Base oil prices were generally stable this week given that there has been little change in conditions since the end of the year, with sluggish demand, plentiful supplies and soft crude oil prices weighing on pricing. Several producers implemented price decreases in December, and no further price action has been reported. Meanwhile, producers were heard to be assessing their supply balances. Inclement winter weather in some parts of the United States have caused transportation disruptions. Some of the market attention turned to the U.S.’ military incursion into Venezuela and the capture of Venezuelan president Nicolás Maduro and his wife over the weekend, as participants expected the news to cause a stir in crude oil markets.

U.S. president Donald Trump’s assertion that Venezuela would be “turning over” up to 50 million barrels of oil to the U.S., and that the U.S. oil industry would be “up and running” in Venezuela within 18 months was expected to cause further concern among investors about oversupply and depressed prices. However, experts noted that any potential Venezuelan oil output would not have an immediate effect, adding that even in the best of circumstances, once safety, security and an advantageous fiscal framework were established in Venezuela, it would take refiners years to restore the country’s oil production, not to mention billions in investment.

Crude oil analysts, for the most part, seemed to shrug off the news about Venezuela, with crude futures trading lower at the start of the week as the focus remained on a potential global supply glut in 2026. OPEC+ members held a meeting on Sunday and reiterated their intention of keeping output unchanged until at least April.

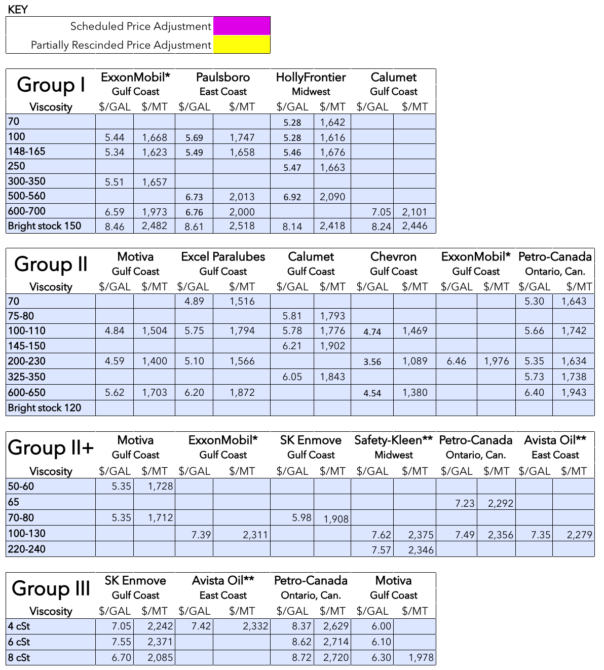

Over the last few weeks of the year, several base oil producers, including Chevron, ExxonMobil, Paulsboro and HollyFrontier, had communicated posted price decreases for most of their API Group I, Group II and Group II+ base oils. Bright stock appeared to be an exception, partly because this grade had been tight for most of the year and prices had consistently held firm. The posted price decreases were heard to have affected mostly contract customers whose agreements are indexed against postings and were likely prompted by a slowdown in demand, ample inventories, a need to capture additional orders and bring posted prices more in line with actual transaction prices.

Group I

Group I base oils have been exposed to downward pressure because of plentiful inventories and sluggish demand, as consumption typically wanes after the end of the summer driving season and does not show a significant uptick until before the spring lubricant production season. Many buyers and sellers had also carried extra inventories to cover potential supply disruptions during hurricane season along the U.S. Gulf Coast and needed to lower stocks before the end of the year.

Furthermore, base oil and lubricant demand has been declining over the last five years, due to several factors affecting automotive lubricant applications, the largest downstream consumer of base oils, which undoubtedly also impacted consumption in 2025. These factors included inflation, fewer vehicle miles driven as many people continued to adopt hybrid or remote work practices following the COVID-19 pandemic, the penetration of electric and hybrid cars, and extended drain intervals in new models of both personal and commercial vehicles that still operate with internal combustion engines.

It was no surprise, therefore, when a few producers stepped out with posted price markdowns in December. ExxonMobil, Paulsboro Refining Co. and HollyFrontier decreased their Group I postings, with the exception of bright stock, by 30 cents per gallon on Dec. 16, Dec. 19 and Dec. 24, respectively. ExxonMobil marked down its Group II and Group II+ grades by 15 cents/gal as well. HollyFrontier (HF Sinclair) also noted that there were no posting changes on its other base stocks.

Aside from attempting to lure domestic buyers with reduced prices, producers also resorted to exports to lower their healthy inventory levels. Some cargoes moved to various destinations in South America, Africa, and the Middle East. Several export transactions were concluded to Brazil, where demand for imports, in particular of the heavy grades and bright stock, had jumped on the back of an unexpected and extended shutdown at the base oil plant of local producer Petrobras in late October. Domestic January prices for most Group I grades fell in Brazil, with the exception of bright stock, which was heard to have edged up due to the snug conditions.

As the year gets into full gear, participants said that activity in Mexico had been healthier than anticipated and that there had been active buying interest, particularly for the light grades. U.S. suppliers were not expected to have made firm offers yet, but were likely to engage in discussions over the next few weeks. There were also expectations that some of the Mexican demand would be fulfilled by rerefined oils. Most Mexican importers have been able to receive or renew their import licenses, while the remaining participants were anticipated to complete the process over the next few weeks, once government agencies resume activities.

Group II

The Group II segment was expected to gradually restore its trading levels following the year-end holidays. Not much fresh business had been achieved by the publishing deadline, as suppliers were assessing inventory levels and arranging logistics for shipments transacted before Dec. 31.

No further posted price adjustments were heard during the week, following Chevron’s and ExxonMobil’s Group II posted price decreases in December, which reflected the prevailing soft market fundamentals. Suppliers did not expect demand to pick up in earnest until February or March, when blenders start to prepare inventories for the busy spring production cycle.

U.S. Group II producers had concluded export business into several destinations in Latin America, Europe and Africa, relieving some inventory pressure. India was one of the main receivers of U.S. cargoes, but volumes were said to be down compared to years past, when several cargoes had made their way to Indian shores in the last few weeks of the year. Ample availability of most grades in Asia, together with steep freight rates and difficulties in making numbers work dampened buying activity in India, sources said.

Rerefiners had also seen steady activity at the end of 2025 and a sudden tightening of some cuts, particularly as rerefiners had been able to place a few cargoes into Mexico. An upcoming maintenance program at a rerefinery in the first part of 2026 was anticipated to strain availabilities since the producer plans to build inventories to meet contract obligations during the shutdown.

Suppliers kept an eye on crude oil market developments because the recent developments in Venezuela were expected to fan nervousness, but the U.S. military action and capture of Venezuela’s president appeared to have had less of an impact than originally anticipated. Nevertheless, there were expectations that sentiment in oil markets would remain bearish due to potential global oversupply conditions. Softer crude oil prices would allow producers to improve margins if base oil price levels were sustained.

Group III

The Group III segment was described as quiet at the start of the new year. The heavy grades continued to be exposed to downward pressure because of lengthening supplies, with market transactions recently reported at slightly lower levels for the 6 cSt and 8 cSt grades in transactions by a particular seller. This was attributed in part to the arrival in the U.S. of several import shipments from Canada, Asia and the Middle East in December, while fresh shipments were scheduled for January as well. Supplies were expected to outpace requirements until demand starts to improve from the PCMO segment as lubricant manufacturers begin to pad base oil inventories for the ramping-up of spring lubricant production in February or March.

Meanwhile, domestic production of Group III grades and rerefining output continued at a steady pace, but most producers were using their Group III base oils as correction fluids or for downstream lubricant production, reducing their impact on the general market.

Naphthenics

Naphthenic base oil prices were stable, although a number of accounts that have contracts indexed against diesel prices may have seen some downward adjustments. Diesel prices had strengthened substantially in early 2025 as Russia, one of the largest diesel exporters, was unable to move diesel out of the country due to international sanctions, as well as the fact that some refineries had been damaged by Ukrainian drone attacks. However, as crude oil prices declined in the latter part of the year, so did diesel prices.

The naphthenics market was described as adequately supplied, especially after the completion of a turnaround at a large facility in October 2025. A slight tightening may occur this month as San Joaquin Refining plans to embark on a three-week routine turnaround at its refinery in California in mid-January and was expected to start building inventories to keep customers supplied during the shutdown. This would coincide with a period of reduced demand for the heavy pale oils from the rubber, tire, grease and process oil segments. Consumption of the light grades, which had been healthy for most of the year due to ongoing demand from the transformer oil and infrastructure segments, had also weakened by year-end, but was likely to see a bump ahead of the spring season.

Crude Oil

Crude oil futures slipped and shares in Asia retreated as markets digested the news of the toppling of Venezuela’s leader amid speculation about the fate of its petroleum reserves. Some analysts said that any additional crude coming from Venezuela would place pressure on oil prices, but lower energy costs could also lead to more optimistic economic growth rates, although geopolitical tensions could also dampen the outlook.

- West Texas Intermediate February 2026 futures settled on the Nymex at $57.13 per barrel on Jan. 6, down from $57.95/bbl for front-month futures on Dec. 30.

- Brent futures for March 2026 delivery were trading on the ICE at $60.21/bbl on Jan. 7, down from $61.33/bbl for front-month futures on Dec. 31.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $59.55/bbl on Jan. 5. Spot prices had settled at $59.34/bbl on Dec. 29, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, Jan. 5 (Dec. 29), EIA

New York Harbor: $2.15 per gallon ($2.16/gal)

Gulf Coast: $2.00/gal ($2.00/gal)

Los Angeles: $2.15/gal ($2.11/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices January 7, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner