With the market still showing signs of being oversupplied and fewer export opportunities because of lackluster demand in other regions, domestic buyers have been able to find as much product as needed and no shortages were reported. Several producers have reached a fairly balanced supply and demand position and did not feel pressured to lower inventories. Others were hoping to conclude export business, but buying appetite from traditional outlets such as India has weakened. The approach of the spring season also meant that additional opportunities may surface within the domestic realm, although lubricant manufacturers still remained cautious in terms of inventory levels. The Presidents’ Day holiday on Feb. 16 dampened activity early in the week.

Crude oil prices did not offer clear direction, because they edged up one day and slipped the next, swayed by geopolitical tensions and demand forecasts. Futures edged down on Monday on reports by that the United States and Iran intended to hold a second round of negotiations regarding Iran’s nuclear program. An International Energy Agency forecast that predicted reduced oil demand growth in 2026, and expectations that the OPEC+ would increase output in April also weighed on prices. However, by Wednesday morning, futures had started to trade higher despite encouraging talks between the U.S. and Iran in Switzerland, on news that Iran had fired missiles towards the Strait of Hormuz as part of a maritime military exercise. Observers feared that any attack could spiral into another regional conflict in the Middle East, which is still reeling from the Israel-Hamas war.

Additionally, market players kept an eye on the European Union’s proposed ban on European maritime services for Russian oil exports which could further disrupt the country’s refined products trade. Russia is one of the world’s top diesel exporters and the sanctions on Russian exports are significantly impacting diesel supplies by tightening global markets and boosting prices.

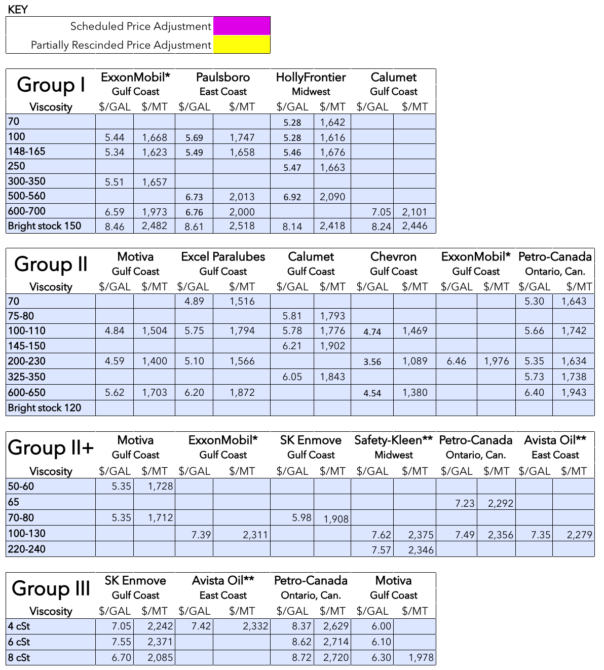

Group I

Supply of the API Group I grades was described as balanced to slightly long, depending on the grade. The heavy grades, with the exception of bright stock, were still more readily available than the light grades and were therefore more exposed to downward pressure. Competitive prices of heavy-viscosity Group II grades also meant that some consumers would secure Group II cuts to replace Group I base stocks in those applications that offered some flexibility. Spot values of the Group I SN500 grade were reported to have inched down by 3 to 4 cents per gallon given ample supplies.

Bright stock commanded more attention than the other grades as demand was healthy and availability remained on the snug side, partly because several bright stock cargoes had been shipped to Brazil in the previous months on increased buying appetite there, while a potential U.S. plant turnaround in the first quarter could also tighten supplies further.

Global oversupply of Group I and Group II base oils have reduced export opportunities for U.S. suppliers, but a number of them still saw ongoing business into Mexico and some inquiries from West Africa. However, macroeconomic factors and trade uncertainties affecting the U.S.-Mexico relationship, together with competition with rerefiners and South Korean supplies posed some challenges to virgin oil producers. Import licenses for Mexican importers have now been renewed for the most part and were not impeding U.S. exports moving to the neighboring nation.

Carnival celebrations in Brazil on Monday and Tuesday this week and a slowdown on the days leading up to the holidays dampened activity, but U.S. suppliers had tried to conclude business ahead of the festive period. Brazil had imported significant amounts of Group I and Group II grades since last October, when key Brazilian producer Petrobras’ Group I plant suffered an unexpected shutdown that lasted several weeks. While contractual supplies have recovered because production rates have improved, spot supplies in Brazil remained on the tight side. Domestic prices for February edged down in Brazil for most Group I grades, while prices for Group II cuts were steady.

Group II

Despite the fact that spot Group II prices were reported as largely stable this week, downward pressure on the 220N and 600N persisted given plentiful availability and sluggish demand, particularly from industrial applications. Spot price indications for the Group II 600N were reported to have slipped by 5 cents per gallon week on week. However, suppliers were hoping that the approach of the spring lubricant production season would translate into improved buying appetite over the next few weeks, and that this would help stabilize prices.

The 100N cut remained on the tight side, supporting prices at the current levels. Export discussions for all Group II grades were more muted than earlier in the year, with steep freight rates and ample Group II supplies in Asia dampening export opportunities into India.

Virgin Group II base oil suppliers said that there had been some pockets of competition with rerefined oils, which many blenders have started to purchase given attractive prices and high quality.

Rerefined base oil volumes were deemed adequate to meet most requirements, even though a rerefiner has scheduled a turnaround in the first quarter and was expected to restrict spot supplies to build inventories. A second rerefiner plans to embark on a brief four-day shutdown in late Q1, but this will not affect the supplier’s shipping schedule.

Group II

As has been the case over the last two months, spot prices for the Group III 4 centiStoke cut were stable-to-firm given more limited supplies of this grade compared to the 6 cSt and 8 cSt cuts. The 4 cSt can be used in more applications and this partly led to the tighter conditions. Discussions involving spot supplies of the 6 cSt and 8 cSt cuts were heard at lower levels compared to last week, with values edging down by 1 to 2 cents per gallon.

Group III cargoes from Asia and the Middle East were anticipated to arrive as scheduled, with no disruptions reported. While most of these shipments were allotted to contractual business, several cargoes were offered on the spot market. There continued to be attractive offers for products with partial approvals.

While concerns of tightening supplies in Europe circulated following a fire at Repsol’s Cartagena, Spain, industrial complex on January 26, steady import supplies from Asia and the Middle East were deemed sufficient to meet current requirements in North America. The fire had broken out in Topping Unit 3, which was on older section of the refinery and separate from other production plants, limiting the risk of the fire spreading, media sources reported. The blaze was put out after a few hours and there were no injuries. The Cartagena complex includes a 135,000-ton Group I unit and a 630,000-ton Group II and III unit operated through a joint venture with South Korea’s SK Enmove.

Domestic production of Group III grades and rerefining operations were steady, with Group III output at these plants mostly used for internal lubricant production and not having a significant impact on current price indications.

Naphthenics

Prices for naphthenic oils were reported as stable, propped up by firm crude oil and feedstock prices the previous week. Steady demand levels for the light grades, along with three plant turnarounds and efforts by the producers to build inventories to ensure all contract commitments were met during the outages have resulted in a tightening supply and demand situation, offering further support to prices.

Robust demand for the light grades mostly came from the transformer oil side, while requirements for the heavy grades that serve the rubber, tire and grease segments have flatlined. Growing supplies in other regions, including Asia, have limited export opportunities for U.S. producers.

An ongoing turnaround and two upcoming ones have strained naphthenic base oil supplies on the domestic front. San Joaquin Refining was expected to have started a three-week scheduled turnaround at its refinery in Bakersfield, California, at the end of January. The producer planned to continue meeting customers’ requirements during the outage but was not likely to offer spot supplies.

Cross Oil plans to start a turnaround at its plant in Smackover, Arkansas, on Feb. 20. The program will last approximately 23 to 25 days, and the supplier was expected to have built inventories to fulfill orders during the shutdown.

Calumet will also likely start to build inventories over the next few weeks as the producer plans to have a turnaround at its naphthenic plant in Princeton, Louisiana, in the first half of April.

Crude

Crude oil futures fell slightly on Wednesday as talks between the U.S. and Iran showed some progress–raising hopes for a de-escalation of tensions and lowering risks of supply disruptions from one of the top Middle Eastern oil producers–but prices then moved up on reports of an Iranian missile strike in the Red Sea.

- West Texas Intermediate March 2026 futures settled on the Nymex at $62.33 per barrel on Feb. 17, down from $63.96/bbl for front-month futures on Feb. 10.

- Brent futures for April 2026 delivery were trading on the ICE at $67.59/bbl on Feb. 18, down from $69.77/bbl for front-month futures on Feb. 11.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $64.55/bbl on Feb. 13. Spot prices had settled at $65.73/bbl on Feb. 9, according to the U.S. Energy Information Administration. (There was no trading on Feb. 16 due to the Presidents’ Day holiday).

Diesel

Low-sulfur diesel wholesale, Feb. 16 (Feb. 9), EIA

New York Harbor: $2.47 per gallon ($2.37/gal)

Gulf Coast: $2.24/gal ($2.13/gal)

Los Angeles: $2.35/gal ($2.30/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices Feb. 18, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner