Despite recent run rate reductions at a number of plants due to freezing weather and a shift toward additional diesel and heating oil output, most base oil grades were readily available. The slight refining adjustments may have mostly affected the light base oil cuts, which were already in tighter supply than the heavy cuts. Export business has slowed down and this has narrowed suppliers’ opportunities to lower inventories further. Posted prices were steady as producers seemed fairly comfortable with current inventory levels, and there were expectations that improved demand would surface over the next few weeks as blenders start building stocks for the busy spring production cycle.

The winter storm that hit large areas of the United States and Canada at the end of January and the freezing temperatures that lingered for several days did not seem to have caused any major base oil production outages or supply disruptions, aside from some delivery delays due to brief port closures and barge, truck and railway transportation issues. Still, some buyers worried that supply may have tightened and there would be less product available at a time when demand typically takes off.

Aside from keeping an eye on base oil supply, participants were also monitoring crude oil prices closely as they have shown volatility since the start of the month. West Texas Intermediate futures surged during the winter storm because operators halted production at oil extraction sites and processing units, and then fell on expectations of nuclear talks between the U.S. and Iran. Last week, the two countries held diplomatic meetings in Oman and analysts grew optimistic about an easing of tensions. However, WTI crude edged higher this week on a weak dollar and ongoing Iran tensions, with traders turning more cautious on tenuous diplomatic progress and renewed threats by U.S. president Donald Trump. Additionally, fresh U.S. guidance for vessels in the Strait of Hormuz also pushed crude prices up as traders interpreted these guidelines as reflecting rising geopolitical risks.

Group I

Within the API Group I segment, bright stock was reported as the least available cut, although the light grades have tightened as well. This was attributed to export transactions in the previous weeks, together with slightly reduced operating rates at some plants and an upcoming turnaround at a Group I plant in the first quarter. The maintenance program was limiting the volumes being offered in the spot market as the producer focuses on meeting contractual commitments, according to sources.

Demand for the heavy cuts remained sluggish given seasonal patterns, which partly explained why these grades were more plentiful. Some buyers continued to seek Group II grades to replace Group I cuts whenever applications allowed because of competitive pricing.

Buying interest for export transactions into various destinations has waned, as the global base oil Group I and Group II segments appeared oversupplied. Regular U.S. shipments of virgin and rerefined base oils continued to move to Mexico, however, but business has slowed down due to macroeconomic factors and competition with Asian supplies, which exerted downward pressure on U.S. offers. Some Asian cargoes were also heard heading to the West Coast of South America, with a 4,000-metric ton parcel mentioned for possible shipment from South Korea this month. Additionally, a 5,000-ton cargo was quoted for shipment from Rotterdam, Netherlands, to Puerto Cabello, Venezuela, in the second half of February.

U.S. exports to Brazil continued to be reported, but volumes seemed to have abated because availability from the key domestic producer, Petrobras, has improved following an unplanned extended shutdown that started last October. The fact that availability has improved in Brazil was reflected in lower domestic prices for February. There was some buying interest for late February U.S. shipments, with at least one cargo heard under discussion. The lot involved up to 13,000 tons of base oils, likely to be lifted on the U.S. Gulf for Rio de Janeiro between Feb. 15 and March 2 by a key Brazilian distributor. Whether the cargo was made up of Group I, Group II or both could not be ascertained. Again, there were reports of competition with barrels from Asian origins being offered into the Brazilian market.

While domestic base oil and lubricant demand in Brazil had picked up in preparation for the summer vacation period, when many drivers take to the road, the approach of the Carnival holidays, when many businesses and factories close for at least a couple days, were expected to briefly dampen consumption. Carnival in Brazil runs from Feb. 13 through Feb. 18, with the peak celebrations and non-working days falling on Monday, Feb 16, and Tuesday, Feb 17. Logistics and customs services may experience significant delays or closures as well.

Group II

Spot Group II prices were steady, although there was still downward pressure on the 220N and 600N on ample availability and lackluster demand, particularly from the industrial segment. According to sources, existing stocks were deemed sufficient to meet immediate needs and buyers were holding off on acquiring additional volumes as lubricant demand prospects remained murky. At the same time, some blenders have started to inquire about additional base oil volumes as they prepare for the spring production season.

The 100N cut continued to be described as snug given thin availability from at least one producer, with spot prices reportedly edging up by a couple of cents per barrel week on week. But there have been no shortages noted and producers have been able to fulfill contractual obligations while keeping enough supplies for a likely pickup in demand ahead of the spring lubricant production cycle. Some buyers have also been able to secure rerefined base oils, which were available at competitive prices.

Rerefined base oils were plentiful, even though a rerefiner has scheduled a turnaround in the first quarter. A second rerefiner plans to embark on a brief four-day shutdown in late Q1, but this will not affect the supplier’s shipping schedule.

Export discussions were more muted than earlier in the year, but some negotiations were taking place for shipments to South Asia. Approximately 6,000 to 8,000 tons of base oils were quoted for shipment from the U.S. Gulf to Mumbai, India, between Feb. 7 and 25.

Group III

Spot prices for the Group III 4 centiStoke were reported as stable-to-firm due to a tightening supply and demand ratio, with some indications edging up by 2 cents/gal. A couple of suppliers were heard to have little 4 cSt availability to offer and this pushed prices up. Conversely, values for the 6 cSt and 8 cSt grades have slipped by about 2 cents/gal on plentiful supplies. There continued to be attractive offers for products with partial approvals.

Domestic production of Group III grades and rerefining operations were reported as largely unaffected by the winter storm a couple of weeks ago, although some plants were heard to have reduced operating rates in preparation for the severe weather. Group III output at these plants is still mostly used for internal lubricant production.

Naphthenics

Prices for naphthenic oils remained stable and received support from steeper crude oil prices over several days. A tightening supply and demand ratio, particularly of spot supplies, offered further support. The reduced supply was the result of improved demand levels, coupled with three upcoming turnarounds and efforts by the producers to build inventories to ensure all contract commitments were met during the outages.

Demand for the light grades was sustained by continuous consumption in the transformer segment, while there has been a slight improvement in requirements for the heavy grades that serve the rubber, tire and grease markets. Demand from the export front has been less robust than last year, especially since supplies in other regions, namely Asia, has grown.

On the domestic front, San Joaquin Refining was expected to have started a three-week scheduled turnaround at its refinery in Bakersfield, California, in late January. The producer plans to continue supplying its customers during the outage and market supplies were generally expected to tighten.

Cross Oil plans to start a turnaround at its plant in Smackover, Arkansas, on February 20. The program will last approximately 23 to 25 days. The producer reported no output disruptions due to the recent severe winter weather.

“We did a complete overhaul of our weatherization after the problems in 2021 and 2022. So we got through this with preparation and some luck as the worst of the ice missed us,” a company source explained.

Calumet will also likely start to build inventories over the next few weeks as the producer plans to have a turnaround at its naphthenic plant in Princeton, Louisiana, in the first half of April.

Crude Oil

Crude oil futures extended gains on Tuesday because analysts feared a confrontation between the U.S. and Iran amid a slowdown in negotiations and a U.S. military build-up in the Middle East. Iran is the fourth largest oil producer within the OPEC.

- West Texas Intermediate March 2026 futures settled on the Nymex at $63.96 per barrel on Feb. 10, up from $63.21/bbl for front-month futures on Feb. 3.

- Brent futures for April 2026 delivery were trading on the ICE at $69.77/bbl on Feb. 11, up from $67.69/bbl for front-month futures on Feb. 4.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $65.73/bbl on Feb. 9. Spot prices had settled at $62.95/bbl on Feb. 2, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, Feb. 9 (Feb. 2), EIA

New York Harbor: $2.37 per gallon ($2.29/gal)

Gulf Coast: $2.13/gal ($2.08/gal)

Los Angeles: $2.30/gal ($2.21/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

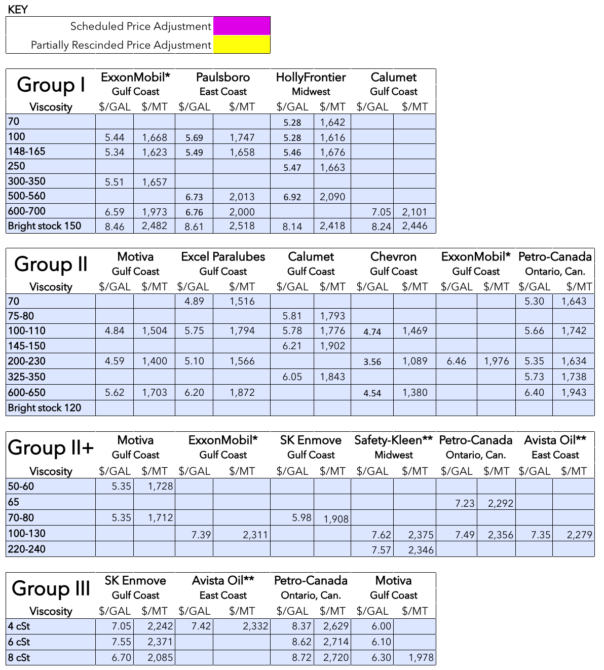

Posted Paraffinic Base Oil Prices February 11, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner