The war between the United States, Israel and Iran has caused a base oil supply and price shock for the global lubricants industry, causing prices to skyrocket and creating widespread shortages.

Industry insiders and observers agree the crisis will last — and possibly worsen — until the Strait of Hormuz reopens to commercial shipping. Many warn, though, that disruptions could last well beyond the end of the conflict, especially for supply of API Group III base stocks.

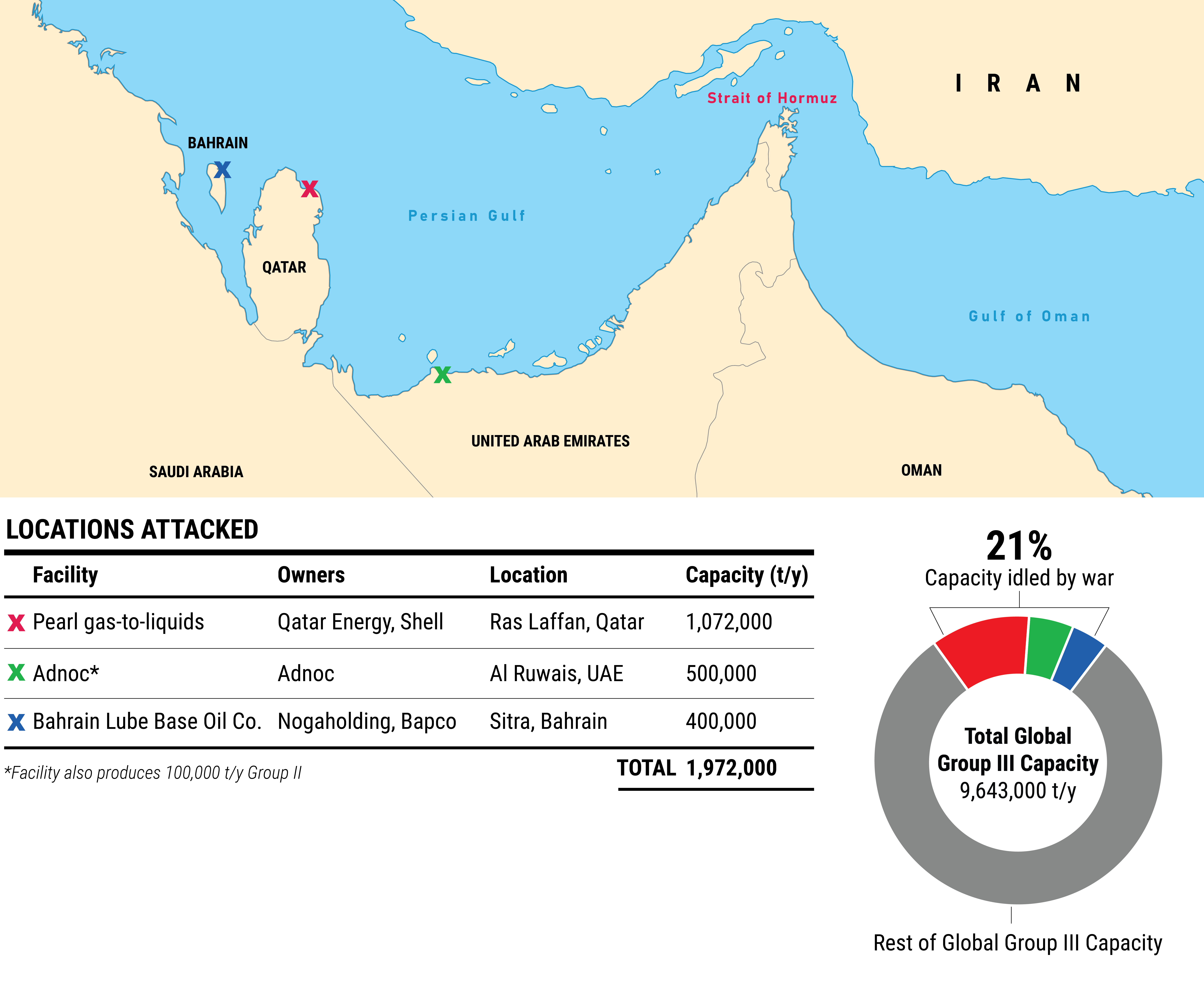

Strait Line to Disruption

The strait’s unprecedented closing was the trigger for the crisis. The narrow waterway, which provides an outlet from the Persian or Middle East Gulf to the Sea of Oman and the Arabian Sea, is used by ships carrying a fifth of the world’s oil and gas. The gulf is also home to three refineries — the Pearl gas-to-liquid plant in Ras Laffan, Qatar, Adnoc’s plant in Al Ruwais, United Arab Emirates, and Bahrain Lube Base Oil Co. in Sitra, Bahrain — accounting for 21% of global Group III production capacity (see Figure 1). Exports from those facilities traverse the strait on their way to markets around the world, as do Iranian Group I exports to markets such as India and the United Arab Emirates.

Shipping traffic through the strait halted shortly after the U.S. and Israel began bombing Iran on Feb. 28, and within a few days Iran’s Islamic Revolutionary Guard Corps had the passageway blockaded through a combination of mines and threat of drone attacks. Markets reacted quickly. Prices on London’s ICE exchange for dated deliveries of Brent crude, which had hovered between U.S. $60 and $70 per barrel for almost all of the previous year, jumped above $93/bbl within 10 days and by early April brushed $110/bbl.

Figure 1. Group III Capacity Knocked Out By War

Prices for mineral base oils — which usually track crude costs — shot up, too, and not just for Group III. Between the last week of February and mid-April, spot pan-Asian and -European rates for Group I 150 solvent neutral more than doubled, from the upper- and low-$600s per metric ton, respectively, to around $1,500/t and $1,700/t. Rates for Group II 150 neutral rose similar amounts, from around $750/t to near $1,600/t in Asia and from $840/t to $1,880/t in Europe. Group III 4 centiStoke went from around $1,125/t to $1,900/t in Asia and from $1,600/t to $2,350/t in Europe. Base oil posted prices in the U.S. and Canada were higher to begin but also increased drastically: from $1,623/t to $2,240/t for the market’s lowest-priced Group I SN150; from $1,348/t to $1,799/t for the lowest Group II 110N; and from $2,242/t to $2,592/t for the lowest Group III 4 cSt.

Despite the run-up in prices, availabilities shrank. Spot offerings largely disappeared, and some suppliers reduced amounts available to regular and contracted customers. An auction dynamic developed for oils that were offered for spot sale, with sellers able to field bids from desperate buyers.

“I don’t think it’s so much an outright shortage as an anticipation of a shortage,” Vincent Gillooley, senior vice president of Chemlube, an international base oil trader in Harrison, New York, said in mid-April. “A lot of buyers are sounding desperate. Prices have basically doubled across the board, but in a lot of discussions going on it’s not even a matter of price. Buyers are being told, ‘Come back to [traders and sellers] by tomorrow’ because if they come back the day after tomorrow it’s too late.”

Unsurprisingly, the worst impacts fell on blenders in the Middle East Gulf. As this issue went to press, the war was seven weeks old, and the strait had been mostly blocked for that period. Most of the base stocks and additives used in the region are delivered by sea, meaning stocks had not been replenished during that time.

“We’re not seeing widespread shutdowns of blending plants yet, but we are definitely seeing operational stresses,” Bluechem Group Global Director for Lubricants and Base Oils Bhupinder Singh, who also leads a LinkedIn group, Lubricants Specialists, organizing webinars about the crisis, said in an April 20 interview. “Without deliveries of base oils or additives, blenders are running low, and if shipping does not open back up in the next several weeks, you will see companies halt production.”

The most immediate reason for the run-up in base oil prices was the increase in crude and feedstock costs. The loss of Group III from the Middle East Gulf also contributed. When shipments from those plants halted, customers looked for alternative sources, setting off a scramble for remaining availability. The Group III shortage in turn led to greater demand for Group II as blenders unable to procure Group III bought the latter grade instead.

Feedstock Diverted to Fuels

In addition, the constraints on crude oil availability reduced base oil production. As quickly as it became clear that crude supply was being squeezed enough to affect fuels production, refiners — in some cases with urging from their governments — began optimizing production of diesel, gasoline, jet fuel and other fuels by redirecting feedstocks from base oils production. Observers said the phenomena was strongest in Asia, which depends heavily on Middle East crudes.

“The redirection of feedstock away from base oils is a significant factor,” said Harry “Ernie” Henderson, president of K&E Petroleum Consulting in Oklahoma City, United States. “Combine that with the reduction in Group III supply and the increase in Group II demand and that’s how you end up in this situation.”

There was near universal agreement that the crisis would continue as long as the strait remained closed and that it could worsen. Some oil industry analysts warned that crude prices could rise significantly higher, particularly after releases from strategic petroleum reserves get sopped up. In late April there were reports of U.S. President Donald Trump saying privately that the strait could remain closed for months.

But analysts and insiders also agreed the lubricant industry’s problems will not resolve as soon as the strait reopens. Factors related to crude availability could begin to resolve soon after, but sources noted that base oil supply chains are lengthy.

“Crude oil shipments that have been held up can take weeks to reach refineries and base oil plants,” said Mattia Adani, president of Milan-based lubricant and specialty chemical producer Nowal Chimica, who is also president of the Brussels-based Union of the European Lubricants Industry. “Then it can take weeks again for base oil cargoes to reach market. You also need to consider that inventories have been depleted — both at the distributor level and at blending plants.

“All that said, I fear our industry, like many others, will face volatility and potential instability for several months — at least until the end of the year — even if the situation is resolved in the coming days or weeks.”

Repairing Damage

Group III supply from the Middle East Gulf will apparently be disrupted beyond the reopening of the strait. All three plants were attacked by Iran, and damage will need to be repaired. Shell, joint venture partner with Qatar Energy in the Pearl facility, announced that one of its production trains was damaged and could take a year to repair. The facility consists of two production trains, each of which converts natural gas into 140,000 barrel-per-day-equivalents of refined products. Base oil capacity of 1,072,000 metric tons per year is divided equally into each of the trains. Presumably the undamaged train could resume production when the conflict ends.

Bapco, which operates the Sitra refinery and base oil plant, announced March 9 that its facility had been struck, that operations were halted and that it was declaring force majeure for supply of products made there. As this issue went to press the company had not discussed damage or a timeline for reopening. Observers speculated that repairs are needed and could take six months.

The day after Bapco’s announcement, Adnoc said a drone strike at one of its refineries, later confirmed to be the one in Al Ruwais, was struck by a drone that caused a fire. The company closed the refinery but by April 23 had offered no information about damage nor a timeline for reopening.

In sum, the outlook remained quite hazy, but the industry faced the prospect of losing 10% or more of global Group III production capacity for six to 12 months or more. Opinions varied of how much disruption this would cause. The U.S.-based Independent Lubricant Manufacturers Association warned of serious shortages that would leave some passenger car engine oil producers unable to adhere to formulas certified as meeting current performance standards. Meeting such standards increasingly requires Group III base stocks. Certifications that products meet performance specs are tied to particular formulas, and rules limit adjustments to base oil content.

On March 13 ILMA asked the American Petroleum Institute and General Motors to allow marketers to replace base stocks while continuing to claim compliance with API and dexos specs, respectively. Normally new formulas would need to undergo new testing — which is extensive and expensive — if more than a minimal amount of formulated base stocks are replaced.

API granted the request, stating that marketers seeking a variance to alter formulas would need to disclose the base oil replacement and document that the change would not adversely affect performance. If accepted by API, marketers would then have 180 days to complete testing and submit results proving performance of the revised formula. GM declined ILMA’s request.

The Brussels-based Union of the European Lubricant Industry, or UEIL, which plays a role similar to ILMA’s in Europe, had requested no such action as this issue went to press. “I agree with ILMA that disruptions will likely persist for months, even if the strait reopens,” Adani said, but he added that UEIL did not consider general relief to be necessary. He noted that the ATIEL Code of Practice, which establishes European rules involving automotive engine oil performance specs, provides for provisional licensing.

“It is done on a case-by-case process in which individual blenders must file for exemptions, he said. “As of now, no company has submitted such a request in Europe.”

Henderson contended that the global market had unused Group III capacity before the war, which should provide some buffer for capacity knocked out by the war.

“There is a global overhang of Group III in terms of capacity,” he said. “That includes new Group III in markets such as China, some of which could get redirected to replace what’s being lost from the Middle East. It may take time for trade patterns to adjust, but things like that could reduce the brunt of the impact.”

There was no question lube blenders in April were confronted with base oil price and supply shocks unprecedented in their size and scope. Middle East Gulf companies upstream of the strait were looking for alternative means of procuring raw materials — for example having shipments discharged at the UAE port of Fujairah or Omani ports, which are in the Gulf of Oman. But cargoes would then need to be trucked to blend plants, which was deemed untenable.

“People are looking at such things because they are searching for possible solutions, but it is not a practical solution for this crisis,” Singh said.

Lube companies there and elsewhere worry they will be coping with the situation for a large portion of the year.

Tim Sullivan is Executive Editor of Lubes’n’Greases. Contact him at Tim@LubesnGreases.com