Chevron stepped out with a posted price decrease announcement this week – the company’s first price revision since May. The price adjustment took some participants by surprise as a second API Group II producer was preparing to take its plant offline for a turnaround, and this was expected to tighten spot supply and support pricing. At the same time, producers needed to find a home for the extra inventories they had been holding during hurricane season, and often adjust prices in the fourth quarter to entice additional orders.

Chevron announced that the company would be decreasing all of its Group II posted prices by 25 cents per gallon, with an effective date of Sept. 30, “to reflect market conditions.”

Other base oil suppliers were heard to be “assessing the situation.” Some observers were of the opinion that the decrease would bring the company’s posted prices more in line with actual market prices. Lubricant manufacturers hoped the decrease would not increase pressure from customers to lower their own finished products prices as ongoing competition among suppliers has already squeezed margins.

Market players acknowledged that some pockets of the base oils market were slightly oversupplied, and this was exerting downward pressure on prices. The fact that a number of producers—mainly in the Group II segment—were dealing with some length and had pursued export business “is always a good indicator of market softness,” a source noted.

Group I

Domestic prices in the Group I segment were steady, with export values also stabilizing as supplies were generally balanced to tight. There had been a few export transactions concluded in the previous weeks, and regular business to Mexico was ongoing, but export movements appeared to have slowed down, reflecting fewer available cargoes as well as lackluster consumption in other regions. A number of suppliers said that domestic demand had remained healthier than anticipated and that they had limited availability for spot transactions.

U.S. suppliers continued to ship Group I and Group II base oil cargoes to Mexico, with one U.S. supplier in particular offering attractive prices because of a supply overhang. However, there were reports of persistent difficulties with import licenses. The Mexican government has been cracking down on Mexican agents who had illegally brought in fuel shipments that had been declared as lubricant cargoes, which are exempt from Mexico’s Special Tax on Production and Services. While it is also illegal to import base oils into Mexico for diesel extension without a prior permit from the Ministry of Energy, many who had obtained a license were looking for opportunities to move light grades into the fuel extender market. Base oil demand from the lubricant manufacturing sector has declined in Mexico given economic uncertainties, but there were signs that base oil buying interest was starting to pick up as blenders have depleted stocks.

Appetite for U.S. Group I cargoes from Brazil has been weaker than earlier in the year because of increased domestic production and lower prices from the main local producer in September. October prices were anticipated to roll over from the previous month. Bright stock was scarce and was therefore commanding most attention and steeper prices. Some buyers were interested in acquiring Group II grades because they were offered at competitive values and they could be used to replace Group I cuts in some applications. This was exerting downward pressure on Group I prices, particularly of the light grades, which were more plentiful.

Group II

While there was still downward pressure on the mid- and heavy-viscosity Group II base oils, spot prices in this segment have stabilized as participants expected to see tighter conditions following the start of a turnaround at Excel Paralubes’ plant in Louisiana this month. However, some downward pressure on the heavy grades persisted due to a demand slowdown from the industrial lubricant segments due to weaker manufacturing output in the U.S.

Some participants had anticipated the Excel turnaround to offer support to prices, and were therefore surprised about Chevron’s posted price decrease. At the same time, at least a couple of Group II producers were heard to have offered cargoes for export, reflecting oversupply conditions which were partly brought on by suppliers starting to release the extra barrels kept during hurricane season. While producers often revise prices in the fourth quarter, some expected suppliers to hold off on any price revisions until there was a better feel on availability once the Excel turnaround got underway.

Excel Paralubes has been running its Group II/Group III plant at reduced rates for most of the year and the producer planned to shut down the unit for a maintenance program and catalyst change at the beginning of October. The unit was expected to be offline for approximately four to six weeks. Excel had begun to build inventories to cover contractual commitments during the outage and had restricted spot availability, according to sources. There was no direct producer confirmation about the plant’s operations.

It was heard that a number of Group II cargoes had been sold to Indian buyers for September and October shipment, and additional export negotiations were still taking place.

Group III

A combination of growing supplies and slowing demand have started to exert downward pressure on Group III base oils, which had been in a fairly balanced position for most of August and part of September. Participants said that due to the end of the summer driving season in the U.S., automotive lubricant consumption levels had weakened, leading to reduced base oil demand. “The hardest hit market demand-wise seems to be PMCO, which tracks well with softer Group III dynamics,” a source commented, while another noted that “discounts are out there for the right volumes.” A Middle East supplier was heard to have lowered its spot offers to attract buyers.

Furthermore, with Group III demand showing a decline in other regions, Asian and Middle Eastern suppliers were expected to ship their regular volumes to the U.S., where prices were still holding at comparatively attractive levels. Even so, suppliers also noted that freight rates had increased in recent months and might be even more impacted once new U.S. fees begin to be implemented on Chinese owned and/or operated vessels. The proposed fees were scheduled to go into effect on Oct. 14 and have prompted ship operators to rearrange their vessel line-ups and move vessels built in China off U.S. routes. Fewer ships were already covering transpacific routes due to the sweeping tariffs imposed on some imports by U.S. president Donald Trump, which had prompted a fall in demand for these goods. As a result, vessel space was tight on certain routes and freight rates have moved up, according to sources.

Additionally, several U.S. producers are now able to manufacture Group III grades and while most of these volumes are used for intra-company lubricant production, the situation has led to reduced demand for Group III imports.

In the U.S., Excel Paralubes was anticipated to shut down its Group II and Group III plant in Lake Charles for maintenance in October. However, the impact of the turnaround on the domestic market was expected to be limited as the unit produces Group III volumes for the company’s own internal consumption. Excel Paralubes does not comment on its production status.

Naphthenics

Prices for naphthenic base oils were reported as largely stable, supported by a balanced-to-tight supply and demand scenario. The current turnaround at Ergon’s naphthenic base oils plant in Vicksburg, Mississippi, was expected to keep spot supplies on the tight side, although reduced requirements for grease production linked to the shutdown of Smitty’s plant in Vicksburg following an explosion and fire in August had temporarily freed up some barrels.

Ergon started a 45-day maintenance program at its refinery on Sept. 1.The company announced that various operating units of the refinery would be down as several reliability improvements will be implemented. Ergon’s current ratable customers were not expected to suffer any supply disruptions because the producer built sufficient inventories ahead of the shutdown to support contract requirements, but the company was likely to restrict spot sales.

While a second naphthenic refiner was heard to be running at top rates, a large portion of its output was expected to move overseas. Domestic pale oil production was more than adequate to meet current demand levels, particularly as consumption of the heavy grades was still weak compared to the lighter grades moving into the transformer oil segment. The heavy grades serve the rubber and tire industry and activity in this segment has slowed down due to the end of the summer driving season in early September.

Crude Oil

Crude oil futures steadied on Wednesday after sustaining heavy losses in the early part of the week because of growing concerns about oversupply if OPEC+ decides to increase output again in November. Signs of dwindling U.S. crude oil inventories limited the losses. Geopolitical tensions related to the conflict in Ukraine and the U.S. government shutdown that started on October 1 and threatened to disrupt government operations and delay the release of key economic data also impacted prices.

West Texas Intermediate November 2025 futures settled on the Nymex at $62.37 per barrel on Sept. 30, down from $63.41/bbl for front-month futures on Sept. 23.

Brent futures for December 2025 delivery were trading on the ICE at $65.61/bbl on Oc. 1, down from $68.34/bbl for front-month futures on Sept. 24.

Louisiana Light Sweet crude wholesale spot prices were hovering at $66.57/bbl on Sept. 29, up from $65.19/bbl on Sept. 22, according to the U.S. Energy Information Administration

Diesel

Low-sulfur diesel wholesale, Sept. 29 (Sept. 22), EIA

New York Harbor: $2.39 per gallon ($2.35/gal)

Gulf Coast: $2.28/gal ($2.24/gal)

Los Angeles: $2.44/gal ($2.44/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

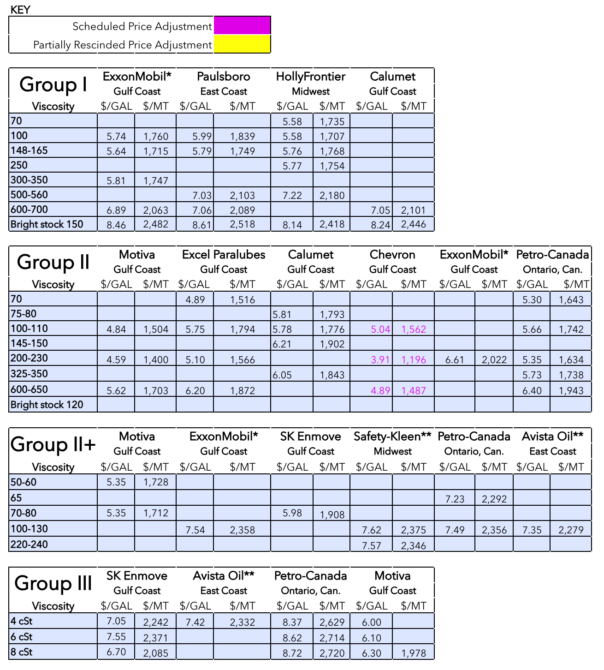

Posted Paraffinic Base Oil Prices September 24, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner