Just when the Middle East situation was starting to look up and an increasing number of vessels had been able to transit the Strait of Hormuz, Iranian drone attacks on three commercial tankers — including a Qatari LNG carrier — on July 6 and 7 prompted United States retaliatory strikes on Iranian targets. The renewed exchange in hostilities led the U.S. administration to revoke a waiver that allowed the sale of Iranian oil, while Iran vowed to continue controlling traffic in the strait. Oil prices surged following news of the strikes, with West Texas Intermediate climbing to around $72 per barrel from recent levels near $69/bbl. Base oil posted prices were steady, but market participants kept an anxious eye on geopolitical developments as an escalation in hostilities may derail the supply recovery process that so many were counting on. With no fresh base oil cargoes able to leave the Persian Gulf, the global market was sure to see critical shortages of API Group III cuts, as previously available stocks have by and large been depleted. Tight supply conditions also affected the Group I and Group II segments of the market, with suppliers maintaining strict sales controls and allocations.

Following news of the memorandum of understanding signed by U.S. President Donald Trump and Iranian President Masoud Pezeshkian on June 17, there had been an uptick in the number of vessels that had been able to exit the Persian Gulf, and this was seen as an encouraging sign that crude oil and base oil flows would resume soon. Several Middle East crude oil and base oils producers were readying their facilities to restart production after taking their facilities offline given the inability to export products while the strait remained closed.

While there were reports that ADNOC had ramped up Group II and Group III production in Abu Dhabi, hoping that export shipments would resume shortly, another key facility in the Middle East was not expected to resume full output for some time. The Shell Qatar Pearl gas-to-liquids (GTL) plant in Qatar was anticipated to keep at least one train off-line for an extended period after damages sustained during Iranian drone attacks in March, with repairs likely to take several months to complete.

The BAPCO plant in Bahrain had also been damaged during drone strikes and a fire on March 5. It was not clear whether BAPCO had been able to restart Group III production in Bahrain. According to Lloyd’s List Intelligence, vessel movements in Bahrain have resumed, but BAPCO operations remained suspended. The March attack had forced the producer to shut down and declare force majeure on its group operations, although the company confirmed that domestic supplies remained fully secured under pre-established contingency plans. At the time, sources familiar with the plant’s operations had said that Group III production had been unaffected by the fire, but some reports indicated that production had stopped temporarily for damage assessments. Sources said that base oil supply from BAPCO continued under force majeure. An official company report on whether the plant had been restarted was not available by the publishing deadline.

While Group I and Group II production in the U.S. continued largely unaffected by the Iran conflict, some Group I producers did suffer production setbacks as their refineries require Middle Eastern crude oil to run. The Group II segment also tightened because many blenders have resorted to using more Group II base oils as a Group III substitute whenever formulations allowed. As a result, a majority of base oil suppliers had suspended spot offers and focused on meeting contractual obligations.

Some were also concerned that they had entered the hurricane season that runs from June until the end of November along the U.S. Gulf Coast with very low stocks.

Group I and Group II

The lower crude oil prices seen of late had ushered in a slowdown in base oil price adjustments. After the start of the Iran war at the end of February, there had been almost weekly posted price increase announcements as crude oil prices had shot up and supplies had tightened. The steeper base oil prices and other rising production costs prompted blenders to increase lubricant and finished product prices as well. But a number of blenders had been unable to absorb the steep base oil values, and demand in some segments had started to soften. Some buyers have also retreated from the market, waiting for availability to improve, which may help stabilize prices.

U.S. base oil postings climbed between 33% and 73%, depending on the grade, since March, but participants acknowledged that in some cases, prices were not as much an issue as being able to secure supply. There was also concern that participants had entered the hurricane season without extra barrels to cover potential supply disruptions. Domestic base oil suppliers were intent on meeting contract obligations and were forced to suspend spot export offers for several weeks.

While U.S. refiners were partly insulated from the Middle East oil supply crunch stemming from the closure of the Strait of Hormuz because many can run on domestic crudes, experts worried that refineries had drawn on strategic emergency crude stocks, and these were nearing critical levels. Domestic U.S. oil production yields mostly light, sweet crude, and many refiners import heavier Middle Eastern grades to maintain optimal margins for producing heavy fuels like diesel and jet fuel, as well as for base oil production.

Asia is particularly vulnerable to Middle East supply shortages as a majority of refineries — with the exception perhaps of the refinery in Malaysia and a few others — were built to run on Middle East crude slates. Some countries have managed to import crude oil from sources outside the Persian Gulf, but yields for certain base oil grades were affected and crude oil shortages were expected to intensify if flows from the Middle East did not resume soon.

In the U.S., strict sales controls and allocations for contract customers were still in place and spot offers were limited, with some inquiries from Europe and Latin America having to go unfulfilled. At the same time, Group I and Group II availability in Asia has improved, with spot offers from suppliers in Northeast Asia, Southeast Asia and India having surfaced over the last couple of weeks. However, steep freight rates were posing some difficulties in the conclusion of business.

Recent and ongoing scheduled turnarounds have exacerbated the tight supply situation in the U.S. Chevron’s Pascagoula, Mississippi, Group II plant was expected to have started a turnaround in early June which was completed at the end of June. The producer was anticipated to have built inventories to meet contract commitments ahead of the outage, restricting its spot availability. No confirmation was available from Chevron as the producer does not comment on its plant operations.

Within the Group II segment, the light grades were the tightest as some blenders have increased the use of Group II light grades to replace Group III cuts in some applications.

Buying appetite for Group I cuts from Brazil continued to be noted as availability of these cuts has tightened because of a production outage at Brazilian producer Petrobras’ plant earlier this year, coupled with a planned turnaround that started in mid-June. Domestic prices have edged up in tandem with international prices and in response to limited availability.

In Mexico, a key U.S. producer was heard to have encountered some difficulties in supplying bright stock as its production rates had been trimmed. Buyers were still on the lookout for heavy-vis grades and bright stock, but spot supplies were minimal in the U.S. and prices have increased significantly, making it difficult for some blenders to justify purchases. Some buyers preferred to postpone orders until availability levels improved, while others said they hoped that additional offers from Asia might help fill some of the supply gaps, but high freight rates may be a deterrent.

Group III

A gradual increase in transits through the Strait of Hormuz had been encouraging news for Group III base oil market participants who were very concerned about global supply shortages due to the lack of Middle East exports. Group III base oil prices have also skyrocketed in most regions and remained firm in the U.S. A number of Persian Gulf producers were understood to have resumed production of crude oil and refined products, including base oils, in preparation for increased export activities. However, the restart process may come to a halt if the renewed hostilities between the U.S. and Iran that started this week continue or intensify.

Some of the facilities have also suffered damages from drone attacks in March and at least one train at the Shell Qatar Pearl GTL unit was not expected to come back online for several months. The supplier was heard to be seeking additional base oil barrels from other producers to meet some of its contractual obligations in the U.S. and Mexico.

According to sources, ADNOC in Abu Dhabi had started to ramp up base oil production as soon as the memorandum of understanding and a 60-day ceasefire had been announced in late June. The producer had reportedly been running its plant at reduced rates for its downstream production of lubricants and it may take some time for the producer to build inventories and for regular export shipments to resume. The U.S. distributor of ADNOC base oils had continued to partially meet contract commitments because it had been able to ship out a large cargo from Abu Dhabi before the conflict broke out, and it had placed customers on strict allocation. The supplier had also continued to supply product from existing stocks, but these were heard to have been depleted. Even if everything goes as planned and vessels are able to transit the Strait safely, the first shipment of ADNOC material was not expected to reach the U.S. until the end of August.

Meanwhile, Group III suppliers from Asia and Canada were trying to fill the vacuum left by Middle East Group III supplies, but exports from these sources were not deemed sufficient to bridge the gap left by the absence of Middle East base oils, which meet almost 43% of U.S. demand.

Asian plants have increased output rates since refiners have been able to import crude from origins outside the Middle East, but refining yields were not expected to be optimum as most refineries in Asia were built to run on Arab crude slates, with the exception of a few refineries. A key South Korean Group III producer has been able to continue running its plant at high rates, even after the start of the Iran war, as it has diversified its crude sources over the last few years and is able to source crude oil from Southeast Asia and other origins.

Most customers that have contracts with South Korean suppliers continued to receive product, but allocations were in place and spot supplies were largely unavailable. A South Korean Group III supplier has received several inquiries for product from buyers who are not regular customers, but it was unable to supply all the extra requirements and has had to turn business away.

An Indian producer that increased Group III output last year was heard to have sold an export cargo to a trader for shipment to the U.S., but the material did not have approvals required for certain applications.

Additional Group III capacity in the U.S. was not expected to come on-stream until later this year. Chevron has announced that new API Group III+ base oil capacity at its base oils plant in Pascagoula, Mississippi, will come to the market starting in the fourth quarter of 2026. ExxonMobil also expects to bring a major Group III base oil expansion on stream at its Baytown, Texas, complex, but not until 2028. No further details were forthcoming from either producer.

Rerefined capacity is also expected to grow in the U.S. in the coming years. Some blenders have turned to rerefined Group III base oils to meet their requirements given the current lack of virgin Group III base oils, leading to rerefiners being sold out of products as well. However, many suppliers to the automotive industry and OEMs faced supply shortages that were not easy to correct given strict formulation requirements.

Naphthenic Base Oils

Naphthenic base oil prices were steady, but suppliers were monitoring Brent crude oil prices as these have a more direct impact on naphthenic base oils than on paraffinic grades and prices were volatile after renewed hostilities between the U.S. and Iran. Producers had implemented several rounds of increases since the start of the Iran war until May, but no other general adjustments surfaced in recent weeks.

Availability of light naphthenic base oils has tightened, with a supplier heard to be sold out of the pale 40, 60 and 100 grades due to demand from the transformer oil segment, while other sellers also noted tight supply and demand fundamentals for these cuts. Suppliers also mentioned an uptick in consumption of pale oils to replace paraffinic grades in industrial applications given supply tightness, but added that naphthenic grades could not help reduce the impact of paraffinic base oils shortages in automotive applications.

Lubricant Increases

Lubricant manufacturers have implemented price increases to offset rising production costs over the last four months. Some suppliers have been successful at achieving the full intended amounts given concerns of potential shortages due to recent and ongoing supply disruptions. Some manufacturers have faced resistance, particularly as buyers were dealing with cash flow constraints and credit limitations against a backdrop of demand uncertainties in downstream markets.

Lubricant manufacturers have announced three round of increases, with effective dates peppered between April and the end of May. The markups have been driven by the mounting costs of base oils, additives, packaging and transportation over the last two months. Participants underscored that given current uncertainties and the fast pace of market changes—not to mention the escalating production costs–it remained very challenging to plan inventories and make pricing decisions.

Among the manufacturers that have announced various lubricant, grease and finished products increases were TotalEnergies USA, Highline Warren, Martin Lubricants, Omni Specialty Packaging, AOCUSA/Amalie, Calumet, CAM2, Castrol, Shell/SOPUS, PennStar, Chevron, ExxonMobil, Citgo, Phillips 66, Reliance Fluid Technologies, Consolidated Brands/ZXP Technologies and Valvoline. During the first two rounds of increases, suppliers had announced lubricant and grease increases of up to 9% to 35%, depending on the product, with some lubricant increases ranging 48 cents per gallon to $5/gal, and $0.07-0.11/lb for greases. The third round called for increases of up to 26% for most products from one supplier, and markups of $3.00/gal-$3.70/gal for synthetic oils, $2.40/gal-$2.60/gal for other oils, and $0.25/lb-$0.29/lb for greases from the rest of the suppliers.

Some manufacturers have been forced to reduce output given difficulties in transfering the higher production costs down the supply chain, coupled with base oil shortages, particularly of Group III cuts. Several OEM dealers were understood to be bracing for difficulties in fulfilling genuine motor oil demand given the current conditions. Dealers and distributors of a number of major automotive manufacturers received notifications of temporary motor oil supply shortages “due to production and logistics constraints within the global petrochemical supply chain,” one letter read. Even if the Strait of Hormuz were reopened tomorrow, the repercussions of the current supply disruptions were expected to be felt until next year. Some small blenders were considering closing their doors because of financial difficulties and credit limitations to purchase raw materials to keep operations running.

Middle East Base Oil Capacity Shutdowns

According to reports, Shell/Qatar Petroleum has halted production at one train of its Pearl GTL Group II/Group III facility in Qatar after sustaining damage during Iranian aerial attacks on March 19. The plant, which can produce 300,000 tons of Group II base oils and 1,072,000 tons of Group III base oils per year, was expected to remain offline for an extended period, possibly one year or longer as the specially designed equipment at the plant may be difficult to repair and may need to be replaced, according to sources. The explosion at a gas production unit in Ras Laffan Industrial City on June 21 has reportedly not impacted production at the QatarEnergy LNG refinery or the Shell Qatar Pearl unit, although QatarEnergy shut production down as a precautionary measure and has warned customers of a delay in LNG shipments. QatarEnergy supplies feedstocks to the Pearl GTL unit.

Abu Dhabi state oil giant ADNOC shut part of its Ruwais refinery complex in response to a fire that broke out on March 10, following a drone strike. Sources indicated that while the Ruwais West refinery was shut down for inspection and safety reasons at that time, other operations within the massive complex continued at reduced capacity. The trimmed base oil output was utilized for the company’s downstream lubricant production. The Ruwais complex houses a 600,000-tons-per-year Group II and Group III plant. According to reports, ADNOC was expected to ramp up base oil production in the next few days to resume export shipments.

In Bahrain, fire erupted at BAPCO’s refinery in Maameer on March 5 following an Iranian attack, forcing the refinery to declare force majeure on production. BAPCO operates a 400,00-tons-per-year Group III base oil facility in Sitra, within the BAPCO refinery complex. BAPCO originally indicated that base oil production had been unaffected, but it was later heard that the producer had trimmed supply levels. There was no update forthcoming from the producer by the publishing deadline.

Crude Oil

Crude oil futures jumped by more than 3% on Wednesday as renewed hostilities between the U.S. and Iran threatened to derail the recent increase in oil shipments through the Strait of Hormuz. The U.S. strikes were prompted by Iranian attacks on three ships in the Strait of Hormuz, including an LNG carrier and an oil tanker.

- West Texas Intermediate August 2026 futures settled on the Nymex at $70.44 per barrel on July 7, up from $69.50/bbl for front-month futures on June 30.

- Brent September 2026 futures were trading on the ICE at $76.04/bbl on July 8, up from $72.25/bbl for front-month futures on July 1.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $69.10/bbl on July 6 (There was no trading on July 3 due to the U.S. Independence Day holiday). Spot prices had settled at $73.12/bbl on June 29, according to the U.S. Energy Information Administration.

Diesel

Low-sulfur diesel wholesale, July 6 (June 29), EIA

New York Harbor: $3.31 per gallon ($3.32/gal)

Gulf Coast: $3.25/gal ($3.30/gal)

Los Angeles: $3.36/gal ($3.38/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

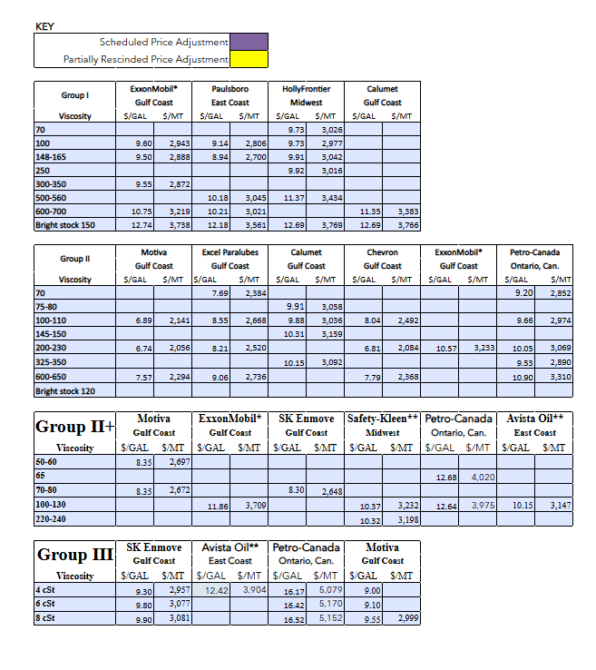

Posted Paraffinic Base Oil Prices July 8, 2026

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner