Freezing temperatures and heavy snow blanketed large swaths of the United States and Canada this week, knocking out power, disrupting transportation and causing several fatalities. A number of refineries were on high alert and some halted operations temporarily. Freeze-offs curtailed roughly five million barrels of crude oil production, primarily in the Permian basin, and crude exports were halted over the weekend because of port closures along the U.S. Gulf Coast. However, ports reopened on Monday. Most participants in the Houston, Texas, area reported little impact on operations and logistics. Producers had prepared for the storm, with minimal impact to base oil production observed at most refineries, but there were some small issues reported at a few blending plants which are more vulnerable to extreme weather conditions.

Given the recent history of freezing temperatures that have affected many of the areas where refineries are located, most facilities have been “winterized” and have plans and procedures in place to protect employees and structures during such extreme weather events. However, an extended power outage could cause output disruptions even though many units are equipped with backup generators, industry sources noted.

One of the refineries that participants were keeping an eye on because of its location in the path of the storm was Paulsboro’s Group I plant in Paulsboro, New Jersey. The company indicated that their lubes business remained unaffected by the severe weather for the time being, but the producer plans to focus on domestic transactions and will temporarily halt fresh export discussions. “As the refinery works through the recent impacts of the weather event, we will suspend quoting export barrels to ensure we meet all our domestic obligations in the near term,” a company source explained.

Calumet operates two plants in Louisiana, a state that was also impacted by the storm. However, neither of Calumet’s units had been affected. “We were able to safely navigate the severe weather without any disruptions,” a company source reported.

HF Sinclair/HollyFrontier’s plant in Tulsa, Oklahoma, was also identified as a likely candidate to feel the impact of the storm. However, its status could not be confirmed by the time of publication.

The winter storm also pushed crude oil prices higher, with futures rising by about 3% on Tuesday, as

U.S. oil producers lost up to 2 million barrels per day, or roughly 15% of national production, over the weekend, according to analysts. The storm also strained energy infrastructure and power grids and was expected to bring a significant drawdown in crude inventories.

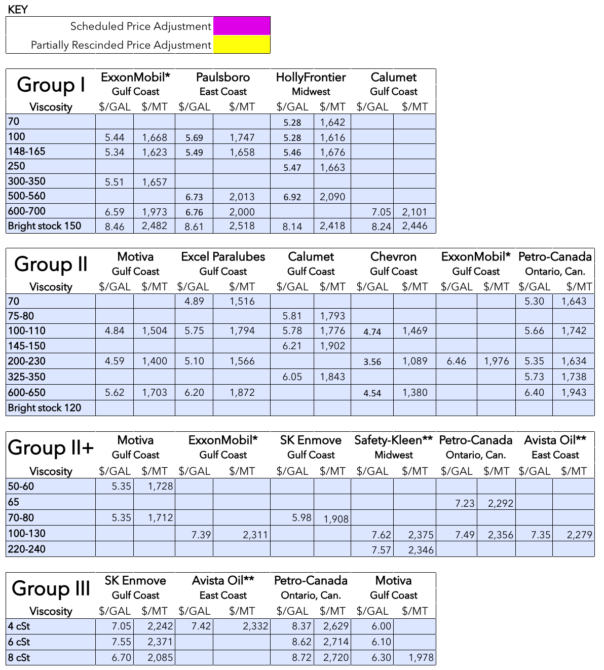

Group I

As has been the case over the last few weeks, API Group I heavy-grade prices remained under downward pressure because of ample inventories and lukewarm demand, but there has been little price movement this week as trading was muted. Economic uncertainties and tariff turmoil have affected industrial activity and demand for industrial oils and metalworking fluids has weakened.

The U.S. domestic market mirrored the situation in other regions as well, with requirements described as lackluster in Europe and Asia, although buying interest for the light grade and bright stock appeared to be stronger than for the heavier cuts.

Domestic Group I suppliers had so far focused their attention on exports to South America, with Brazil being one of the strongest contenders for U.S. barrels. As previously reported, Brazilian producer Petrobras’ base oils plant had suffered an unexpected and extended shutdown in October and the supplier had been unable to meet all of its domestic requirements, which drove buyers to seek Group I and Group II imports. However, Petrobras’ ability to supply Group I contractual volumes appeared to have improved, although the producer was still unable to offer spot cargoes. While bright stock was still very much sought-after, prices have come under pressure because of substantial import quantities.

U.S base oils also continue to move regularly into Mexico – the largest importer of U.S. base oils. Suppliers were facing competition from U.S. rerefined grades, as well as Asian material, according to sources. Some buyers were hesitant about committing to large quantities as prospects in lubricant applications were still dim.

A 5,000-metric ton cargo was heard to have been shipped from Houston, Texas, to Rio de Janeiro, Brazil, on January 15. A 2,000-metric-ton parcel was mentioned for possible shipment from the U.S. East Coast to Antwerp-Rotterdam-Amsterdam (ARA), or Gibraltar, or Egypt between Feb. 1-5, although it could not be confirmed whether it involved only Group I base oils.

Group II

Group II spot prices were also on tenuous ground because of plentiful supplies and demand that was slow to emerge. However, while some suppliers appeared to be amiable to granting price concessions, a number of them held offers firm. The lighter grades were tighter and at least one supplier was heard to have no spot supplies of the light grade to offer for spot export business, which provided more support to pricing.

While the Group II segment was generally perceived as being oversupplied, market players commented that the situation was slightly more manageable than at the same time last year, when inventories were much larger. This was partly attributed to the fact that suppliers had been able to ship large volumes of base oils into different export destinations during the fourth quarter of 2025, although some countries such as India had taken fewer cargoes than in the previous years. However, the Group II had also reached the end of the year with a tighter supply and demand ratio because of the turnaround of a Group II plant in the last quarter.

U.S. producers were competing for business with rerefiners in Mexico, although the additional supplies helped meet demand for the light grades, which were in more limited supply. Rerefiners expected tightening supplies as an upcoming maintenance program at a rerefinery in the first part of 2026 was anticipated to limit availability. The rerefiner was heard to be building inventories to cover obligations during the outage.

Nevertheless, demand in Mexico was still sluggish, with economic instability dampening business as blenders were unsure of lubricant demand levels over the next few weeks. Most importers have been able to renew import licenses, although there were some participants that were still in the process of securing theirs.

Group III

Spot prices for the Group III 4 centiStoke have edged up on more limited availability, while downward pressure on the 6 cSt and 8 cSt persisted. There were fewer extra volumes of Asian material available in the U.S. market, likely because suppliers had been able to place most of their products over the last couple of weeks.

Given the length of 6 cSt and 8 cSt grades, it was heard that a supplier was only selling the 4 cSt in conjunction with 6 cSt and 8 cSt cuts. Prices for the heavier grades remain under pressure and some offers were heard at around $2.60-2.80 per gallon, but failed to elicit increased buying interest.

Domestic production of Group III grades and rerefining output were not impacting current spot prices directly as producers were using their Group III base oils as correction fluids or for internal lubricant production. However, a gradual tightening of global supplies of Group III grades has been observed, and this could ultimately impact U.S. prices in the coming weeks.

In related industry news, ExxonMobil announced that the company had begun construction on a major expansion of its Group III base oil capacity at its Baytown complex in Texas. The project is expected to add about 8,000 barrels per day of Group III capacity. (For further details, see “ExxonMobil Breaks Ground on Group III Unit at Baytown” in this week’s issue of Lube Report).

Naphthenics

Prices for naphthenic oils have been reported as generally steady. Steeper crude oil prices along with a fairly balanced supply and demand scenario offered support. Despite increased availability of the heavy-viscosity grades because of weaker consumption from the rubber and tire segment, the market had entered the last quarter of the year on snug conditions given an extended turnaround and upgrade at Ergon’s Vicksburg, Mississippi, plant, and this situation continued into the first month of the year. Requirements from the rubber and tire segment were anticipated to creep up in the next few weeks as suppliers prepare stocks for the spring season. There has also been a small uptick in demand for the light pale oils from the transformer oil segment.

Additionally, San Joaquin Refining started to build inventories ahead of a three-week turnaround scheduled for late January at its refinery in Bakersfield, California. The producer plans to continue supplying its customers during the outage and market supplies were generally expected to tighten.

Calumet will also likely begin building inventories soon as the producer plans to have a turnaround at its naphthenic plant in Princeton, Louisiana, in the first half of April.

Crude

Crude oil futures climbed to four-month highs, propelled by a weak dollar and the effects of a powerful winter storm in the U.S. Further price support came from expectations that OPEC+ would maintain a pause in output hikes until at least April.

- West Texas Intermediate front-month futures settled on the Nymex at $62.39 per barrel on Jan. 27, up from $60.36/bbl for front-month futures on Jan. 20.

- Brent futures for March 2026 delivery were trading on the ICE at $67.96/bbl on Jan. 28, up from $64.01/bbl for front-month futures on Jan. 21.

- Louisiana Light Sweet crude wholesale spot prices were hovering at $61.69/bbl on Jan. 26. Spot prices had settled at $61.40/bbl on Jan. 16, according to the U.S. Energy Information Administration. (There was no trading on Jan. 19 due to the Martin Luther King Jr. holiday).

Diesel

Low-sulfur diesel wholesale, Jan. 26 (Jan. 16), EIA

New York Harbor: $2.32 per gallon ($2.26/gal)

Gulf Coast: $2.18/gal ($2.11/gal)

Los Angeles: $2.23/gal ($2.21/gal)

Gabriela Wheeler can be reached directly at gabriela@LubesnGreases.com

LNG Publishing Co. Inc./Lubes’n’Greases shall not be liable for commercial decisions based on the contents of this report.

Posted Paraffinic Base Oil Prices: January 28, 2025

(Prices are FOB basis, in U.S. dollars per gallon and U.S. dollars per metric ton).

Archived base oil price reports can be found through this link: https://www.lubesngreases.com/category/base-stocks/other/base-oil-pricing-report/

Historic and current base oil pricing data are available for purchase in Excel format.

*ExxonMobil prices obtained indirectly.

**Rerefiner