Crude oil and diesel prices surged to multi-month highs following news that the United States and Israel had launched a coordinated attack on Feb. 28 against Iranian targets, killing key officials and damaging military facilities. Iran responded with retaliatory strikes on U.S. military bases, ports, airports and oil refining facilities in neighboring Persian Gulf countries. The government in Tehran also closed the Strait of Hormuz on Saturday, stranding several oil tankers in the Gulf and choking vessel movements.

The strait is key to oil and gas exports as it connects the biggest Gulf oil producers, such as Saudi Arabia, the United Arab Emirates, Iran and Iraq, with the Gulf of Oman and the Arabian Sea. News outlets reported that Saudi Aramco had started to reroute some of its crude oil shipments to the Red Sea port of Yanbu, but other operators have suspended shipments. The situation did not only affect crude oil, but diesel/gasoil and jet fuel movements as well.

Oil prices were expected to remain high while the conflict continued, but analysts were concerned that a quick de-escalation would erase the fresh gains, which is what happened in June 2025 when the U.S. struck Iranian nuclear facilities. Conversely, a prolonged war would likely help support prices and offset a planned OPEC+ output increase.

Similarly, U.S. base oil suppliers were evaluating global market conditions to determine whether any price adjustments were warranted. They cited growing concerns that the conflict in the Middle East would result in base oil production and shipment disruptions as facilities and vessels in the Persian Gulf came under attack and ship operators suspended activity in most of the region. The climbing price of diesel may influence refinery decisions, with operators potentially favoring distillates production in detriment of base oil output if diesel prices continue to rise. Freight and insurance rates surged due to the heightened war risk premiums, and some key insurers suspended cover altogether.

A number of base oil producers responded almost immediately to the potential supply disruptions and surging crude oil prices by increasing postings, although steeper oil prices do not typically translate into higher base oil prices overnight. Prices for API Group III base oils were the most likely to be impacted by the situation in the Middle East as close to half of all U.S. Group III imports originate in that region, but South Korean producers were also affected as refiners process Middle Eastern crude oil.

In the U.S. market, SK Enmove increased its Group II+ and III U.S. base oil postings by 10 cents per gallon on March 1. A second Group III supplier was heard to have raised its 4 cSt spot prices by 30 cents/gal this week as well.

The SK posted price increase followed a couple of initiatives that emerged in February but that were unrelated to the situation in the Middle East. Two producers adjusted postings at that time, ExxonMobil and Motiva, with one nominating an increase and the other a decrease. The ExxonMobil Group II+ EHC45 increase was thought to have been prompted by tightening supply of the Group III 4 cSt grade, which ExxonMobil’s product can replace in certain applications. Motiva’s decreases were likely driven by a need to bring posted prices more in line with actual market transactions.

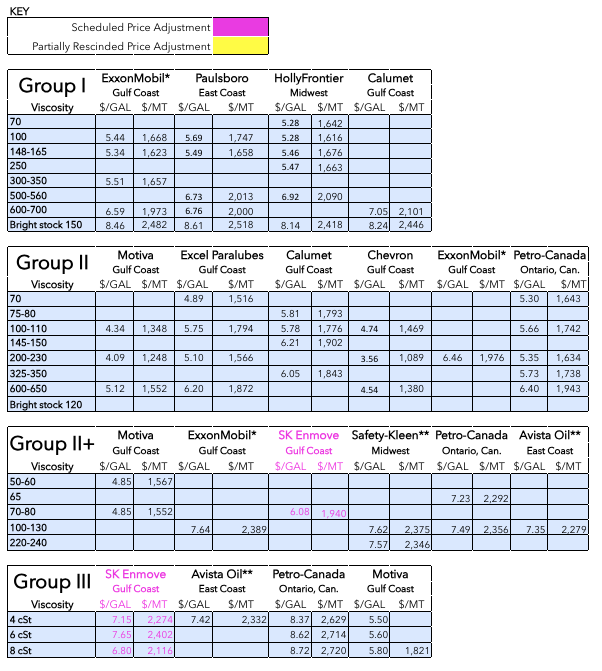

Group I

The base oil market continued to be described as slightly long, with suppliers focusing on attaining a balanced supply and demand inventory position. In general terms, the Group I and II light grades were less readily available than the heavier grades. However, bright stock seemed to be an exception in that supplies were more limited and demand remained healthy, supporting stable-to-firm prices. Spot prices of all grades were heard to have been adjusted up by about 5 cents/gal, driven by steeper crude prices and prospects of a tightening supply and demand scenario.

With the spring lubricant and agricultural planting season approaching, base oil suppliers have started to prepare for an uptick in domestic demand. But buyers were likely to be more conservative in terms of orders and secure only those volumes needed to run day-to-day operations instead of building high inventories, although some have started to worry about the upward price pressure emerging this week.

U.S. producers were still on the lookout for export opportunities, but the dramatic changes in global market fundamentals this week prompted some to hold off on offers until a clearer market picture emerged and oil prices stabilized. At the same time, base oil and lubricant consumers worried that a prolonged conflict might not only pressure up crude oil and base oil prices, but also result in steep gasoline prices, heftier inflation and an economic downturn that would likely dampen lubricant demand.

Regular contract shipments were expected to continue moving to Mexico, where prices were also exposed to upward pressure. Some spot cargoes have also been earmarked for Brazil, where demand is ongoing despite the restart and increased production rates at the domestic Petrobras plant, following an unplanned extended shutdown that started last October. Spot availability of bright stock was still on the snug side, but supplies of other Group I and II grades appeared to be more ample.

Group II

As was the case for Group I grades, the Group II heavy grades were more plentiful than their light-viscosity counterparts, although at least one supplier was heard to be in a balanced-to-snug position on all grades.

Last week, Motiva announced a posted price decrease of 50 cents per gallon for its Group II, II+ and III grades that went into effect on March 1. According to sources, the company revised its prices to get postings aligned with actual market values, with participants also pointing out that not all accounts will be impacted by the price revisions, since the producer uses many different price formulas for contracts.

At the same time, there were reports that ExxonMobil had increased the price of its Group II+ EHC 45 grade by 25 cents/gal on Feb. 20. Sources commented that this price increase was not so much a reflection of market conditions for standard grade Group II/II+ products, but rather an indication of high demand for Group III 4 cSt base stock. ExxonMobil has obtained Dexos approval for its EHC 45 product in PCMO applications and it can replace an approved Group III 4 cSt cut.

Rerefined base oils have gained widespread acceptance in the U.S. and Mexico and were heard to be competing with virgin base oils in some segments. Spot supplies of rerefined material may see a slight tightening as a rerefiner has scheduled a turnaround in the first quarter and was expected to limit spot supplies to build inventories. A second rerefiner plans to embark on a brief four-day shutdown in late Q1, but this was not expected to affect the supplier’s deliveries.

Group III

The Group III segment might see the most direct impact of the geopolitical developments in the Middle East as close to half of all U.S. Group III imports originate in Bahrain, the United Arab Emirates, Saudi Arabia and Qatar.

“The biggest impact from the Iran crisis is that there is very little spot availability of Group III base oils,” a market source commented.

A couple of Middle East facilities were also heard to been hit by Iranian drone attacks, but it was not clear whether base oil production had been affected. In Qatar, Qatar Energy halted production of liquefied natural gas and other products following drone attacks on its facilities in Ras Laffan and Mesaieed. While it could not be ascertained whether the Qatar/Shell Pearl gas-to-liquids base oil unit had suffered any damages, base oil production may be curtailed as the unit utilizes natural gas from the refinery to produce Group III base oils.

Steeper freight rates and insurance premiums were also expected to exert upward pressure on prices in the long term. A supplier of Middle East material said that the closing of the Strait of Hormuz would not result in supply disruptions because the company had already altered its shipping route since the Houthi attacks in the Red Sea started back in 2023/2024, with vessels sailing the longer route around the Cape of Good Hope in South Africa instead. But this had resulted in longer voyages and higher freight rates. Given all of these disruptive factors, it was not surprising to see price increases emerge within the Group III segment.

As mentioned, SK Enmove announced a posted price increase of 10 cents/gal on all of its Group II+ and III grades, effective March 1.

A second supplier was heard to have increased the spot price of its Group III 4 cSt cut by 30 cents/gal, while it is offering competitive prices for its 6 cSt and 8 cSt grades, which appeared to be more plentiful.

Naphthenics

Prices for naphthenic oils were reported as stable, but they were exposed to upward pressure due to the sudden jump in crude oil and diesel prices. Buyers whose contracts are indexed against diesel prices may see increases over the next few days. The pale oil supply and demand ratio has also tightened over the last few weeks due to two ongoing plant turnarounds, and this provided additional price support.

San Joaquin Refining was expected to complete a scheduled turnaround at its refinery in Bakersfield, California, at the end of February, but a restart was delayed for a couple of weeks. The producer is now expecting production to restart on March 4. The delay has depleted the producer’s inventory and it was expected to be on allocation through March.

Cross Oil has scheduled a turnaround at its plant in Smackover, Arkansas, that began on Feb. 20. The program will last approximately 23 to 25 days, and the supplier was expected to have built inventories to fulfill orders during the shutdown.

Calumet will also likely start to build inventories over the next few weeks as the producer plans to have a turnaround at its naphthenic plant in Princeton, Louisiana, in the first half of April.

Crude Oil

Crude oil futures rose about 1% on Wednesday, following hefty increases of 8% on Monday and 3% on Tuesday as U.S.-Israeli strikes on Iran disrupted Middle East supplies. The pace of gains slowed from past sessions after U.S. President Donald Trump suggested the U.S. Navy could escort vessels through the Strait of Hormuz, Reuters reported.

- West Texas Intermediate April 2026 futures settled on the Nymex at $74.56 per barrel on March 3, up from $65.63/bbl for front-month futures on Feb. 24.

- Brent futures for May 2026 delivery were trading on the ICE at $82.31/bbl on March 4, up from $70.71/bbl for front-month futures on Feb. 25.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $75.38/bbl on March 2. Spot prices had settled at $69.09/bbl on Feb. 24, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, March 2 (Feb. 24), EIA

New York Harbor: $3.00 per gallon ($2.78/gal)

Gulf Coast: $2.82/gal ($2.61/gal)

Los Angeles: $2.88/gal ($2.67/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices March 4, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner