While the winter storm that affected large parts of the United States and Canada last week and the freezing temperatures that persist did not directly damage base oil facilities, contingency plans and the need to produce more diesel as demand for this fuel has jumped may impact base oil production rates moving forward. This might tilt supply towards the tight side and reduce the overhang that is currently impacting prices, particularly of the heavy grades, which were deemed plentiful.

The extremely cold temperatures caused refineries along the U.S. Gulf Coast to curtail production overall by roughly 50%, sources familiar with refinery operations said. Refineries on the Gulf Coast are not built for cold weather and simply do not run well at below freezing temperatures.

“Refiners learned their lesson in 2021 [during Winter Storm Uri], when they lost power and had a hard shutdown and the negative results that occurred from that,” a source explained. Hard shutdowns tend to damage equipment, and it is more difficult to restart a plant after them. Instead of waiting for a repeat of the same scenario, this time, refineries reduced production rates ahead of the storm.

Aside from base oil production outages, back in February 2021, refineries lost diesel output and they still had to meet diesel contract requirements, which caused a significant backlog. Similarly, this year, refineries will likely be making more diesel to catch up and fulfill commitments, particularly as diesel demand has spiked due to the need to run generators during widespread power outages. Sources said this situation may continue during most of the month of February. “Then add refinery maintenance turnarounds on top of this, and we might head into the busy season for base oil on lower supply,” the source added. A base oil supplier commented that buyers appeared worried about availability over the next few weeks, noting that “some of our buyers are more eager to secure more volume than usual; they may not need it now, but they want to make sure they will have it in 2-3 weeks.”

Most base oil producers reported little impact on base oil production from the storm as plants continued to run, even though some did so at reduced rates. Participants were keeping an eye on crude oil prices, which showed a sharp increase as the severe weather halted operations at oil production and processing units. However, futures fell early this week on news that the U.S. and Iran were likely to hold nuclear talks to de-escalate tensions, following U.S. president Donald Trump’s threat of a military attack on the country.

In oil-related news, the U.S. announced that it had reached a trade deal with India, after a year of tense relations between the two countries. The terms do not seem to be very advantageous for India;

the country was expected to curtail Russian oil imports (which are available at deeply discounted prices due to sanctions), as well as increase oil purchases from the U.S. and perhaps Venezuela. According to Trump, India has promised to buy $500 billion worth of energy, technology, agricultural goods, coal and “many other products.” That is a very big commitment, given India’s total goods imports reached $721 billion in the fiscal year ending March 2025, according to Nikkei Asia.

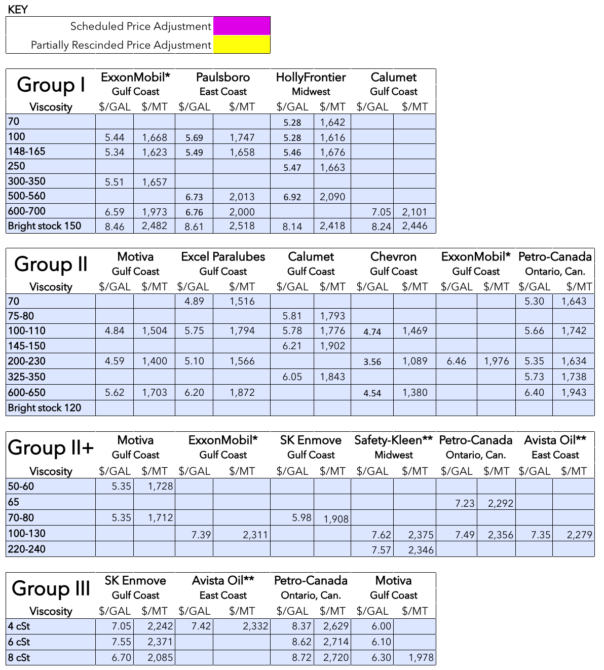

Group I

API Group I prices seemed to have stabilized, although the heavy cuts remained under downward pressure because of more plentiful availability and lower demand during the winter months, with domestic spot prices slipping by 2-4 cents per gallon week on week. The availability of competitively priced Group II heavy grades, which some blenders can use as a substitute, also pressured prices. Bright stock, on the other hand, was still sought-after and given fairly snug supplies, prices were firm. An upcoming Group I plant turnaround was also limiting the volumes being moved into the spot market as the producer wants to ensure contract commitments are met.

Discussions for export transactions have simmered down, partly because suppliers preferred to wait for a clearer supply situation in the next couple of weeks, following severe weather impacts and a sharp uptick in crude oil and feedstock prices. Some shipments were also heard to have suffered delays due to the closing of ports due to the freezing temperatures, while barge, railway and truck traffic was also affected.

Some attention continued to focus on exports to Brazil, although requirements appeared to have weakened because the key domestic producer, Petrobras, has been able to meet most of its contract commitments. Petrobras’ base oils plant had suffered an unexpected and extended shutdown since October and the supplier had been forced to suspend spot shipments and reduce contract volumes, which drove buyers to seek Group I and Group II imports. However, Petrobras’ ability to supply Group I contractual volumes appeared to have improved, although the producer was still unable to offer spot cargoes.

Regular U.S. shipments of virgin and rerefined base oils continued to move to Mexico, but demand in general was deemed lower than anticipated for this time of the year. Some participants blamed the reduced buying appetite for U.S. base oils on the availability of attractive offers for Asian material.

Group II

Domestic spot prices for the Group II mid- and heavy-viscosity grades 220N and 600N showed small downward adjustments of a couple of cents per gallon on plentiful availability and lackluster demand, namely from the industrial segment. The light grade 100N had reached the end of 2025 in a tight position and this continued to be the case, providing support to steady pricing.

Producers focused on meeting contractual obligations, making sure that inventories would be sufficient to meet any pickup in demand ahead of the busy spring lubricant production season.

As was the case with Group I base oils, suppliers were more hesitant about offering Group II cuts for export as the supply situation may be changing in the U.S. and crude oil prices had firmed the previous week. There was some buying interest noted from South America and Africa, but it could not be confirmed whether any deals had been concluded by the publishing deadline.

Group III

Spot prices for the Group III 4 cSt were reported as stable, while there continued to be downward pressure on the 6 cSt and 8 cSt grades on more substantial availability. There were fewer extra volumes of Asian products available in the U.S. market, with at least one supplier heard to be staying away from offering spot volumes.

Domestic production of Group III grades and rerefining operations were reported as largely unaffected by the winter storm, although some plants were heard to have reduced operating rates in preparation for the severe weather and in order to avoid a forced or hard shutdown, which makes a restart more difficult.

A rerefiner plans to undertake a brief four-day planned shutdown in late Q1, but this will not affect the supplier’s shipping schedule.

Naphthenics

Prices for naphthenic oils remained largely stable and received support from steeper crude oil prices last week, and an increasingly tighter supply and demand ratio, particularly as far as spot supplies were concerned. The tightening was the result of improved demand levels, coupled with upcoming turnarounds and efforts by the producers involved to build inventories and make sure that all contract commitments were met.

San Joaquin Refining was expected to have started a three-week scheduled turnaround at its refinery in Bakersfield, California, in late January. The producer plans to continue supplying its customers during the outage and market supplies were generally expected to tighten.

Calumet will also likely start to build inventories over the next few weeks as the producer plans to have a turnaround at its naphthenic plant in Princeton, Louisiana, in the first half of April.

A third producer was heard to have planned a maintenance shutdown in the first quarter as well, although further details could not be confirmed.

Crude Oil

Crude oil futures had weakened in previous sessions as U.S. refiners struggled to absorb increased Venezuelan crude exports. Reports of possible nuclear talks between the U.S. and Iran later this week also drove futures down, but prices edged up during early trading on Wednesday as the U.S. shot down an Iranian drone over the Arabian Sea.

U.S. crude oil inventories were impacted by the powerful winter storm last week, with the American Petroleum Institute (API) estimating a decrease of 11.1 million barrels in the week ending January 30. Crude oil inventories had decreased by 247,000 barrels the previous week.

- West Texas Intermediate March 2026 futures settled on the Nymex at $63.21 per barrel on Feb. 3, up from $62.39/bbl for front-month futures on Jan. 27.

- Brent futures for April 2026 delivery were trading on the ICE at $67.69/bbl on Feb. 4, slightly down from $67.96/bbl for front-month futures on Jan. 28.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $62.95/bbl on Feb. 2. Spot prices had settled at $61.69/bbl on Jan. 26, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, Feb. 2 (Jan. 26), EIA

New York Harbor: $2.29 per gallon ($2.32/gal)

Gulf Coast: $2.08/gal ($2.18/gal)

Los Angeles: $2.21/gal ($2.23/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices

February 4, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

* ExxonMobil prices obtained indirectly.

** Rerefiner