Following a tenuous ceasefire between Israel and Iran last week, crude oil prices slumped, easing concerns about potential base oil posted price increases triggered by earlier price spikes. The lower oil prices reestablished a sense of stability and muffled discussions about potential base oil hikes. Most base oil segments remain balanced to slightly tight, supporting steady pricing, although some corners of the market continued to show more strained conditions than others due to recent and upcoming turnarounds. Demand was at anticipated levels for the summer, but suppliers have tempered their expectations as base oils and lubricants consumption has been on a downward trend for the last two years.

Crude oil futures have fallen back to values seen before the conflict started, relieving some of the pressure on base oil pricing. Producers have turned their attention to making sure they have adequate inventories to deal with possible output disruptions during the hurricane season, while meeting contract commitments.

Demand continues to be described as healthy by some producers, and lackluster by others, depending on what downstream segments these suppliers cater to. Base oils that are used in automotive applications had seen an uptick in demand before the summer driving season kicked off in late May because lubricant manufacturers had started to prepare for the peak oil change months when numerous drivers take to the road. With the July 4 holiday weekend coming up, the number of people traveling was expected to jump. Following a busy holiday weekend and summer vacation travel period, requirements were anticipated to slow down.

At the same time, factory-fill lubricants have seen a drop in demand due to production disruptions caused by the tariff upheaval that started earlier this year. Several countries were in the midst of negotiations with U.S. president Donald Trump and his envoys to reach agreements that would potentially eliminate the high duties that the president has threatened to implement, but that have been put temporarily on hold until July 9. The approach of the deadline prompted some manufacturers to front-load certain products that were expected to be subject to tariffs. It was unclear how the tariffs would affect automotive imports from Japan. On Tuesday, president Trump said that he doubted a trade deal with Japan could be reached before the July 9 deadline, adding he was considering raising tariffs on Japanese imports to 30% or 35%.

Group I

The tight fundamentals observed in the API Group I segment have started to fray, with the heavier cuts becoming more readily available as planned turnarounds at several facilities have now been completed and demand has started to ease. Even bright stock, which had been difficult to obtain in sizeable quantities, has started to lengthen. Nevertheless, a supplier was heard to be unable to meet additional requests for product as it was prioritizing contract commitments and didn’t have any extra availability for the time being.

A number of plant maintenance programs have been completed in recent weeks. Calumet was expected to complete a turnaround at its Group I/Group II unit in Shreveport, Louisiana, in late June. The turnaround only affected heavy Group I grades. The company performed maintenance on the lighter viscosity base oil lines last March.

American Refining Group was also heard to have completed a turnaround at its Group I plant in Bradford, Pennsylvania, last month, according to sources.

Ergon has rebuild inventories following a turnaround at its Group I/Group II unit that lasted from the end of March until mid-May and has been able to continue supplying its ratable customers even during the outage.

There was still buying interest from Mexican buyers and importers for U.S. Group I and Group II base stocks, but volatility in crude oil prices had prompted some participants to rush in and secure cargoes in case base oil prices went up. Then, when crude values fell, many buyers decided to take a step back and wait until prices stabilized. Economic uncertainties also dampened buying appetite.

Group II

In this segment, supply was expected to lengthen because plants have resumed production following maintenance programs. The recent turnarounds, along with reduced operating rates at some plants had strained Group II spot supplies, but as most units increase operating rates, additional spot volumes were expected to become available, although the light grades were still described as snug.

Chevron’s plant in Pascagoula, Mississippi, restarted in late May following a turnaround, but the producer was heard to have been able to find a home for rall the extra barrels that had become available after it had rebuilt inventories, according to sources.

Motiva restarted its plant in mid-June and was building inventories, following a three-week turnaround at its Port Arthur, Texas, hydrocracker that began in late May. The shutdown was anticipated to have affected mainly the Group II 220N grade, but stocks have been mostly replenished, and there were reports that the supplier had some extra availability for export.

Excel Paralubes was heard to continue running its Lake Charles, Louisiana, plant at reduced rates, but contractual obligations are being met. The supplier was heard to be building inventories for the hurricane season and had restricted its spot sales. The production issues were not expected to be resolved until the plant’s scheduled turnaround in October, according to sources. Chevron, Motiva and Excel Paralubes did not comment on the status of their operations.

Ergon completed a seven-week turnaround at its Group I/Group II base oil unit in Newell, West Virginia, and restarted its plant on schedule in the second half of May.

Spot rerefined base oil cargoes were also scarce given recent and upcoming shutdowns. At least one rerefiner reported a sold-out position for the next 4-5 weeks given healthy demand and additional orders from buyers who were eager to pad inventories during hurricane season.

There were reports that a rerefiner’s plant had suffered some production setbacks, following a turnaround, which may have exacerbated the current tight supply situation.

Avista may be embarking on a short turnaround in September. The company was heard to be running its rerefining plant in Georgia at record rates and has recently completed an expansion, bringing its capacity up to 1.15 million barrels per year.

Group II was still fairly tight in the U.S., narrowing the possibilities of concluding spot export transactions, but cargoes continued to move to Mexico, although Mexican importers were still dealing with some difficulties in renewing or receiving import licenses from the Mexican government. These licenses were issued to restrict the illicit import of light base oils that are used in fuel blending.

Domestic base oil prices in Brazil were heard to have softened, making them more attractive than most U.S. offers. Spot supply from the U.S. was still fairly snug in any case, limiting options, while buyers were also hesitant because of crude oil price volatility and global economic uncertainties.

Group III

With hurricane inventory building efforts underway in the U.S. and the global supply situation still showing signs of tightness, Group III base oil prices have remained on firm footing, with spot prices inching up by one to two cents per gallon this week. The U.S. imports most of the Group III base oils it consumes from Canada, Asia and the Middle East, and turnarounds in those regions have curtailed spot availability.

There had been some concern that Group III import shipments from the Middle East could see disruptions given the Israel-Iran conflict and a possible closing of the Strait of Hormuz. However, the agreed cease-fire should reduce that risk and allow for shipments to continue, although uncertainties lingered. Increased supply was expected to gradually become available from Canada, following Petro-Canada’s inventory rebuilding efforts after a turnaround earlier in the year.

In South Korea, SK Enmove’s Group III plant in Ulsan has completed a partial two-month turnaround that started in May, although the shutdown was not expected to have a significant impact on supplies because of uninterrupted production on the facility’s other trains, company sources said.

In the Middle East, Adnoc completed a turnaround at its Group II/Group III plant in Ruwais, Abu Dhabi, United Arab Emirates, that started in May. The unit has restarted.

Naphthenic base oils

Naphthenic base oil producers were also keeping a close eye on crude oil prices as margins had been suddenly squeezed when crude futures shot up, with some suppliers making overtures towards raising base oil prices. However, crude futures have retreated and this granted some relief.

Most pale oils displayed balanced-to-tight conditions, although the light grades were in high demand in the transformer oil segment, while the tire and rubber segments, which call for heavier viscosities, were less dynamic. Supply was expected to become more limited as a producer was understood to be building inventories ahead of its turnaround in September.

Ergon has scheduled a maintenance program at its naphthenic refinery in Vicksburg, Mississippi, beginning September 1. Various operating units of the ERI refinery will be down for approximately six weeks as several reliability improvements will be implemented. No supply interruptions were expected for Ergon’s current ratable customers, as product inventory levels were anticipated to be sufficient to support sales during the planned shutdown, company sources said.

Crude Oil and Diesel

Crude oil futures settled slightly up on Tuesday as analysts awaited an OPEC+ decision regarding upcoming output levels, while there were also signs of steady global oil demand.

On July 1, West Texas Intermediate August 2025 futures settled on the Nymex at $65.45 per barrel, compared to $64.37/bbl on June 24.

Brent futures for September 2025 delivery were trading on the ICE at $67.15/bbl on July 1, from $68/bbl for August futures on June 24.

Louisiana Light Sweet crude wholesale spot prices were hovering at $68.60/bbl on June 30, compared to $71.86/bbl on June 23, according to the U.S. Energy Information Administration.

Low sulfur diesel wholesale spot prices were at $2.37 per gallon at New York Harbor, $2.30/gal on the Gulf Coast and $2.54/gal in Los Angeles on June 30, compared to $2.34/gal, $2.27/gal and $2.40/gal, respectively, on June 23, according to the EIA.

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

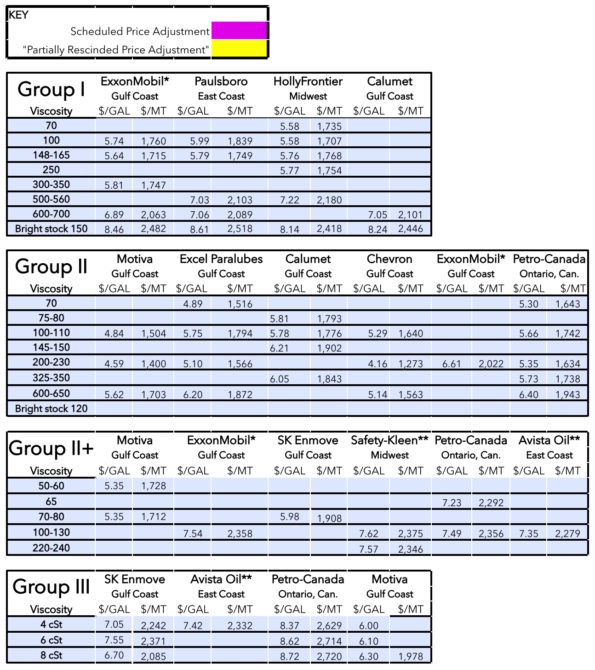

Posted Paraffinic Base Oil Prices

July 2, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner