It has been a historic week of geopolitical developments. Israel and Iran pulled back from all-out war after the United States bombed Iranian nuclear facilities on Saturday and the two belligerents called for a ceasefire. Whether the cessation of attacks holds remains to be seen.

With tensions running so high, it was no surprise to see extreme volatility in crude oil markets amid concerns of reduced supply and a possible closing of the Strait of Hormuz. While the conflict did not necessarily impact U.S. base oil prices directly, potential production and shipping disruptions in the Middle East could have repercussions for base oil markets everywhere as participants face higher crude oil and feedstock values, as well as increased freight rates.

Operations at Middle East ports did not appear to have suffered major disruptions, but the conflict between Israel and Iran has triggered heightened risks and insurance costs for maritime traffic in the region. Maersk, a major shipping company, temporarily suspended vessel calls and cargo acceptance at Israel’s Port of Haifa, while some shipping groups have made carrier route adjustments to steer clear of the Strait of Hormuz, a crucial waterway for oil and container traffic, according to CNBC. The conflict has also exacerbated the ongoing situation in the Red Sea, where Houthi rebels have been attacking commercial vessels, causing major disruptions and rerouting of ships around Africa. Airlines have changed flight paths or suspended air traffic to avoid flying near the affected territories as well.

Predictably following all the latest developments, crude oil futures displayed extreme volatility. Futures jumped by as much as 13% when news about the Israel-Iran conflict were first announced on June 13. A few days later, prices gave up much of their gains when it became clear that the airstrikes had not damaged energy infrastructure. Values surged once again after the U.S. bombed Iranian nuclear facilities on June 21, but prices plummeted soon after–hitting their lowest level in two weeks–as Israel agreed to U.S. President Donald Trump’s proposal for a ceasefire with Iran, assuaging worries of supply disruptions in the Middle East.

Meanwhile, base oil prices were reported as stable-to-firm, but refiners were monitoring crude oil prices closely because margins would remain squeezed and base oils would be more exposed to upward pressure if crude oil values remained at high levels for an extended stretch of time. Some suppliers were waiting for clearer signs before stepping back into the market with fresh offers. A few buyers ventured out to secure additional cargoes to build inventories ahead of potential price hikes.

Despite ongoing buying interest at destinations such as Mexico and Brazil, U.S. export volumes have declined due to slim availability of some grades, along with steep pricing and a reduced number of offers. Suppliers did not appear pressured to find a home for their extra volumes as they opted for padding inventories to cover possible output disruptions during the hurricane season.

Group I

Tight conditions of some Group I cuts persisted, lending support to firm prices, with spot indications for the light grade SN150 moving up by a couple of cents per gallon as demand has picked up in the last four to six weeks, according to sources. This was partly driven by tight Group II supply and buyers seeking Group I cuts as a substitute. While a few downstream segments such as industrial and metalworking fluids have shown weaker activity, other sectors maintained steady consumption.

Bright stock continued to attract much attention because it is a difficult grade to replace and global production has declined in recent years given permanent plant shutdowns and routine turnarounds. However, prices were reported as largely stable during the week. A supplier mentioned receiving many inquiries for bright stock, but being unable to meet them because it didn’t have any availability at the moment.

Group I turnarounds in Southeast Asia, Japan, China and the Middle East have reduced supplies in those regions, prompting buyers to look for availability in other regions. U.S. supplies were limited because of a couple of U.S. turnarounds that had also reduced domestic availability.

Calumet will be completing a turnaround at its Group I/Group II unit in Shreveport, Louisiana, this month. The turnaround will only affect the Group I heavy grades. The company performed maintenance on the lighter viscosity base oil lines last March.

American Refining Group was also heard to have planned a turnaround at its Group I plant in Bradford, Pennsylvania, this month, according to sources.

Ergon was heard to be rebuilding inventories following a turnaround at its Group I/Group II unit that lasted from the end of March until mid-May. The producer had also built inventories ahead of the shutdown to continue supplying its ratable customers.

Mexican buyers and importers have shown steady buying interest for U.S. base oils, with the light grades particularly sought after. While some buyers had delayed purchases in hopes of negotiating lower prices later on, when supply starts to grow following the summer driving season, the sudden increase in crude oil values prompted many to secure cargoes to avoid potential upward price revisions.

While appetite for U.S. base oils from Brazil had been lackluster over the last couple of months due to increased local production and improved availability of imports from neighboring countries such as Argentina, there had been a short-lived uptick in inquiries given improved activity in downstream lubricant segments. However, recent developments in the Middle East and the rise in crude oil values have imbued the market with fresh uncertainties, which translated into subdued demand for base oils and lubricants.

Group II

The light grades continued to show more limited availability than their heavy-vis counterparts. This was partly attributed to a ramping up of Group III production at some refineries, to the detriment of Group II output. Group II suppliers have been trying to manage stocks carefully to meet contract obligations and still have some spot availability.

“From a Group II and Group III standpoint, we had a very strong start to the year and don’t see any weakness in that part of the market. In fact, it has been challenging to manage demand above expectations,” a source commented.

Recent and ongoing turnarounds have strained Group II spot supplies. A market participant who was looking for additional Group II base oils to supplement its supply noted that it had been more difficult than expected to find key stocks that had been reportedly long, such as the 220N and 600N, with prices also higher than anticipated. As plants resume production, more product was expected to be introduced into the market.

Chevron’s plant in Pascagoula, Mississippi, restarted in late May following a turnaround, but the producer was heard to have been able to place all the extra barrels that had become available after it had built inventories, according to sources.

Motiva restarted its plant earlier this month and was building inventories, following a three-week turnaround at its Port Arthur, Texas, hydrocracker that began in late May. The shutdown was anticipated to have affected mainly the Group II 220N grade, but stocks have been replenished, and there were reports that the supplier was considering an export transaction for shipment to India.

Excel Paralubes was heard to continue running its Lake Charles, Louisiana, plant at reduced rates, but contractual obligations are being met. The supplier was heard to be building inventories for the hurricane season and had restricted its spot sales. The production issues were not expected to be resolved until the plant’s scheduled turnaround in October, according to sources. Chevron, Motiva and Excel Paralubes did not comment on the status of their operations.

Ergon completed a seven-week turnaround at its Group I/Group II base oil unit in Newell, West Virginia, and restarted its plant on schedule in the second half of May.

A one-month turnaround at Safety-Kleen’s rerefining unit had been expected to curb availability of some of its rerefined products, but the plant was heard to be running now, while another rerefiner was understood to be completing maintenance in June. Most rerefiners were reportedly offering limited supplies into the spot market.

There continued to be buying interest from Brazil and Mexico, which appeared to increase with the ascent of crude oil futures as buyers were concerned that base oil prices would follow suit. However, Group II was still fairly tight in the U.S., limiting spot availability for export, and Mexican importers were still dealing with some difficulties in renewing or receiving import licenses from the Mexican government.

Group III

Global supply in the Group III segment remained tight given recent and ongoing turnarounds. Sources indicated that they had not noticed any shortages, but “not a lot of spot product floating around either.” Buyers and suppliers were also acquiring extra barrels to build inventories ahead of potential output disruptions during the peak of the hurricane season in August and September.

There was also some concern that Group III import shipments from the Middle East could face challenges if the Israel-Iran conflict continued and shipping were affected by suspended port operations or the closing of the Strait of Hormuz. On Tuesday, news that a cease-fire agreement had been reached seemed to assuage some of these concerns, although it was not clear how long the cease-fire would last.

A North American Group III producer had restricted supplies to its customers to their forecast for a few weeks coming out of turnaround, but those restrictions have been lifted.

In South Korea, SK Enmove’s Group III plant in Ulsan was undergoing a partial two-month turnaround that started in May, although the shutdown was not expected to have a significant impact on supplies because of uninterrupted production on the facility’s other trains, company sources said.

In the Middle East, ADNOC completed a turnaround at its Group II/Group III plant in Ruwais, Abu Dhabi, United Arab Emirates, that started in May. The unit has been restarted.

Bapco was heard to have originally scheduled a turnaround at its Group III facilities in Sitra, Bahrain, in late March or early April, but has reportedly postponed it. No updates could be obtained by the publishing deadline.

Naphthenic base oils

As was the case for paraffinic market participants, naphthenic base oil producers were also watching developments on the crude side very closely as price fluctuations typically have a more direct impact on pale oil prices. Suppliers appeared reluctant to adjust prices until a clearer picture emerged and crude prices remained at a certain level for an extended period.

A balanced supply and demand ratio offered support to stable pale oil prices, although the light grades continued to see stronger demand than the heavier viscosities as consumption in the transformer oil segment was healthy, while the tire and rubber segments were sluggish. There was limited extra supply available as a producer was understood to be building inventories ahead of its turnaround in September.

Crude Oil and Diesel

Crude oil futures fell sharply on Tuesday after Israel and Iran agreed to a ceasefire–though the deal came close to collapse—and analysts were less worried about supply issues. President Trump said China can keep buying oil from Iran, but clarified that sanctions remained in place, while urging Chinese refiners to purchase crude from the U.S.

On June 24, West Texas Intermediate August 2025 futures settled on the Nymex at $64.37 per barrel, compared to $74.84/bbl for July futures on June 17, and $64.98/bbl on June 10.

Brent futures for August 2025 delivery were trading on the ICE at $68/bbl on June 24, from $76.40/bbl on June 17, and $66.87/bbl on June 10.

Louisiana Light Sweet crude wholesale spot prices were hovering at $71.86/bbl on June 23, compared to $75.63/bbl on June 16 and $68.74/bbl on June 9, according to the U.S. Energy Information Administration.

Low sulfur diesel wholesale spot prices were at $2.34 per gallon at New York Harbor, $2.27/gal on the Gulf Coast and $2.40/gal in Los Angeles on June 23, compared to $2.40/gal, $2.31/gal and $2.46/gal, respectively, on June 16, according to the EIA.

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

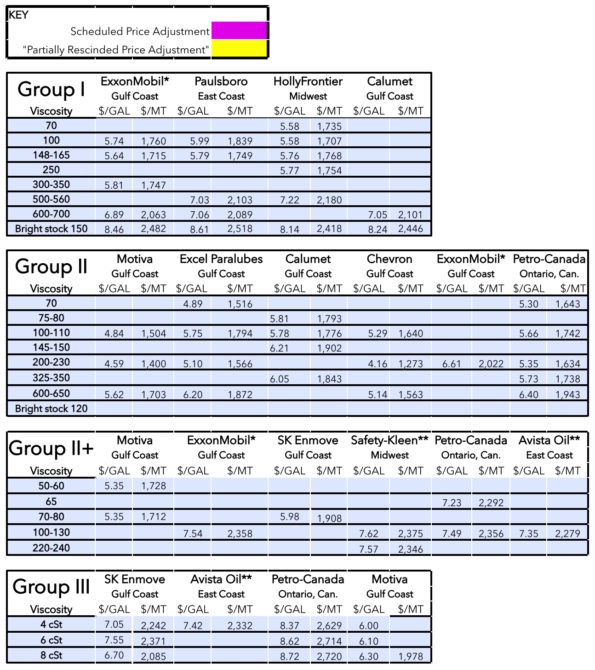

Posted Paraffinic Base Oil Prices

June 25, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner