Russia’s 2022 invasion of Ukraine and the sanctions that followed have caused tremendous upheaval to humans and economies — among them remaking one of the world’s biggest base oil and lubricant industries.

Once a large exporter of base oils to Europe, those exports have now largely ceased — or entered the shadows. Previously it was largely supplied by Western lubricant and lube additive companies, but domestic and Asian suppliers have taken much of that business. Across the spectrum, trade routes and supply chains have been disrupted, making operations more expensive and haphazard. Analysts say the changes underscore both the resilience of lubricants demand and the structural limits imposed by sanctions, high borrowing costs and restricted access to global markets.

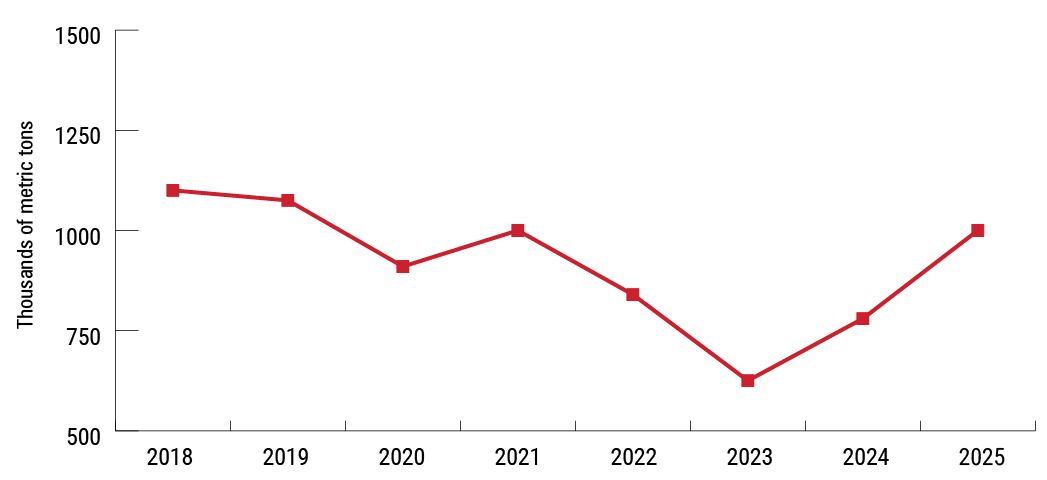

Base Oil Exports

Before the war, Russia exported about 1 million metric tons of base oils annually. Those volumes fell sharply after the invasion as sanctions tightened and payment and shipping channels narrowed.

Exports dropped to around 840,000 tons in 2022 and declined further to about 625,000 tons in 2023. In 2024, shipments recovered to roughly 780,000 tons, and in 2025 they returned to about 1 million tons — an increase of around 28% year on year, according to estimates shared by Berlin-based trader DYM Resources, based largely on railway and river shipment data. (See Figure 1.)

Figure 1. Russian Base Oil Exports During War

Source: DYM Resources

DYM Managing Director Denis Varaksin said the rebound reflects the industry’s ability to rebuild export logistics.

“Exports in 2025 increased significantly, mainly due to improved logistics and payment routes,” he said. “Rosneft, Gazprom Neft and Lukoil were able to adapt and continue shipping through different trading structures.”

Some analysts argue that tighter U.S. sanctions on Rosneft and Lukoil, combined with Ukrainian drone attacks — including a couple of strikes in September and October on Bashneft’s refinery complex in Ufa, a major API Group I base oil producer — interrupted export flows through Black Sea and Baltic Sea routes. Varaksin said he does not see this as the decisive factor.

“This export growth could have been stronger,” he said. “We continue to see Russian base oils arriving in Turkey, where resellers still offer significant volumes. There may be cases where shipowners or refiners avoid visibility as sanctions tighten, but product flows continue.”

Regarding the Baltic and Black Sea export routes, Varaksin said bulk tanker shipments may have slowed or in some cases become less visible, while container deliveries continued. Maritime flows have grown increasingly opaque, particularly as port infrastructure has come under repeated attack. In 2025 and early 2026, Ukraine’s armed forces intensified drone attacks on the Black Sea ports of Novorossiysk and Tuapse — long central to Russia’s crude and refined product exports — disrupting operations and adding uncertainty to loading schedules. Kaliningrad, Russia’s Baltic Sea enclave, serves as a key hub. Lukoil operates a base oil terminal there and remains the only major oil company handling such volumes at the site.

With limited transparency in maritime trade, railway shipment data remains the most consistent indicator of Russian base oil supply and movement. Varaksin said those figures show exports increased overall in 2025 as Russia established more stable trade channels, although a strong ruble, drone attacks and weak export prices constrained further growth.

Western sanctions are often perceived as a full embargo on Russian oil, but the policy framework was designed to limit the revenue Moscow uses to finance its military operations and sustain the war effort in Ukraine, rather than eliminate exports altogether. The price-cap mechanism introduced in late 2022 allowed Russian crude and refined products to remain on global markets while restricting prices at which they could be sold using Western shipping, insurance and financial services.

Additional U.S. measures targeting specific oil companies have increased pressure, but the overall system has remained intact. Russia responded by expanding alternative payment mechanisms and building a network of trading intermediaries.

Urals crude trades at a discount, yet oil remains Russia’s primary revenue source. A growing “shadow fleet” and new routing structures have enabled shipments to continue — mainly to China, India, the United Arab Emirates and Turkey.

Russian base oils are not shipped directly to the European Union, Varaksin said. Instead, exports are directed to markets where payments and logistics remain workable, including Turkey, India, the United Arab Emirates, Israel and Egypt.

Intermediaries and third-country processors then play a role in reexporting or blending volumes that eventually enter European markets.

The Union of the European Lubricant Industry recently raised concerns in an open letter to the European Commission that sanctioned Russian products may be entering the EU via blending and reexport operations in neighboring markets. UEIL President Mattia Adani warned that such trade could harm the competitiveness and stability of the European lubricants industry.

Domestic Lubes Market

Inside Russia, the lubricants sector has proven more resilient than many other industrial segments. Anatoly Filatkin, head of Moscow-based automotive consultancy Autostat, said the market entered a new equilibrium in 2024 after two years of disruption.

“The main trends remained largely unchanged from 2024 into 2025,” Filatkin said in October at the CarXL 2025 automotive forum in Moscow. “Competition intensified, sellers still outnumber buyers and demand softened slightly.”

Before 2022, the market was dominated by foreign brands and aligned with global specifications and approvals. That structure collapsed after the invasion, leading to plant shutdowns, component shortages and a reshaped vehicle fleet.

“Supply chains were rebuilt, and competition increased as new brands entered and existing ones expanded,” Filatkin said. “Demand recovered in 2024 but eased slightly again in 2025.”

Russia’s finished lubricants market — around 1.6 million tons annually — has historically been stable, declining only modestly even during the COVID-19 downturn. Autostat forecasts a decline of roughly 2.7% in 2025 followed by modest growth of about 1% in 2026.

Engine oils for passenger car and light commercial vehicles remain the strongest segment, with volumes affected largely by drain intervals. Heavy-duty and industrial lubricants face weaker demand tied to slower industrial activity.

With Western additive suppliers exiting the market, Russian producers rebuilt supply chains around China and intermediaries in the Middle East. These channels now play a central role in the production of finished lubricants.

Industry consultant Pavel Kartashov said the shift has significantly altered pricing and procurement.

“Chinese products are available, but they are not cheap,” Kartashov said. “They often require full prepayment in hard currency and long delivery times. That raises costs across the market.”

According to Kartashov, the market now operates under tighter constraints. Procurement is more complex, financing costs are higher and purchasing decisions are increasingly driven by availability rather than brand or specification.

“Customers have fewer options and often buy what is available,” he said. “Supply routes are longer, costs are higher and decisions are made faster because alternatives are limited.”

The departure of some Western finished lubricant suppliers opened space for domestic producers and private labels. Russian oil companies expanded blending capacity, while smaller manufacturers and contract blenders launched new brands targeting retail and fleet markets.

The result is a more fragmented competitive landscape. Sellers have multiplied, purchasing power has weakened and premium segments once dominated by global brands remain only partially filled.

Lubricant additives and specialty components remain difficult to source. Producers depend heavily on imports through Asian channels, often requiring hard-currency prepayment and extended delivery timelines. Kartashov said the shift has changed the way companies operate.

“The market functions differently now,” he said. “There are fewer formal processes, fewer tenders and more decisions driven by availability and logistics. It reflects a business environment shaped by war and sanctions.”

In an effort to hamper Russia’s war machine, Ukraine has repeatedly launched drone strikes on the country’s oil infrastructure, including refineries. At least six of the attacked refineries include base oil plants and lube blending facilities. (See Figure 2.)

Figure 2. Attacks on Russian Base Oil Refineries

Oleg Tsvetkov of the Topchiev Institute of Petrochemical Synthesis confirmed that Novokuibyshevsk was still producing additives and lubricants as of late last year, and he described the broader market as relatively stable but trending slightly downward.

Sanctions have reduced export opportunities and complicated operations in Europe, where marketing, testing and product approvals have become increasingly difficult for Russian brands, according to Kartashov. Following renewed U.S. sanctions, Lukoil pulled out of the European market altogether through a broad divestment of international assets.

He said the loss of Europe represents a structural shift.

“Without approvals, testing and marketing, it is very difficult for Russian lubricant brands to operate there,” he said. “In the medium term, many will struggle to return.”

Russian lubricant suppliers are increasingly targeting Asia and the Middle East, where political and commercial barriers are lower.

“There is a clear drive to build positions in Arabic and Asian markets,” Kartashov said. “These countries may buy oils and other products more freely, and companies see an opportunity to gain share where restrictions are less severe.”

But transparency remains limited. Reliable data from these regions is scarce, and companies disclose little about performance.

A Market in Transition

Most aspects of Russia’s base oil and lubricant industry have been significantly impacted by sanctions against the invasion of Ukraine. Channels for sales into Europe — historical foci for base oils and lubes — have largely been eliminated. If such trade is going on now it is clandestine, indirect and likely less profitable. Integration with global specifications and approvals has weakened, reinforcing a shift in the industry’s export trade toward non-Western markets.

The lubricant market within Russia has undergone major shake-ups. Departure of some Western companies created opportunity for local suppliers, which indeed have expanded, but the market faces structural challenges: high borrowing costs, sanctions and banking restrictions, infrastructure risks and limited access to advanced additives and technologies.

“The industry is still operating and still adapting,” Kartashov said. “But this is a different market from before 2022 — more complex, more expensive and more dependent on alternative partners.”

Russia’s lubricants sector has shown an ability to adapt under pressure. Whether it can sustain that adaptability — and remain competitive without access to Western technology, capital and markets — will determine its direction in the years ahead.

Boris Kamchev is a reporter with Lubes’n’Greases. Contact him at Boris@LubesnGreases.com