Crude oil prices hovered at nosebleed levels as the United States and Israel war against Iran continued and the vital Strait of Hormuz remained closed, effectively cutting off oil shipments from most oil-producing nations in the Persian Gulf. The situation in the Middle East and tightening base oil supplies has driven base oil producers to implement price increases throughout the month of March, with some nominating several rounds in the span of a month. According to reports, ExxonMobil and Paulsboro announced a fourth increase, and on the naphthenics side, Ergon and Process Oils also communicated price adjustments over the week.

While the risk of the conflict dragging on persisted, with more than 4,000 Marines in the Middle East and 2,000 paratroopers on their way,there were signs that the U.S. and Iran might be closer to reaching a deal. Iranian state media reported that Iran’s president Masoud Pezeshkian had said his country was ready to stop fighting, provided assurance that it would not be attacked again. U.S. president Donald Trump, on his part, declared that Iran’s military had been decimated and that the country did not have the ability to build a nuclear weapon any longer – a claim he had also made when the U.S. bombed Iranian nuclear facilities in June 2025.

Meanwhile, crude oil futures continued to hover at levels above $100 per barrel, despite optimism that the war would soon come to an end following the Iranian and U.S. presidents’ comments, because the Strait of Hormuz remained closed and Middle East oil supplies were limited.

The average national diesel price rose to $5.454 per gallon by the end of March, reflecting a hefty 45% month-over-month spike, while gasoline prices have increased significantly as well, OilPrice.com reported. The Trump administration may resort to restricting gasoline exports to relieve the price pressure at home.

Base Oil Price Increases

The soaring crude oil prices and reduced global availability of base oils, given the closure of the Strait and plant shutdowns in the Middle East following Iranian drone attacks, have driven base oil producers to seek several base oil price increases since the start of the conflict on Feb. 28.

According to sources, ExxonMobil communicated its fourth posted price increase since early March, with the hike going into effect on April 3. The company explained that the price increase was “due to continued rapidly changing global and regional supply/demand balances.” ExxonMobil’s API Group I grades will increase by 48 cents/gal; its Group II EHC65 cut by 60 cents/gal and its Group II+ EHC45 grade by 71 cents/gal.

Paulsboro will be increasing prices by 48 cents/gal on all of its Group I base oils on April 8. This is also the producer’s fourth increase since early March.

On the naphthenic base oils side, producers have also communicated price increases for contractual transactions, with a few suppliers announcing a second or third round of increases this month.

Ergon announced an increase of 35 cents/gal in pricing of naphthenic oils in the North American market, effective March 27. The company added that it was “closely monitoring developments within the Middle East and will provide pricing updates as needed in a timely manner.” Ergon had previously

raised naphthenic base oil prices by 45 cents/gal on March 13.

Process Oils communicated a price increase of 35 cents/gal for its naphthenic base oils in the North American market, effective March 27. Process Oils had previously implemented an increase of 45 cents/gal for its line of Cross Oil naphthenic base oils which went into effect on March 13.

Calumet had alsoannounced a 25 cents/gal price increase on all of its naphthenic oils, effective March 25, the previous week. The producer had earlier implemented price hikes on March 10 and March 17.

The supply and demand balance within the naphthenic base oils segment has tilted towards the tight side, particularly for the light grades, because of recent, ongoing and upcoming plant turnarounds and healthy demand from the transformer oil sector. Consumption of the heavy grades was not as robust, but may see an uptick ahead of the summer driving season from the rubber and tire segments.

San Joaquin Refining completed a scheduled turnaround at its refinery in Bakersfield, California, in March. The turnaround and a delayed restart depleted the producer’s inventory and it was expected to be on allocation while it rebuilds stocks.

Cross Oil started a turnaround at its plant in Smackover, Arkansas, on February 20. The program was expected to last approximately 23 to 25 days, and after a restart attempt, the plant was heard to have been shut down again. Even though the supplier was expected to have built inventories to fulfill orders during the shutdown, a longer outage might limit supplies from the producer moving forward.

Calumet was expected to have built inventories ahead of a turnaround at its naphthenic plant in Princeton, Louisiana, in the first half of April, and have restricted spot sales for that purpose.

Lubricant Increases

Lubricant manufacturers have also communicated price increases given the mounting cost of base oils, additives and transportation, with implementation dates peppered between mid-March and mid-April. A number of suppliers have announced a second round of increases as the first adjustments were deemed insufficient to offset the sharp rise in production costs. Among the manufacturers that have announced increases so far were Calumet, CAM2, Shell/SOPUS, PennStar, Chevron, ExxonMobil, Citgo, Phillips 66, Martin Lubricants, Amalie, Highline Warren, Reliance Fluid Technologies and Omni Specialty Packaging. Most suppliers announced increases of up to 9% to 25%, depending on the product, and some marked up prices by 48-85 cents/gal.

Group I and Group II

A tightening supply and demand scenario affected both the Group I and Group II segments, but the Group II seemed to have been particularly hit by dwindling supplies. A majority of U.S. base oil producers have withdrawn spot offers and abstained from seeking export business, as they focused on fulfilling contract commitments and protected inventory levels.

Refinery economics have shifted towards the increased production of gasoline, diesel and jet fuel because of potential shortages and soaring prices, forcing some refiners to stream more feedstocks into competing fuels output versus that of other products such as base oils.

The reduced output would coincide with the traditional spring lubricant production cycle, when base oil demand from the automotive, agricultural and construction segments tends to flourish. Suppliers were focusing on meeting term obligations and have restricted sales volumes or have placed customers on allocation. A majority of buyers took in as much product as possible to ensure availability and have accepted the steeper prices, while those who decided to wait for an end to the conflict in the Middle East may have difficulties in sourcing product. Even if the war were to end in the next few days, the situation was not expected to improve overnight, with the consequences of the global crude supply shortages and suspended shipments likely to last for some time. The supply shortages were especially noticeable in the Group III segment.

In some cases, buyers have turned to rerefined base oils to make up for product deficits, and this has helped support rerefined base oil prices.

In Brazil, the local producer, Petrobras, was heard to have suffered production setbacks affecting Group I heavy-viscosity base oils and bright stock since mid-February and supplies have therefore tightened. With imports from the U.S. expected to be reduced to a trickle, consumers worried about product shortages. Prices have climbed in line with those in other regions, with both Group I and II values showing a steady ascent, while Group III have seen the most significant increases due to reduced supplies from the Middle East and a suspension of spot offers from Asian suppliers. The domestic producer has also announced hefty increases for domestic sales in April.

In Mexico, base oil prices have also climbed because of reduced availability from the U.S. as suppliers have withdrawn spot offers. Contract cargoes generally continued to move from the U.S. to Mexico, but suppliers were very restrictive in terms of volumes. Spot offers for Asian base oils into Latin America have also been suspended because of production cutbacks and climbing freight rates. There continued to be reports of U.S. rerefined base oils moving to Mexico at slightly more competitive prices than virgin base oils.

Group III

Base oil production disruptions in the Middle East following Iranian drone attacks on base oil plants and the refineries that supply their feedstocks have led to global supply shortages. Close to half of all U.S. Group III imports originate in Qatar, Bahrain, and the United Arab Emirates, and these countries have ports on the Persian Gulf, which is effectively closed off to vessel traffic. With the Shell/Qatar Pearl GTL plant out of commission following drone attacks on both its facilities and the gas refinery that supplies its feedstocks, almost 20% of all Group III supplies have been taken out of the market, leading the balance of producers to place customers on allocation.

Asian supplies have also been reduced because Group III producers utilize Middle East crude imports to run their refineries, and crude exports from that region have plummeted. Several Asian governments have requested refiners to produce fuels instead of other refined products like base oils that were not considered as essential, while exports of refined products have also been suspended. South Korean imports moving to the U.S. were anticipated to continue, but customers were expected to see restrictions and allocations. Prices have climbed, not only because of supply disruptions, but also because of steeper feedstock costs, freight rates and insurance premiums.

Domestic Group III producers were trying to meet contract obligations, with a couple placing customers on allocation, but spot offers have been withdrawn by a majority of suppliers. While there had been speculation that domestic producers would try to increase Group III production rates, sources said that they would maintain the current Group II and Group III output levels so as to protect their refining equipment.

Middle East Base Oil Capacity Shutdowns

Iran and its allied militias continued to launch drones and missiles across the Middle East in retaliation to the U.S. and Israeli attacks, targeting energy infrastructure in Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Bahrain, and Iraq, and putting several facilities out of commission. These strikes exacerbated the dire oil supply situation, as not only were crude tankers unable to transit the Strait of Hormuz, but crude oil and refined products output have also been shut down.

Several Middle East base oil producers have been forced to halt production and declare force majeure.

According to reports, Shell/Qatar Petroleum has halted production at its Pearl GTL Group II/Group III facility in Qatar after sustaining damage during aerial attacks on March 19. The unit, which can produce 300,000 metric tons of Group II base oils and 1,072,000 metric tons of Group III base oils per year, experienced a fire at one of its processing trains and production has been shut down, with sources expecting the plant to remain offline for an extended period, possibly one to two years. Earlier Iranian attacks on Qatar Energy’s LNG refinery in Ras Laffan, which supplies feedstocks to the Pearl unit, caused damages that will put the facilities out of commission for several years, with the company expected to declare force majeure on LNG contracts for up to five years, Reuters reported.

Abu Dhabi state oil giant ADNOC has shut part of its Ruwais refinery complex in response to a fire that broke out on March 10, following a drone strike. Sources indicated that while the Ruwais West refinery was shut down for inspection and safety reasons, other operations within the massive complex might be continuing at reduced capacity. According to sources, the Ruwais East unit was running and was expected to continue production, including that of base oils, but this could not be confirmed with the producer directly. The Ruwais complex houses a 600,000 metric-tons-per-year Group II and Group III plant.

In Bahrain, fire erupted at Bapco’s refinery in Maameer on March 5 following an Iranian attack, forcing the refinery to declare force majeure on production. Bapco operates a 400,000 tons-per-year Group III base oil facility in Sitra, within the Bapco refinery complex. Bapco originally indicated that base oil production had been unaffected, but it was not clear whether the unit was currently producing base oils.

Iran also attacked Iraqi oil facilities, further crippling refining operations in the country. In Saudi Arabia, a drone struck the Samref oil refinery in Yanbu, while Saudi forces intercepted a ballistic missile targeting the Port of Yanbu–one of the few ports where tankers are still able to lift cargoes as it is located on the Red Sea.

Crude Oil

Crude oil futures climbed on Tuesday as markets were on edge given ongoing attacks in the Middle East and restricted transit in the Strait of Hormuz. Iranian drones targeted fuel tanks at Kuwait International Airport, causing a fire and damage to the tanks. However, prices moved lower following unconfirmed reports that Iran’s president was looking to end the war.

- West Texas Intermediate April 2026 futures settled on the Nymex at $101.38 per barrel on March 31, up from $92.35/bbl for front-month futures on March 24.

- Brent May 2026 futures were trading on the ICE at $105.50/bbl on April 1, up from $101.10/bbl for front-month futures on March 25.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $110.69/bbl on March 30. Spot prices had settled at $96.43/bbl on March 24, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, March 30 (March 24), EIA

New York Harbor: $4.49 per gallon ($4.17/gal)

Gulf Coast: $4.53/gal ($4.12/gal)

Los Angeles: $5.20/gal ($4.51/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

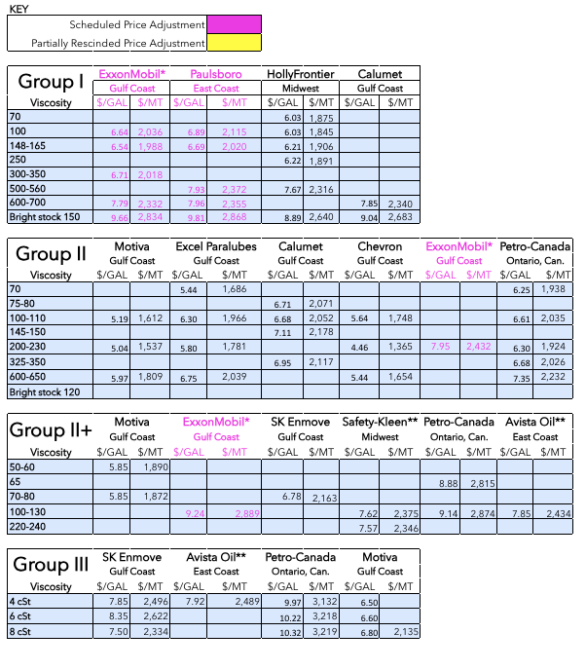

Posted Paraffinic Base Oil Prices April 1, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner