More base oil price increases emerged this week from producers ExxonMobil, Excel Paralubes, Paulsboro and San Joaquin Refining, which was not surprising given the vertiginous climb in crude oil and diesel prices and the tight global supply fundamentals. With the Iran war dragging on and no signs of it ending any time soon, and the Strait of Hormuz still closed to most traffic, a fifth of the world’s oil exports are still unable to reach their destinations. Many refineries in Asia are running at reduced rates and are focusing on fuel production, limiting base oil output, while a large portion of base oils produced in the Middle East remain trapped in the Persian Gulf, leading to significantly reduced global base oil supplies. The API Group III segment is the most affected by the current situation, but Group I and Group II base oils are also experiencing extremely strained conditions.

While the United States seems to be partly insulated from the crude oil supply disruptions as local refineries are mostly able to run on domestic crude and oil from other origins such as Canada, Mexico and Venezuela, the base oil market was still affected by the shortages in other regions because foreign buyers were anxious to obtain product, and U.S. export prices have risen, pushing domestic values up as a result. Most U.S. producers have been unable to offer volumes beyond those they need to fulfill contractual commitments, and spot supplies seemed to be drying up as existing inventories were being depleted.

Demand for U.S. crude oil has also increased as Asian refiners look to diversify their supplies given the disruptions of Middle East oil shipments. For example, a tanker carrying U.S. crude oil arrived in Japan on Sunday, marking the first oil shipment from the U.S. since the Iran war began in late February. Mexico has also agreed to supply Japan with one million barrels of crude oil. But it was also reported on Tuesday that Panama-flagged Japanese tanker Idemitsu Maru, carrying 2 million barrels of Saudi oil, crossed the Strait of Hormuz, becoming one of the very few ships that has been able to do so since the start of the conflict.

Crude oil futures jumped on Tuesday, April 28, on signs that U.S. president Donald Trump was reluctant to engage in negotiations with Iranian leaders, as he called off a trip of negotiators headed to Pakistan where discussions to end the war were expected to take place, and told his advisors that Iran’s latest proposal to open the strait was unacceptable. Iran offered to reopen the strait if the U.S. lifted its naval blockade, but suggested delaying discussions on its nuclear program to a later date. West Texas Intermediate futures surged by more than 3% to close at $99.93 per barrel, and Brent futures leaped over the $110/bbl mark to settle at $111.26/bbl.

Another shock to crude markets came when the United Arab Emirates announced that the country would be exiting the Organization of the Petroleum Exporting Countries (OPEC), dealing a heavy blow to the group at a sensitive time given the ongoing turmoil in energy markets. To reduce the dependence on the Strait of Hormuz in the future, Emirati officials have mentioned plans for new pipelines from the UAE’s oil fields in Abu Dhabi that would bypass the strait and allow crude to be shipped from the port of Fujairah.

Meanwhile, Iran has continued producing crude oil, but its storage tanks at Kharg Island were expected to be at capacity in the next few days, so producers were expected to resort to floating storage. However, they may have to shut in production, which would be placing economic pressure on Iran, but would also reduce the flow of much needed Middle East oil into the global market.

Paraffinic Base Oils — Group I and II

The steep crude oil prices and tightening global supplies prompted at least one U.S. base oil producer to announce price increases again this week, following several rounds since the start of the Iran war.

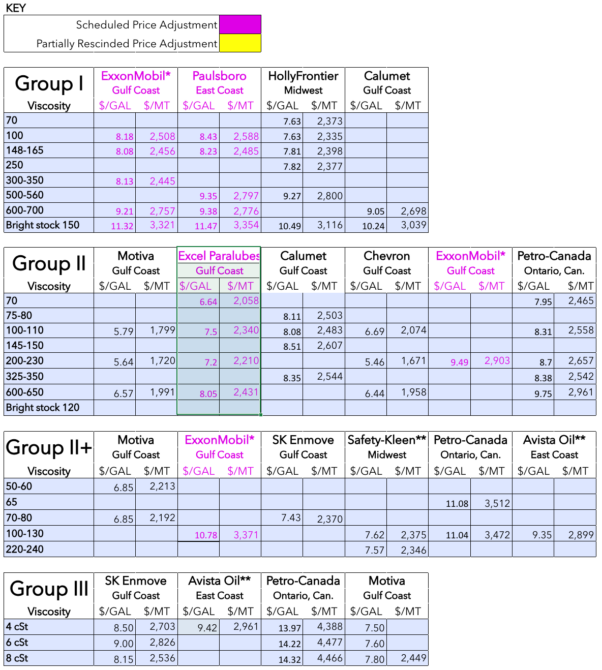

According to reports, ExxonMobil communicated posted price increases for all its base oils, which will go into effect on April 30. Except for the company’s Group I bright stock, which will be increased by 95 cents per gallon, all the producer’s Group I, Group II and Group II+ cuts will go up by 71 cents/gal.

Paulsboro was anticipated to implement a posted price increase of 71 cents/gal on all of its Group I grades, except its bright stock, which will be increased 95 cents/gal, as of May 5.

Excel Paralubes announced that the company would be increasing its Group II 70N and 110N grades by 70 cents/gal and its 220N and 600N by 80 cents/gal, effective May 1.

Spot business remained minimal as a majority of U.S. base oil producers have been unable to offer spot volumes because they focused on meeting contract commitments. While some suppliers had been able to provide spot cargoes from existing inventories, these were being depleted. Domestic producers noted that although U.S. production had not been “hit as hard” as other producers’ globally due to the Middle East oil supply disruptions, base oils were still very tight in the U.S.

While some producers were able to supply contract customers at normal levels, a few have implemented strict allocation programs or were considering cuts for the coming months. Blenders who were not able to receive enough base oil volumes from their suppliers have contacted other producers to obtain additional product. “We are getting a lot of spot inquiries, both domestic as well as from around the globe,” a producer acknowledged.

However, most suppliers had little extra inventory to offer, with another supplier noting: “We are not quoting on exports, spot orders or taking on new customers. Some exceptions for occasional truck, flexi or ISOTANK, subject to availability.” This seemed to be the situation for many suppliers at a time when lubricant demand picks up in the U.S. ahead of the summer driving season, and participants also start to pad inventories for the hurricane season, which starts in June.

The tight conditions were affecting Group II cuts the most, but Group I supplies were also snug, particularly bright stock, which is a difficult grade to replace. Demand for lubricants that serve the industrial and heavy-duty segments has been steady, although market uncertainties were leading to limited stockpiling.

Given the steep increases in competing fuel prices — diesel prices have increased 45% since the start of the war and the national average price stood at $5.46 on Tuesday, according to The New York Times — some refiners were favoring fuel production and have cut back base oil output. A couple of producers were heard to have had to export base stocks to support internal operations in Asia and Europe, as crude shortages in those regions have led to curtailed refinery runs.

In Brazil, there has been some panic purchasing as supplies have been tight for some time and they were expected to become even more strained as stocks were being run down. An outage at Brazilian producer Petrobras’ plant that started several weeks ago was still affecting supplies and has exacerbated the snug Group I supply conditions. The producer was heard to have suffered a production issue back in February which affected Group I heavy-viscosity base oils and bright stock availability. Base oil prices have surged because of the challenges importers face in finding supplies from the U.S., and Asian exports were largely unavailable. Supplies of Group III grades have dwindled even more as shipments from the Middle East and Asia have been curtailed. Domestic suppliers were striving to meet contract commitments but had to restrict volumes to customers. The domestic producer has also announced hefty increases of approximately 30 percent for domestic sales in April.

In Mexico, prices continued to be exposed to upward pressure due to climbing crude oil prices, declining supplies and limited export availability from the U.S. and Asia. Contract shipments continued to flow from the U.S. to Mexico, but suppliers were being more restrictive in terms of volumes and have placed some customers on allocation. Steeper transportation and packaging costs were becoming an additional burden, particularly as blenders were facing buyer resistance to lubricant and finished products price increases.

Group III

With significantly reduced base oil volumes being able to reach the U.S. from the Persian Gulf and Asian refineries also cutting back production levels, the Group III segment was suffering the most direct consequences of the supply disruptions brought about by the war and closing of the Strait of Hormuz.

Iranian missile and drone attacks have damaged several refineries and base oil plants in the Middle East. One train at the Shell/Qatar Pearl GTL plant in Ras Laffan, Qatar, will be out of commission for at least one year following drone attacks, while the gas refinery that supplies its feedstocks has also been shut down. Drone attacks and supply disruptions at the Adnoc plant in Abu Dhabi and Bapco facilities in Bahrain have also resulted in large volumes being taken out of the market.

Some Asian producers are facing crude oil supply shortages as most refineries run on Middle East crude, and oil supplies from that origin have plummeted. While some governments in Asia have released strategic emergency oil supplies to ensure refineries continue to run and secure fuel supplies for the general population, some refineries were heard to be running at reduced rates and prioritizing fuels output versus that of other refined products such as base oils. Refiners were also seeking alternative sources of crude oil outside of the Middle East, although refining yields may not be the same as most facilities were built to run on Arab crude oil and shipments were expected to take some time to arrive.

Close to one third of global Group III base oil capacity is concentrated in the Middle East, and shipments from most producers have been suspended, although some cargoes were heard to be moving out from ports in the Red Sea. However, shipments were constrained due to a lack of vessels able to transit the area. The consensus seems to be that Group III barrels are going to dry up by June for those who are dependent on Middle East Group III supply, according to sources.

Asian Group III suppliers have up until now been able to meet a majority of U.S. contract commitments. Some were in a better position to continue doing so because their refineries have diversified where they receive their crude from, but others were expected to be close to depleting their stocks, and this will likely lead to product shortages until refineries increase production rates, and fresh shipments are delivered.

Domestic Group III producers were trying to continue running plants at top rates to meet contract obligations, with a couple having to place customers on allocation, but North American production is not sufficient to meet even a portion of all U.S. demand. Group III prices have therefore increased significantly over the last few weeks.

Naphthenic Base Oils

On the naphthenics side of the business, San Joaquin Refining informed customers that the company would be increasing all naphthenic and aromatic specialty oils by 50 cents/gal on May 4. The refiner had previouslymarked up its products by 70 cents/gal on April 6, citing volatile market conditions and regional supply/demand imbalances as driving the increases.

Other naphthenic base oil producers have implemented price increases to offset soaring crude oil and feedstock prices as well. A tightening supply and demand balance also provided additional support to the higher pale oil values. Ergon, Process Oils/Cross Oil and Calumet have all announced increases since the beginning of the Iran war on February 28.

Recent plant turnarounds, steady domestic demand and brisk export business have exacerbated the extremely tight market conditions. The light grades were in high demand from the transformer oil segment, while consumption of the heavy grades has been steadily creeping up as the rubber and tire segments prepare inventories for the U.S. summer driving season, which traditionally starts on Memorial Day weekend in late May. Some participants worried that miles driven this year may be dampened by increases in the price of gasoline and diesel.

Calumet started a two-week turnaround at its naphthenic base oil plant in Princeton, Louisiana, in mid-April. The producer said that the turnaround had gone to plan, and the unit was running well, allowing the supplier to work on building back inventory levels.

San Joaquin Refining completed a scheduled turnaround at its refinery in Bakersfield, California, in March. The turnaround and a delayed restart depleted the producer’s inventory, but the supplier was currently working on rebuilding stocks, while Cross Oil completed turnaround at its plant in Smackover, Arkansas, in March.

Lubricant Increases

A number of lubricant and grease manufacturers have communicated a fresh round of price increases, following previous adjustments given the mounting costs of base oils, additives, packaging and transportation. The implementation dates have been set between March 11 and May 20, with some suppliers nominating one increase and some two increases since the start of the war in Iran. Participants underscored that given current uncertainties and the fast pace of market changes—not to mention the escalating production costs–it has been very challenging to plan inventories and make pricing decisions.

Among the manufacturers that have announced increases were Calumet, CAM2, Castrol, Shell/SOPUS, PennStar, Chevron, ExxonMobil, Citgo, Phillips 66, Martin Lubricants, AOCUSA/Amalie, Highline Warren, Reliance Fluid Technologies, TotalEnergies USA, Consolidated Brands/ZXP Technologies, Omni Specialty Packaging, and Valvoline. Most suppliers announced lubricant and grease increases of up to 9% to 35%, depending on the product, with some lubricant increases ranging 48 cents per gallon to $5/gal, and $0.07-0.11/lb for greases. The higher end of the range applied to fully synthetic lubricants, and it was also inclusive of previous increases.

Middle East Base Oil Capacity Shutdowns

According to reports, Shell/Qatar Petroleum has halted production at one train of its Pearl GTL Group II/Group III facility in Qatar after sustaining damage during Iranian aerial attacks on March 19. The plant, which can produce 300,000 metric tons of Group II base oils and 1,072,000 metric tons of Group III base oils per year, experienced a fire at one of its processing trains and production has been shut down at that train, with sources expecting the plant to remain offline for an extended period, possibly one year or longer as the specially designed equipment at the plant may be difficult to repair and may need to be replaced, according to sources. Earlier Iranian attacks on Qatar Energy’s LNG refinery in Ras Laffan, which supplies feedstocks to the Pearl unit, caused damages that will put the facilities out of commission for several years, with the company expected to declare force majeure on LNG contracts for up to five years, Reuters reported.

Abu Dhabi state oil giant Adnoc has shut part of its Ruwais refinery complex in response to a fire that broke out on March 10, following a drone strike. Sources indicated that while the Ruwais West refinery was shut down for inspection and safety reasons, other operations within the massive complex might be continuing at reduced capacity. According to sources, the Ruwais East unit was running and was expected to continue production, including that of base oils, but this could not be confirmed with the producer directly. The Ruwais complex houses a 600,000 metric-tons-per-year Group II and Group III plant. Adnoc has been able to ship product out through ports on the Red Sea, according to sources.

In Bahrain, fire erupted at Bapco’s refinery in Maameer on March 5 following an Iranian attack, forcing the refinery to declare force majeure on production. Bapco operates a 400,000 tons-per-year Group III base oil facility in Sitra, within the Bapco refinery complex. Bapco originally indicated that base oil production had been unaffected, but it was later heard that the producer had trimmed supply levels.

In Saudi Arabia, a drone struck the Samref oil refinery in Yanbu, while Saudi forces intercepted a ballistic missile targeting the Port of Yanbu — one of the few ports where tankers are still able to lift cargoes as it is located on the Red Sea.

Crude Oil

Crude oil futures climbed on Wednesday on news that the UAE would be exiting the OPEC, while there has been little progress towards a resolution to the U.S.-Israel-Iran conflict. President Donald Trump appeared ready to increase the pressure on Iran’s economy and oil exports by continuing the U.S. blockade of Iranian ports.

- West Texas Intermediate June 2026 futures settled on the Nymex at $99.93 per barrel on April 28, up from $89.67/bbl for front-month futures on April 21.

- Brent June 2026 futures were trading on the ICE at $114.47/bbl on April 29, up from $99.27/bbl for front-month futures on April 22.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $101.29/bbl on April 27. Spot prices had settled at $92.76/bbl on April 20, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, April 27 (April 20), EIA

New York Harbor: $4.01 per gallon ($3.60/gal)

Gulf Coast: $3.94/gal ($3.46/gal)

Los Angeles: $4.34/gal ($3.65/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices April 29, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner