Base oil prices were reported as steady-to-firm, with market participants keeping an anxious eye on crude oil futures, since prices have climbed, following several weeks of steady decline. Some base oil suppliers reported consumption at expected levels, while others said that certain applications had started to show weaker conditions. With the hurricane season on many participants’ minds, part of the current demand was thought to be related to stockpiling efforts to cover requirements in the event of output disruptions caused by severe weather. Forecasters at the National Oceanic and Atmospheric Administration have predicted above-normal hurricane activity in the Atlantic basin this year.

Crude oil futures strengthened on optimism regarding a possible resolution to the ongoing trade war between the United States and China, as representatives of the two nations met to try to restore the flow of rare earth minerals and reach a deal that would lower the tariffs imposed on each other.

Crude oil prices lost considerable territory since early April, when West Texas Intermediate futures had been hovering near $71/bbl. By late May, futures had fallen to around $60/bbl but were trading near $65/bbl this week.

A paraffinic base oil producer implemented a 20-cents-per-gallon decrease in mid May, thought to be driven by the lower crude oil values and expectations of increased supply after the refiner’s base oil plant resumed production following a routine turnaround. No other initiatives had emerged at the time, but other producers were closely monitoring market conditions to evaluate potential price changes.

Downstream, lubricant and finished products manufacturers were dealing with firm production costs and customer pressure to maintain or reduce prices, even though the cost of many inputs has climbed. Freight rates for rail and truck transportation of base oils have also increased, and the hikes have been passed on to buyers. Competition among suppliers also limited their options in terms of revisions for finished products. Some blenders were heard to be requesting temporary value allowances (TVAs) on base oils, but there were no reports of TVAs having been granted.

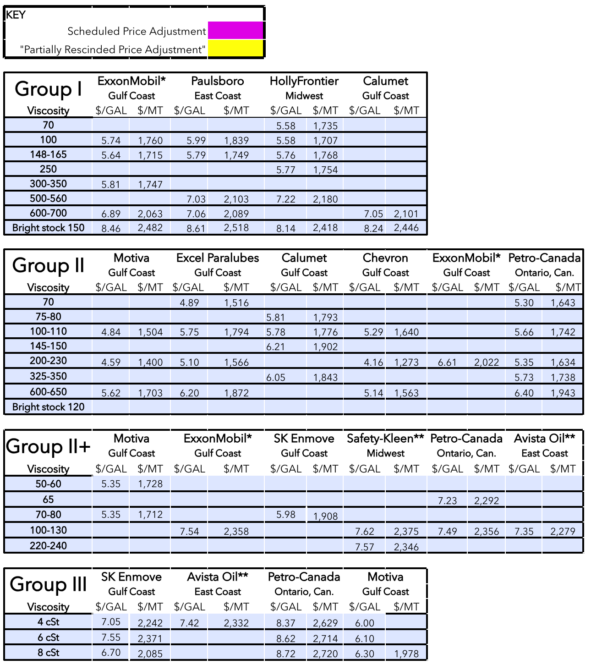

Group I

The tight API Group I supply and demand ratio seen of late has started to ease as demand from some applications, mainly those related to industrial activities, has declined. However, bright stock continued to outshine its counterparts as interest for this grade remained healthy, supporting firm pricing. A supplier appeared to have extra supplies of Group I grades and these were heard to have been offered into the spot export market.

The Group I segment was expected to remain on the tight side for a while longer, though, since a number of recent and imminent plant turnarounds, not only in the U.S., but in other regions as well were expected to trim global availability.

Calumet will be completing a turnaround at its Group I/Group II unit in Shreveport, Louisiana, this month. The turnaround will only affect the Group I heavy grades. The company performed maintenance on the lighter viscosity base oil lines last March.

American Refining Group was also heard to be preparing for a turnaround at its Group I plant in Bradford, Pennsylvania, according to sources.

Ergon was heard to be rebuilding inventories following a turnaround at its Group I/Group II unit from the end of March until mid May. The producer said that there were no supply interruptions for ratable customers as the company had built inventories ahead of the shutdown.

In Mexico, there is ongoing buying appetite for Group I grades and prices have edged up on limited availability of U.S. barrels. Some buyers have turned to Group II supplies as they seemed to be more readily available, but they were certainly not abundant either. Buyers with immediate needs were acquiescing to current offers, but others preferred to delay purchases for as long as possible in hopes of attaining lower prices once more product comes into the market.

There has also been appetite for Group I grades from Brazil, but limited availability of these cuts – the heavy-viscosity grades and bright stock in particular – have pushed spot export prices up, while domestic Group I prices in Brazil were heard to have been adjusted down.

Group II

Spot prices for a number of Group II grades were heard to have come under pressure on growing supplies and a recent posted price decrease. However, sources said that the excess supply that had entered the domestic market following the restart of Chevron’s plant in Pascagoula, Mississippi, in early May had been cleared, and this had helped stabilize domestic pricing and had also started to exert upward pressure on export offers.

At the same time, once Motiva restarts its plant and begins to build inventories, following a turnaround, more barrels were likely to become available and this could weaken some of the price support for Group II grades. Motiva had scheduled a three-week turnaround at its Port Arthur, Texas, hydrocracker that started in late May and was expected to be completed by the end of the week. The shutdown was anticipated to affect mainly the Group II 220N grade.

For the time being, Group II producers appeared to be sold out of 100N, 220N and 600N spot barrels, with some of the supplies understood to have moved to Mexico.

Excel Paralubes was heard to continue running its Lake Charles, Louisiana, plant at reduced rates, but contractual obligations are met. The supplier was heard to be building stocks ahead of the hurricane season and had restricted its spot sales. The production issues were not expected to be resolved until the plant’s scheduled turnaround in October, according to sources. Chevron, Motiva and Excel Paralubes did not comment on the status of their operations.

Back in late March, Ergon had started a seven-week turnaround at its Group I/Group II base oil unit in Newell, West Virginia, to complete maintenance and implement several reliability improvements. The plant was heard to have been restarted as planned in the second half of May.

Additional Group II availability was expected to be offered by rerefiners, whose plants were heard to be running well following brief turnarounds at several facilities, but the extra volumes were still deemed small. A turnaround at a rerefining unit this month could also crimp available supplies.

Buying interest from Brazil for Group II grades has ticked up as inventories have been drawn down in that country, particularly for the lighter grades. Given a snug supply situation and limited availability in the U.S., spot export price indications have inched up.

Group III

Spot prices for Group III base oils have edged up on tight availability, not only in the domestic market, but on a global scale given ongoing plant turnarounds. This has led to fewer spot import cargoes being offered in the U.S. Higher prices in Europe are enticing sellers to move more product into that region. Tighter supply of the 4 cSt grade versus the 6 cSt and 8 cSt grades led to steeper spot prices for this cut, with values edging up by a few cents per gallon week on week.

Domestic Group III production was also heard to have been reduced as producers who can also manufacture Group II grades have increased Group II output as they rebuild inventories or stockpile products ahead of the peak hurricane period in August and September.

In North America, Group III supplies had improved following the restart of Petro-Canada’s Group III plant in Mississauga, Canada, in early May after the producer completed a turnaround. The Group II unit at the same location continued to operate during the Group III maintenance program. However, ongoing turnarounds in other parts of the world have constrained Group III supplies.

In South Korea, SK Enmove started a partial two-month turnaround at its Group III plant in Ulsan in May, although the shutdown was not expected to have a significant impact on supplies because of uninterrupted production on the facility’s other trains, company sources said.

In the Middle East, Adnoc started a two to three-week turnaround at its Group II/Group III plant in Ruwais, Abu Dhabi, United Arab Emirates, in early May.

Bapco was heard to have scheduled a 10-week turnaround at its Group III facilities in Sitra, Bahrain, which was originally scheduled to start in late March or early April, but was reportedly postponed to early June.

Naphthenic base oils

Naphthenic base oil prices remained stable, following 20 cents-per-gallon price decreases implemented on a majority of grades in mid-May, with the exception of one refiner who did not adjust the pale 60 cut. The adjustments were said to have been prompted by lower crude oil and feedstock prices and growing supplies of the heavier grades.

The light grades remained fairly tight given robust demand from the transformer oil and process oils segments, while the heavier pale oils that move into the tire and rubber segment were seeing more moderate consumption. A further tightening of supplies was likely to materialize in the second half of the year as Ergon Refining Inc. will be embarking on a turnaround and was likely to start building inventories to cover requirements during the outage.

Ergon has scheduled a planned maintenance event at its naphthenic refinery in Vicksburg, Mississippi, beginning Sept. 1. Various operating units of the ERI refinery will be down for approximately six weeks as several reliability improvements will be implemented. No supply interruptions were expected for Ergon’s current ratable customers, as product inventory levels were anticipated to be sufficient to support sales during the planned shutdown.

Crude Oil and Diesel

Crude oil futures were trading near a seven-week high on Tuesday as trade talks between the U.S. and China took place in London, England, with analysts evaluating the possibility that a deal between the world’s two biggest economies could support global economic growth and boost oil demand.

On June 10, West Texas Intermediate July 2025 futures settled on the Nymex at $64.98 per barrel compared with $63.41/bbl on June 3.

Brent futures for August 2025 delivery were trading on the ICE at $66.87/bbl on June 10, up from $65.40/bbl on June 3.

Louisiana Light Sweet crude wholesale spot prices were hovering at $68.74/bbl on June 9, compared with $65.94/bbl on June 2, according to the U.S. Energy Information Administration.

Low-sulfur diesel wholesale spot prices were at $2.15 per gallon at New York Harbor, $2.09/gal on the Gulf Coast and $2.19/gal in Los Angeles on June 9, compared to $2.06/gal, $2.00/gal and $2.15/gal, respectively, on June 2, according to the EIA.

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices

June 11, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner