a production outage at Brazilian producer Petrobras’ plant back in February has prolonged the snug Group I supply situation, particularly of the heavy-viscosity base oils and bright stock. A planned turnaround that started in mid-June may compound the ongoing supply tightness. Supplies from Asia have been offered to Brazilian buyers as well, but consumers were also seeking U.S. supplies.

In Mexico, demand for the heavy-vis grades and bright stock grades was strong and buyers were having difficulties locating enough barrels as product has been quite tight in the U.S. Consumers acquiesced to higher prices in line with export markets in Latin America and Europe. Additional offers were anticipated to emerge from Asia as the tight supply situation there has started to ease.

Group III

Group III supplies have reached critical levels for many blenders, and there is little relief in sight because flows from the Middle East will likely take several weeks to resume, even if the Strait of Hormuz were completely reopened tomorrow. As it stands, only a limited number of vessels are currently traversing the chokepoint and many ships are still trapped in the Persian Gulf.

Furthermore, most Group III base oil production in Qatar, Bahrain and Abu Dhabi has seen disruptions due to Iranian drone attacks on several refineries, with repairs being carried out, and suppliers of base oils manufactured in Qatar and Bahrain remaining under force majeure.

A bright spot this week was a report that the ADNOC plant in Abu Dhabi was preparing to restart production over the next few days, but it may take some time for the producer to build inventories and for regular shipments to resume. The U.S. distributor of ADNOC base oils had continued to partially meet contract commitments because it had been able to ship out a large cargo from Abu Dhabi before the conflict broke out, and it had placed customers on strict allocation. The supplier continued to ship product from alternative locations, but its stocks were believed to be close to depleted and like small drops unable to quench the growing thirst for Group III supplies in the U.S.

A Group III supplier has received numerous requests for product from buyers who are not regular customers, but it was unable to supply all the requirements and has had to turn business away. The dire supply situation was not expected to improve any time soon. “I don’t think there is any hope for relief within 2026,” a source conceded, while another mentioned severe disruptions in lubricant supplies to OEMs around the world given the lack of Group III supplies and polyalphaolefins.

Group III suppliers from Asia and Canada were doing their utmost to fill the vacuum left by Middle East Group III supplies, but even in the best of times, production from other sources was not deemed sufficient to bridge the gap left by the absence of Middle East base oils, which fulfill almost 43% of U.S. demand.

While Asian plants have increased output rates since refiners have been able to import crude from sources outside the Middle East, they have had to meet term commitments in Asia and the U.S. and have been unable to offer much spot availability. Refining yields were also expected not to be optimum as most refineries in Asia were built to run on Arab crude slates.

A key South Korean Group III producer had been able to continue running its plant at high rates, even after the start of the Iran war, as it has diversified its crude sources over the last few years and is able to source crude oil from Southeast Asia and other origins. Even so, suppliers are barely able to meet contract commitments and have very little extra product to offer for spot business.

Some blenders have turned to rerefined Group III base oils to meet their requirements, but rerefined capacity is still comparatively limited in the U.S.

While U.S. Group III producers were running plants at high rates, their output does not have a big impact on the general market because most of their output is used for internal lubricant production or has been allocated for contract business. Chevron started a turnaround at its Pascagoula, Mississippi, Group II/Group III plant in June, and the producer was anticipated to have built inventories ahead of the outage. Chevron has announced plans to start Group III+ production in Pascagoula, but commercial production will not be available before the end of 2026.

ExxonMobil also expects to bring a major Group III base oil expansion on stream at its Baytown, Texas, complex, but not until 2028. No further details were forthcoming from either producer.

Naphthenic Base Oils

Despite volatility in upstream segments, prices in the naphthenic segment were generally stable, although participants continued to watch the latest geopolitical developments in the Middle East since it may take some time before crude exports from the region go back to pre-war levels and base oil flows also resume.

Naphthenic base oil suppliers said they had seen a surge in demand over the last few weeks, partly attributed to the fact that some paraffinic grades were being replaced with pale oils given the scarcity affecting the paraffinic segment. Pale oil supplies were deemed sufficient to cover most requirements, and no shortages were reported. Buyers in Asia also said that naphthenic base oil cargoes from the U.S. continued to be shipped regularly and no disruptions had been noted.

Demand for the heavy grades from the rubber and tire segments had started out the summer on the lackluster side, but buying activity has taken off after the summer driving season got officially underway in late May. The lighter grades continued to see strong consumption from the transformer oil segment and have also been exported to markets which offered attractive margins such as Europe. Most refineries in the U.S. have been insulated from crude supply shortages as they run on domestic crude oil, unlike most Asian refineries which were built to run on Middle East crude slates.

Lubricant Increases

Lubricant manufacturers have implemented price increases to offset rising production costs over the last four months. Some suppliers have been successful at achieving the full intended amounts given concerns of potential shortages due to recent and ongoing supply disruptions. Some manufacturers have faced resistance, particularly as buyers were dealing with cash flow constraints and credit limitations against a backdrop of demand uncertainties in downstream markets.

Lubricant manufacturers have announced three round of increases, with effective dates peppered between April and the end of May. The markups have been driven by the mounting costs of base oils, additives, packaging and transportation over the last two months. Participants underscored that given current uncertainties and the fast pace of market changes—not to mention the escalating production costs–it remained very challenging to plan inventories and make pricing decisions.

Among the manufacturers that have announced various lubricant, grease and finished products increases were TotalEnergies USA, Highline Warren, Martin Lubricants, Omni Specialty Packaging, AOCUSA/Amalie, Calumet, CAM2, Castrol, Shell/SOPUS, PennStar, Chevron, ExxonMobil, Citgo, Phillips 66, Reliance Fluid Technologies, Consolidated Brands/ZXP Technologies and Valvoline. During the first two rounds of increases, suppliers had announced lubricant and grease increases of up to 9% to 35%, depending on the product, with some lubricant increases ranging 48 cents per gallon to $5/gal, and $0.07-0.11/lb for greases. The third round called for increases of up to 26% for most products from one supplier, and markups of $3.00/gal-$3.70/gal for synthetic oils, $2.40/gal-$2.60/gal for other oils, and $0.25/lb-$0.29/lb for greases from the rest of the suppliers.

Some manufacturers have been forced to reduce output given difficulties in transfering the higher production costs down the supply chain, coupled with base oil shortages, particularly of Group III cuts. Several OEM dealers were understood to be bracing for difficulties in fulfilling genuine motor oil demand given the current conditions. Dealers and distributors of a number of major automotive manufacturers received notifications of temporary motor oil supply shortages “due to production and logistics constraints within the global petrochemical supply chain,” one letter read. Even if the Strait of Hormuz were reopened tomorrow, the repercussions of the current supply disruptions were expected to be felt until next year. Some small blenders were considering closing their doors because of financial difficulties and credit limitations to purchase raw materials to keep operations running.

Middle East Base Oil Capacity Shutdowns

According to reports, Shell/Qatar Petroleum has halted production at one train of its Pearl GTL Group II/Group III facility in Qatar after sustaining damage during Iranian aerial attacks on March 19. The plant, which can produce 300,000 metric tons of Group II base oils and 1,072,000 metric tons of Group III base oils per year, was expected to remain offline for an extended period, possibly one year or longer as the specially designed equipment at the plant may be difficult to repair and may need to be replaced, according to sources. The explosion at a gas production unit in Ras Laffan Industrial City on June 21 has reportedly not impacted production at the Qatar Energy LNG refinery or the Shell Qatar Pearl unit. Qatar Energy supplies LNG feedstock to the Pearl GTL unit.

Abu Dhabi state oil giant ADNOC shut part of its Ruwais refinery complex in response to a fire that broke out on March 10, following a drone strike. Sources indicated that while the Ruwais West refinery was shut down for inspection and safety reasons, other operations within the massive complex might be continuing at reduced capacity. The Ruwais complex houses a 600,000 metric-tons-per-year Group II and Group III plant. According to reports, ADNOC was expected to restart base oil production in the next few days.

In Bahrain, fire erupted at BAPCO’s refinery in Maameer on March 5 following an Iranian attack, forcing the refinery to declare force majeure on production. BAPCO operates a 400,000 tons-per-year Group III base oil facility in Sitra, within the BAPCO refinery complex. BAPCO originally indicated that base oil production had been unaffected, but it was later heard that the producer had trimmed supply levels.

Crude Oil

Crude oil futures fell on Wednesday on expectations of gradually increasing traffic through the Strait of Hormuz. Brent crude prices fell more than $3 per barrel to their lowest level since before the start of the Iran war.

- West Texas Intermediate August 2026 futures settled on the Nymex at $73.21 per barrel on June 23, down from $76.05/bbl for front-month futures on June 16.

- Brent August 2026 futures were trading on the ICE at $73.47/bbl on June 24, down from $79.63/bbl for front-month futures on June 17.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $76.15/bbl on June 23. Spot prices had settled at $81.32/bbl on June 16, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, June 23 (June 16), EIA

New York Harbor: $3.17 per gallon ($3.21/gal)

Gulf Coast: $3.16/gal ($3.15/gal)

Los Angeles: $3.24/gal ($3.25/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

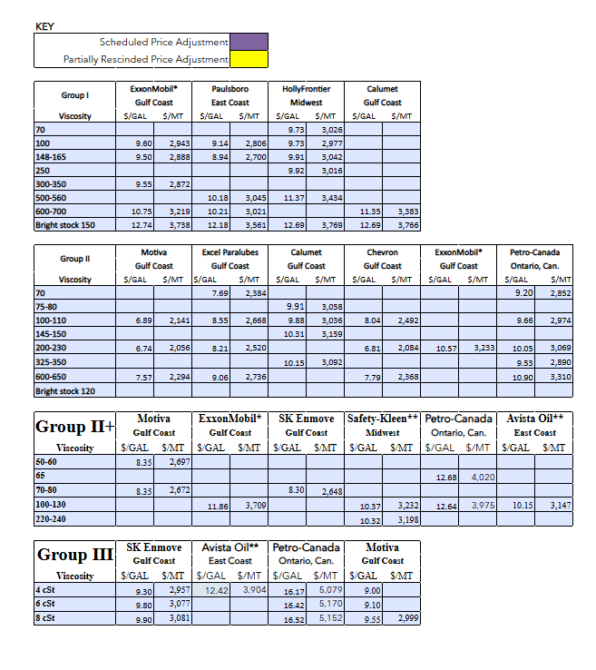

Posted Paraffinic Base Oil Prices

June 24, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner