Base oil activity proceeded at a moderate pace this week, partly dampened by the Martin Luther King Jr. federal holiday on Jan. 19, with suppliers noting that inquiries had started to come in following the year-end holidays, but that demand remained sluggish. Buyers were assessing potential product needs and some have started to replenish stocks, but were cautious as they preferred to wait to see if prices would be revised.

Purchasing depended on how lubricant demand was shaping up, with some blenders seeing better offtake than others. Spot prices were generally steady, but remained under downward pressure due to ample domestic inventories and falling feedstock values. Sellers did not expect a significant pick-up in requirements until the end of the month or early February and kept an eye on crude oil and feedstock values, which drove refinery decisions.

Crude oil futures remained volatile and fell again early in the week as investors worried about the economic impact of the additional tariffs that United States President Donald Trump threatened to impose on several European nations.

Tariffs have come into focus again because the president plans to enforce fresh levies on imports from European countries that are standing by Denmark and objecting to his Greenland annexation plans. Greenland is a self-governing Danish territory whose citizens have expressed strong opposition to becoming part of the U.S. On Saturday, Trump threatened to impose tariffs of 10% on Denmark, Norway, Sweden, France, Germany, the U.K., the Netherlands and Finland, which would then rise to 25% on June 1, “until such time as a Deal is reached for the Complete and Total purchase of Greenland,” the president wrote.

The tariffs on thousands of imports that were first imposed when Trump took office last year have been under the Supreme Court’s scrutiny as well, and its justices were expected to rule on their constitutionality this week. If the Supreme Court strikes down President Trump’s tariffs, the Trump administration plans to begin replacing them almost immediately with other levies.

Tariffs on certain raw materials such as steel, aluminum and critical minerals like chromium and tungsten have impacted construction, technology sectors, the automotive industry and indirectly, the lubricants industry as they have raised costs for U.S. manufacturers and consumers and have dampened demand for consumer goods. Nearly 45% of consumers have reported cutting back on nonessential items and 30% have delayed major purchases due to tariff-related price hikes. Additionally, in anticipation of tariffs, some businesses and consumers accelerated imports in the first half of 2025, creating a temporary, artificial surge in demand before a sharp, subsequent drop, according to trade and business data released by the Congressional Budget Office, the Budget Lab at Yale, the Center for American Progress and other organizations.

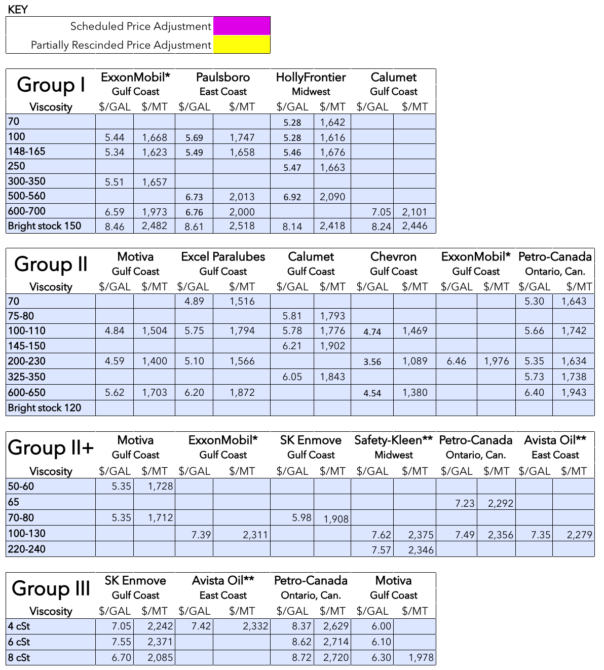

Group I

A similar trend to that seen over the last few weeks persisted, with API Group I prices exposed to downward pressure due to lackluster demand and plentiful inventories. Ample supplies on a global scale meant that producers had fewer opportunities to place their products elsewhere, with the exception perhaps of bright stock, which has enjoyed steady demand in the domestic market, as well as an uptick in buying interest from Brazil.

While some buyers have already stepped forward with product inquiries, others held off on purchases for as long as possible in hopes of reduced pricing. Talk about lower spot prices for the heavy grade, with decreases of one to two cents per gallon mentioned, encouraged those buyers who had sufficient stocks to wait for larger discounts. On the other hand, there were discussions for spot cargoes of bright stock taking place at steeper prices, with small increases of one to two cents per gallon mentioned, because of a tightening of this grade and emerging export opportunities.

The focus of export business remained Brazil, as Brazilian producer Petrobras’ base oils plant was heard to have suffered an unexpected and extended shutdown in October. The supplier has been unable to meet all of its domestic requirements, although its ability to supply Group I cuts was improving compared to late last year. The tight conditions of bright stock in Brazil drove domestic prices up in January, while the Group I light grade experienced a decrease. The SN500 cut was reported as steady. It remains to be seen whether domestic prices are adjusted again in February. Several cargoes of Group II grades had also been available in Brazil and those blenders who were able to replace Group I cuts with Group II base oils opted for doing so as prices were competitive. But it was not clear whether the export opportunities would last as demand typically weakens in January and February during the summer holidays and Carnival in Brazil.

U.S. suppliers have also set their sights on export business to Mexico, where buying interest has started to improve, but the conclusion of deals appeared to be rather elusive since buyers’ price expectations did not meet offer levels. The availability of rerefined grades and Asian material also meant that suppliers had to deal with additional competition.

There were no Group I plant turnarounds scheduled for the first half of the year. Paulsboro plans to embark on a maintenance shutdown at its plant in New Jersey in the last quarter of 2026.

Group II

Despite abundant supplies of most grades, Group II spot prices were holding at steady levels, with the exception of the 600N, which saw moderate downward adjustments of about 4 cents/gal to 5 cents/gal week on week on lengthening supplies and muted buying appetite. The heavy grades in general see reduced demand during the colder months of the year. At least one supplier was heard to have no spot supplies of the light grade to offer for export business.

Aside from a soft domestic market and limited volumes of some grades, suppliers were facing reduced export opportunities as most base oils are oversupplied on a global scale. Steep freight rates and ongoing logistical difficulties, some of them related to geopolitical tensions, also narrowed the number of destinations that U.S. supplies might be shipped to. Typically, India is the receiver of vast amounts of U.S. Group II grades, but last year and the beginning of 2026 saw fewer cargoes moving there given plentiful Asian supplies offered at competitive levels and somewhat sluggish demand from Indian consumers. Additionally, the availability of domestic base oils as Indian plants were running well also reduced the need for imports. In the coming years, a number of new plants were expected to come online in India and this will gradually diminish demand for imported base oils.

U.S. producers also saw some competition with rerefiners in Mexico. In a way, rerefined product was a welcome alternative because the 100N remained relatively tight in the U.S. Rerefiners also reported tightening supplies as an upcoming maintenance program at a rerefinery in the first part of 2026 was anticipated to limit availability. The producer was expected to start building inventories ahead of the shutdown and will likely restrain spot supplies, while availability of discounted products has dried up, according to reports.

Group III

Spot prices in the Group III segment were softer, due mainly to oversupply conditions and expectations of additional import cargoes from Canada, Asia and the Middle East arriving over the next couple of months. The imported volumes in the U.S. are largely absorbed by blenders who serve the PCMO segment given the growing need for high-performance base oils, although demand for cooling fluids, which require Group III base oils has also been expanding.

The heavy grades in particular were exposed to downward pressure because of ample supplies, with market transactions recently heard concluded at lower levels for the 6 cSt and 8 cSt grades as they were more readily available. Oversupply conditions were not exclusive to the U.S., with sales opportunities in other regions being reduced by plentiful supplies and lackluster demand. However, the U.S. still attracts large volumes of imports because of more attractive prices. While domestic demand was not anticipated to improve over the next few weeks, there should be an uptick ahead of the lubricant production season in the spring when blenders prepare for the busy summer driving and oil change season.

Domestic production of Group III grades and rerefining output were not impacting current spot prices directly as producers were using their Group III base oils as correction fluids or for downstream lubricant production.

Naphthenics

Naphthenic base oils were described as ample and more than sufficient to cover current domestic requirements. However, a slight supply tightening may occur this month as San Joaquin Refining plans to embark on a three-week routine turnaround at its refinery in California in late January and was expected to have started to build inventories to cover contractual obligations during the outage. Ergon was still heard to be snug on some grades following an extended turnaround and upgrade at its Vicksburg, Mississippi, plant last year.

Prices for naphthenic oils had been lowered into some accounts earlier this month, with some of the reductions linked to diesel prices as contracts are indexed against a number of different feedstocks. However, no market-wide announcements have been heard.

Demand from the tire and rubber segments was not expected to increase significantly until the spring season gets underway, but requirements for the light grades from the transformer oil sector have held their own. Export opportunities have been limited by oversupply conditions in other regions.

Crude Oil

Crude oil futures fell on Wednesday given an expected build-up of U.S. crude inventories, which offset upward price pressure from a temporary halt in output at two large fields in Kazakhstan. U.S. threats of fresh tariffs on goods from several European nations that oppose its bid to gain control of Greenland also caused crude oil volatility.

- West Texas Intermediate March 2026 futures settled on the Nymex at $60.36 per barrel on Jan. 20, down from $61.15/bbl for front-month futures on Jan. 13.

- Brent futures for March 2026 delivery were trading on the ICE at $64.01/bbl on Jan. 21, down from $65.08/bbl for front-month futures on Jan. 14.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $61.40/bbl on Jan. 16. There was no trading on Jan. 19 due to the Martin Luther King Jr. holiday. Spot prices had settled at $60.34/bbl on Jan. 12, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, Jan. 16 (Jan. 12), EIA

New York Harbor: $2.26 per gallon ($2.18/gal)

Gulf Coast: $2.11/gal ($2.04/gal)

Los Angeles: $2.21/gal ($2.06/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices January 21, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner