Base oil prices continued to be exposed to upward pressure from steep crude oil prices, as flows from the Middle East remained constrained by the nearly complete closure of the Strait of Hormuz and by reduced output in the Persian Gulf. Various U.S. suppliers have adjusted up posted prices since the beginning of the Iran conflict on an almost weekly basis, with Motiva stepping out with a fresh round of increases this week. However, price revisions have slowed, with participants speculating that base oil values may have peaked as buyers seem unable to absorb further markups and there is a risk of significant demand destruction. Most base oils remained in tight supply in the U.S., but the API Group III segment showed the most blatant market imbalance as supplies from the Middle East were largely absent, while Asian and domestic producers have implemented allocations and offered little extra availability.

Crude oil prices had cooled off the previous week on expectations of a peace deal in the Middle East as U.S.-Iran negotiations had resumed, but diplomatic efforts appeared to have been abandoned after both countries exchanged strikes on military and telecommunications facilities, driving oil prices up again. West Texas Intermediate and Brent futures rose by more than 2% on Wednesday, extending gains from the previous session.

U.S. refiners have been partly insulated from the Middle East oil supply disruptions because they are able to run refineries on U.S. crude slates and oil imported from Mexico, Canada and Venezuela, but the reduced global crude availability has forced most countries to tap into their national emergency stockpiles such as the U.S. Strategic Petroleum Reserve to bridge the supply gap. Executives from ExxonMobil and Chevron recently warned that oil prices could skyrocket over the next two months as oil stockpiles are being drained, according to several media outlets. The surging oil prices could cause demand to fall, increase inflation and trigger a global economic slowdown.

This scenario has already been partially playing out on the lubricants side of the business, where rising prices of both fuels and finished lubricants coupled with inflation, cash flow constraints and economic uncertainties have led to reduced consumer spending, including automotive maintenance. Millions of vehicle owners are delaying, skipping, or stretching intervals for basic tasks like oil changes due to the rising costs of finished products, insurance, and fuel. Independent repair shops, dealerships, and parts suppliers are all reporting signs that consumers are postponing preventative maintenance to cope with tighter household budgets, according to a report from NBC San Diego.

The maintenance slowdown was somewhat exacerbated by supply constraints affecting parts and fluids, with the Group III base oil shortages particularly affecting passenger car motor oil supplies. Some automakers have already warned dealerships and service centers about shortages involving specific service materials. Toyota and Nissan recently issued letters indicating that supplies of 0W-8 and 0W-16 motor oils were becoming strained.

Lubricant manufacturers were trying to implement lubricant and grease price increases to offset the mounting costs of base oils, additives, packaging and transportation since March. Suppliers reported robust lubricant consumption and reduced buyer resistance to the increases, which could be partly attributed to concerns about potential shortages and even higher prices in the coming months, with end-users building stocks now to avoid these issues at a later date. Some buyers were more conservative in terms of purchases as they anticipated the Iran war to end and refined products prices to go down.

Group I and Group II

Motiva communicated a posted price increase of 35 cents per gallon on its Group II base oils, and 50 cents/gal on its Group II+ and Group III grades, with the exception of the Group III 8 cSt cut, which was raised 75 cents/gal, with an effective date of June 1.

This announcement follows that of several other suppliers, including ExxonMobil, SK Enmove, Calumet, HF Sinclair, Excel Paralubes and Avista Oil during the previous two weeks. But there has been a definite slowdown in the number of increase announcements emerging each week, as it appears margins have improved slightly. Producers have turned more cautious to avoid further demand destruction as some blenders have reduced purchases because they are unable to absorb the rising production costs and they faced credit limitations to acquire additional base oils. To illustrate the challenging credit limits, a seller explained: “Back in February, if one of our customers bought four railcars per month, this represented about $450,000; now it represents almost $1 million.”

At the same time, there are medium-sized to large blenders who are willing to pay any price to secure base oils and keep operations running, sources conceded.

Aside from hefty crude oil prices, producers mentioned an extremely tight supply and demand balance as one of the factors driving the base oil increases. A majority of suppliers appeared to be able to meet contractual obligations, but have little spot availability to offer. Sales controls and allocations are still in place and this has driven some buyers to contact sellers that are not their regular suppliers to inquire about additional barrels. However, there are almost no extra supplies to be found. “Some people are finally realizing that there is not enough base oil for everyone,” a market source noted.

Within the Group I category, availability of bright stock and the heavy cuts was particularly strained, but the Group II cuts were also very limited, so much so that both buyers and sellers expressed concern about the difficulties in building any emergency stocks as the Atlantic Basin hurricane season got underway.

Recent and upcoming scheduled turnarounds in the U.S. may have exacerbated the tight supply situation. Motiva was heard to have completed a two-week partial turnaround at its Port Arthur, Texas, Group II/III plant in April, which mainly affected its mid-viscosity base oils. HF Sinclair’s Tulsa, Oklahoma, Group I unit also completed a maintenance program in April.

Additionally, Chevron’s Pascagoula, Mississippi, Group II/Group III plant was expected to start a turnaround in June, and the producer was anticipated to be building inventories ahead of the outage, restricting its spot availability even further.

Rerefined base oils have also tightened on the back of strong offtake from contract customers and rerefiners were unable to offer much spot availability.

The export situation as seen over the last three months persisted, with a majority of Group I and Group II suppliers largely unable to participate in export business. There have been reports of small cargoes moving to Brazil and Europe, with the arbitrage into Europe opening after a sharp increase in prices in that region amid restricted availability, since European refiners focused on contract obligations and fuel production.

There were expectations of increased Asian Group II and Group III cargoes becoming available for spot business as refining rates increase in that region and demand declines. Some cargoes may be headed to the U.S. and Latin America, although steep transportation costs have thwarted the conclusion of a few deals.

Demand for Group I grades from Brazil was still robust as a production outage at Brazilian producer Petrobras’ plant that started back in February has resulted in snug Group I supplies, particularly of the heavy-viscosity base oils and bright stock. A planned turnaround in June may compound the ongoing supply tightness. Some suppliers were heard to have implemented allocation measures for Group II grades to ensure supply to customers in the coming weeks. Base oil prices have surged because of the scarcity of spot supplies from the U.S. and Asia, although there were expectations that Asian refiners might have more availability in the coming weeks as refining rates were improving. Domestic Group I prices were heard to have been adjusted up by 40%, with buyers having few options but to accept the markups given the pervasive supply tightness.

In Mexico, there has been resistance to price increases for U.S. base oils, and some U.S. suppliers have halted exports temporarily, particularly of the light grades. The situation was slightly different for the heavy-vis grades and bright stock, since these cuts have been very difficult to obtain and consumers appeared willing to pay higher values in line with export markets in Latin America and Europe. Asian availabilities may become an alternative for Mexican consumers as supply levels are gradually increasing in that region, but Asian suppliers may also find other outlets that offer more attractive margins.

Group III

Most Group III base oils produced in the Middle East remained trapped in the Persian Gulf as Iran maintained its blockade of the Strait of Hormuz, although a very limited number of tankers was heard to have traversed the crucial waterway in recent days. However, there was no mention of fresh base oil cargoes being shipped from Qatar and Bahrain, and shipments from the United Arab Emirates have been reduced due to shipping constraints, although isotank volumes were reportedly moving out of ports on the Red Sea. Some of the Middle East suppliers had been able to continue meeting contract obligations by tapping stocks held in storage at various locations, but these stocks seem to be depleted. A supplier was heard to have implemented a strict allocation program.

Suppliers from other regions were heard to have received inquiries for additional cargoes as buyers were unable to receive shipments from the Middle East, and this situation may be extended beyond a reopening of the strait. There are expectations that even if shipments through Hormuz resumed, it would take about four months for 80% of pre-war flows of crude oil and refined products to restart, and full flows may not be achieved before 2027.

Asian base oil volumes moving to the U.S. and other destinations were expected to improve in the next few weeks. Asian refiners had trimmed output levels due to a lack of Middle East crude oil shipments moving to Asia and the need to prioritize fuel supplies. However, the situation appeared to be gradually improving as several countries have tapped into strategic emergency crude stocks to keep refineries running, or have imported crude oil from alternative sources such as Latin America, the U.S., Australia and Africa. Asian base oil demand was also heard to be weakening due to the extremely high prices, freeing up more volumes for export.

A key South Korean Group III producer had been able to continue running its plant at high rates and produce base oils to fully meet contract commitments as it has diversified its crude sources over the last few years, with the refinery able to handle alternative crudes much better than other refineries. Another Asian producer was expected to offer spot supplies of Group II grades, which some blenders may be able to use to replace Group III cuts in some applications.

In terms of domestic supplies, Group III producers focused on contract commitments and there was little spot availability as a result. The tight conditions may be exacerbated when Chevron starts a turnaround at its Pascagoula, Mississippi, Group II/Group III plant in June, and the producer was anticipated to be building inventories ahead of the outage, restricting its spot availability even further.

Naphthenics

Prices in the naphthenic segment were mostly stable, despite crude oil price fluctuations over the last couple of weeks. Producers have implemented several increases since March and were watching crude prices carefully, as naphthenic base oils are affected by crude price swings more directly than paraffinic oils. Most refiners were heard to be running base oil plants at full rates due to steady demand and improving margins.

The heavy grades have seen improved demand from the rubber and tire segments as the summer travel season got officially underway on Memorial Day on May 25. The lighter grades continued to see robust requirements from the transformer oil segment.

Lubricant Increases

Several lubricant manufacturers have announced a third round of increases, following two previous initiatives since March. The effective dates of the fresh increases range May 22-26. The markups have been driven by the mounting costs of base oils, additives, packaging and transportation over the last two months. Participants underscored that given current uncertainties and the fast pace of market changes — not to mention the escalating production costs — it remained very challenging to plan inventories and make pricing decisions.

Among the manufacturers that have announced various lubricant, grease and finished products increases were TotalEnergies USA, Highline Warren, Martin Lubricants, Omni Specialty Packaging, AOCUSA/Amalie, Calumet, CAM2, Castrol, Shell/SOPUS, PennStar, Chevron, ExxonMobil, Citgo, Phillips 66, Reliance Fluid Technologies, Consolidated Brands/ZXP Technologies and Valvoline. During the first two rounds of increases, suppliers had announced lubricant and grease increases of up to 9% to 35%, depending on the product, with some lubricant increases ranging 48 cents per gallon to $5/gal, and $0.07-0.11/lb for greases. The third round called for increases of up to 26% for most products from one supplier, and markups of $3.00/gal-$3.70/gal for synthetic oils, $2.40/gal-$2.60/gal for other oils, and $0.25/lb-$0.29/lb for greases from the rest of the suppliers.

While the original price hikes had met with buyer resistance, It was heard that the increases had gained some acceptance among consumers as supplies have tightened and there were concerns of more potential shortages if the war in the Middle East continued.

Some manufacturers have been forced to reduce output given difficulties in transfering the higher production costs down the supply chain, coupled with base oil shortages, particularly of Group III cuts. Several OEM dealers were understood to be bracing for difficulties in fulfilling genuine motor oil demand given the current conditions. Dealers and distributors of a number of major automotive manufacturers received notifications of temporary motor oil supply shortages “due to production and logistics constraints within the global petrochemical supply chain,” one letter read. Even if the Strait of Hormuz were reopened tomorrow, the repercussions of the current supply disruptions were expected to be felt until next year. Some small blenders were considering closing their doors because of financial difficulties and credit limitations to purchase raw materials to keep operations running.

Middle East Base Oil Capacity Shutdowns

According to reports, Shell/Qatar Petroleum has halted production at one train of its Pearl GTL Group II/Group III facility in Qatar after sustaining damage during Iranian aerial attacks on March 19. The plant, which can produce 300,000 tons of Group II base oils and 1,072,000 tons of Group III base oils per year, was expected to remain offline for an extended period, possibly one year or longer as the specially designed equipment at the plant may be difficult to repair and may need to be replaced, according to sources.

Abu Dhabi state oil giant ADNOC shut part of its Ruwais refinery complex in response to a fire that broke out on March 10, following a drone strike. Sources indicated that while the Ruwais West refinery was shut down for inspection and safety reasons, other operations within the massive complex might be continuing at reduced capacity. The Ruwais complex houses a 600,000-tons-per-year Group II and Group III plant. ADNOC has been able to ship product out through ports on the Red Sea, according to sources.

In Bahrain, fire erupted at Bapco refinery in Maameer on March 5 following an Iranian attack, forcing the refinery to declare force majeure on production. Bapco operates a 400,000-tons-per-year Group III base oil facility in Sitra, within the Bapco refinery complex. Bapco originally indicated that base oil production had been unaffected, but it was later heard that the producer had trimmed supply levels.

Crude Oil

Crude oil futures surged following a flare-up in hostilities between the U.S. and Iran, fanning fears of extended disruptions to energy flows. A larger-than-expected drawdown in U.S. crude inventories added further upward pressure.

- West Texas Intermediate July 2026 futures settled on the Nymex at $93.76 per barrel on June 2, slightly down from $93.89/bbl for front-month futures on May 26.

- Brent August 2026 futures were trading on the ICE at $97.16/bbl on June 3, up from $96.45/bbl for front-month futures on May 27.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $100.09/bbl on June 2. Spot prices had settled at $112.25/bbl on May 22, according to the U.S. Energy Information Administration. (There was no trading on May 25 due to the Memorial Day holiday in the U.S).

Diesel

Low-sulfur diesel wholesale, June 2 (May 22), EIA

New York Harbor: $3.69/gal ($3.83/gal)

Gulf Coast: $3.63/gal ($3.73/gal)

Los Angeles: $4.12/gal ($4.29/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

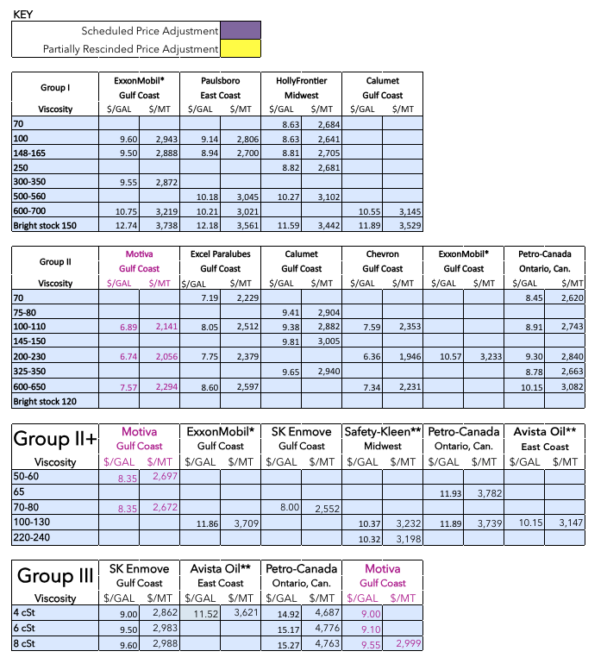

Posted Paraffinic Base Oil Prices June 3, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner