Paraffinic base oil prices were mostly stable with activity levels ticking up ahead of the Memorial Day weekend on May 26, which marks the start of the summer driving season.

A paraffinic producer’s posted price decrease announcement last week did not trigger an avalanche of other price reductions as many had expected, but market players kept monitoring conditions very closely. Prices for some grades were exposed to downward pressure because of growing availability, but other cuts received support from a tighter supply and demand scenario. Falling crude oil and feedstock prices weighed on all grades. On the naphthenic base oils side, recently announced decreases have now been implemented.

Some corners of the market, particularly those related to Latin American business, were somewhat quiet as many participants were away at the Argus Base Oils Conference taking place in Miami, Florida, on May 20-21.

Crude oil futures had surged last week on news that United States and Chinese officials had reached an agreement to lower their respective tariffs for 90 days while trade negotiations continued. However, oil prices fell early this week following Moody’s downgrade of the U.S. sovereign credit rating and the publication of official data that showed declining growth in China’s industrial output and retail sales, which could lead to reduced oil demand from the world’s top importer. There were also concerns about the health of the U.S. economy. News about a potential Israeli strike on Iran pushed oil prices up on Wednesday.

The barrage of U.S. tariffs has severely dampened the mood among exporters around the world, and 42% of companies now expect their export revenues to decline markedly, Reuters reported, citing a global survey by Allianz Trade published on Tuesday. The credit insurer had surveyed 4,500 exporters in Germany, France, Italy, Spain, Poland, Britain, the U.S., Singapore and China about global trade in March and April, before and after the unsettling tariff announcements by the U.S. on April 2.

One of the economic segments that has been significantly affected by the tariffs is the automotive industry, which has also had a direct impact on base oils and lubricants.

Despite a reduction of Trump’s initial 25% duties on imported vehicles and similar levies on foreign parts and components, automakers have already suffered some of the repercussions from the tariffs, with several manufacturers having to shift production patterns and alter their supply chains, resulting in output disruptions and reduced demand for factory-fill lubricants and greases.

General Motors has halted exports of a small number of American-made vehicles to China as a result of the tariffs as well. The automaker confirmed on Monday that it had stopped sending Chevrolet Tahoe sport utility vehicles to China and has cancelled plans to export other high-end models there, according to media reports. The company also produces some models in China under joint ventures with Chinese manufacturers.

API Group II and Group III producers supply high performance oils to the passenger car motor oil segment, and demand for most grades was heard to have slipped since the beginning of the year, not only because of tariffs, but because of longer drain intervals for newer models and an increase in EV market penetration, amid other factors. The International Energy Agency published a report last week that predicted that more than one in four cars sold worldwide this year would be electric.

Base oil demand for the spring production cycle ahead of the start of the summer driving season was at expected levels, according to some suppliers, although less robust than in previous years. Once most summer lubricant requirements have been met, consumers and suppliers alike were expected to start reinforcing inventories in preparation for the hurricane season. Severe weather along the U.S. Gulf Coast, where many refineries and base oil plants are located, can sometimes bring production to a halt, and participants generally keep extra volumes to cover requirements during potential supply disruptions. The National Oceanic and Atmospheric Administration’s National Hurricane Center defines the Atlantic hurricane season as running from June 1 through November 30.

In its latest “Refining industry risks from 2025 hurricane season” report, the Energy Information Administration noted that the hurricane season will be an active one, with the number of storms exceeding the 1991–2020 historical average of 14 storms, and Colorado State University’s forecast predicting 17 named storms in 2025.

Group II

Group II base stocks had tightened in March and April on the back of a number of plant turnarounds, but the restart of a couple of these units earlier this month was anticipated to bring more product to the market. Demand was also expected to slow down once base stock requirements to cover lubricant production for the summer driving season have been met. This had begun to weigh on pricing, which was already being pressured by falling crude oil and feedstock values.

The changing market conditions were thought to have triggered Chevron’s posted price decrease announcement last week. The company implemented a 35 cents per gallon price decrease on its API Group II base oils, effective May 13.

Chevron was heard to have restarted its plant in Pascagoula, Mississippi, following a turnaround and catalyst change that had begun in April. According to market sources, the producer was likely to see a 10% yield increase with the new catalyst. Chevron’s Richmond, California, plant was also running well after its turnaround last October. Chevron was understood to be rebuilding stocks following the Pascagoula shutdown and will not be offering spot volumes until the end of the month. However, additional product was expected to become available in June, pressuring prices. There was no producer confirmation about the turnaround details since the company does not disclose information about its plant operations.

Motiva started a turnaround its hydrocracker earlier this month, which was anticipated to affect mainly the Group II 220N grade. The three-week maintenance program had been pushed back by a couple of weeks because the catalyst delivery was delayed, but should be completed by the first week of June, according to market sources. The company does not disclose details about its plant operations. Reduced supplies may deter the producer from implementing price revisions, although availability may lengthen in July, sources speculated.

Excel Paralubes has been running its Lake Charles, Louisiana, plant at reduced rates since late last year reportedly due to technical issues related to Group III production at the facility, but contractual obligations continued to be met. However, sources indicated that the producer was abstaining from offering spot volumes this month, and might not be able to supply spot cargoes in June, depending on whether it can build enough stocks ahead of the hurricane season. The production issues were not expected to be resolved until the plant’s scheduled turnaround in October.

Ergon just completed a turnaround at its Group I/Group II base oil unit in Newell, West Virginia, that started on March 31, after perfoming maintenance and implementing several reliability improvements. The producer said that no supply interruptions were expected for current ratable customers as the company had built inventories ahead of the shutdown.

Group I

Supply in the domestic Group I segment seemed to be the tightest of all, as orders were generally steady and production was curtailed on account of turnarounds. There were reports of some pockets of the market having lost strength likely because of the implementation of tariffs, as seemed to be the case in the industrial segment, but the decline was partly offset by snug supply conditions.

There appeared to be increased buying interest for Group I cargoes for export due to strained conditions in other regions as a result of a busy refinery turnaround schedule and plant rationalizations in recent years. Traders were hoping to move U.S. base stocks to Europe, but there was also buying appetite for Group I products from the Middle East, Africa, India and Latin America. However, higher prices in Europe were expected to attract more of the available molecules to that region. At the same time, Group I supplies in the U.S. were also not abundant because of a recent plant turnaround and steady demand.

Shipments of both Group I and Group II grades to Mexico continued regularly, but some transactions were hindered by Mexican importers facing difficulties in obtaining or renewing import licenses. Some buyers were delaying purchases in hopes that export prices would decrease, especially following Chevron’s recent posted price decrease in the U.S.

Ample availability of both Group I and Group II grades in Brazil was placing downward pressure on spot pricing, of the light grades in particular. Some blenders were interested in securing Group II cuts to replace Group I grades as prices of the higher performance oils were more competitive. Argentinian base oils also continued to fill some of the supply gaps in neighboring Brazil, reducing the need for imports from sources with longer lead times.

Group III

Group III prices received support from decreased Group III production at U.S. facilities as Group II output has been ramped up at some units, and volumes shipped from overseas had also declined slightly in the previous months. Spot prices were heard to have climbed by a few cents per gallon week on week for most Group III grades.

At the same time, tariff-related disruptions in automotive manufacturing in the U.S., Mexico and Canada has affected demand for factory-fill lubricants, and many engine oils require Group III base oils in their formulations.

Most imported base oils were expected to be able to enter the U.S. without tariffs because they fall under the energy commodities category and those from Canada are exempt as long as they are USMCA compliant.

Several plant turnarounds in North America, Asia and the Middle East have curtailed global Group III supplies and pushed prices up. However, the restart of production at Petro-Canada’s Group III plant in Mississauga, Canada, earlier this month following a turnaround that began in April should allow for additional product to be reintroduced into the market. The company had built contingency inventory to avoid any supply impacts to customers. The Group II unit at the same location continued to operate during the Group III turnaround.

In South Korea, SK Enmove will be undergoing a partial turnaround at its Group III plant in Ulsan for two months, starting this month, but the shutdown was not expected to have a significant impact on supplies because of uninterrupted production on the facility’s other trains, company sources said.

In the Middle East, ADNOC started a two to three-week turnaround at its Group II/Group III plant in Ruwais, Abu Dhabi, United Arab Emirates, earlier this month.

Bapco was heard to have scheduled a 10-week turnaround at its Group III facilities in Sitra, Bahrain, which was originally scheduled to start in late March or early April, but was reportedly postponed to later this month or early June.

Downstream, blenders were facing resistance to proposed increases that they had hoped would offset the climbing costs of additives, raw materials and components, some of which were driven by higher tariffs. Competition among suppliers thwarted the implementation of price hikes for finished products as suppliers strove to protect market share, particularly in the case of independent lubricant producers competing with major manufacturers.

Naphthenic base oils

A majority of naphthenic base oil producers have implemented a 20 cents/gal price decrease, with effective dates falling between May 9-16. The decrease applied to most grades, with the exception of pale oil 60 and transformer oils, which San Joaquin Refining said would remain unchanged.

Demand for the light pale oils was healthy, particularly for the transformer oils, while the heavier grades were expected to see an uptick in consumption levels from the rubber and tire industry ahead of the summer driving season. The demand increase may be smaller than in previous years because of automotive production disruptions.

Naphthenic producers continued to look for opportunities to ship products to Europe, Latin America and Asia, but competition with European suppliers hampered some of the transactions.

Crude Oil and Diesel

After finishing lower during previous trading sessions, crude oil futures climbed on Wednesday on reports of a potential Israeli attack on Iranian nuclear facilities, fanning concerns that the conflict could disrupt supply availability from the key Middle East region.

On May 20, West Texas Intermediate July 2025 futures settled on the Nymex at $62.03 per barrel, compared to $63.67/bbl on May 13.

Brent futures for July 2025 delivery were trading on the ICE at $66.38/bbl on May 20, from $65.89/bbl on May 13.

Louisiana Light Sweet crude wholesale spot prices were hovering at $66.28/bbl on May 19, compared to $65.52/bbl on May 12, according to the U.S. Energy Information Administration.

Low sulfur diesel wholesale spot prices were at $2.13 per gallon at New York Harbor, $2.05/gal on the Gulf Coast and $2.16/gal in Los Angeles on May 19, compared to $2.11/gal, $2.05/gal and $2.16/gal, respectively, on May 12, according to the EIA.

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

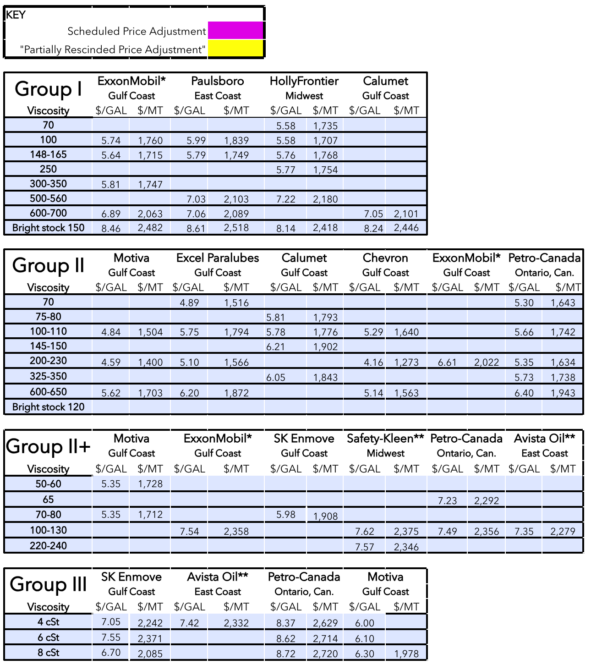

Posted Paraffinic Base Oil Prices

May 21, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner