United States refiners produced an anemic 27.2 million barrels of virgin mineral base oil in the first six months of this year, according to recent statistics, 7% less than the same period last year and the third-worst first half output in the past 20 years.

Base oil production in the country still has not returned to pre-COVID-19 levels, having trended downward by about 8% since the pandemic. But the market also remains in significant flux in other ways, too. U.S. base oil exports and imports have both been rising for years and continue to do so. Amidst that reconfiguration, domestic plant utilization rates have been falling. Two API Group III projects now underway could jolt at least some of these trends, putting a dent in imports while raising the amount of domestic output consumed at home.

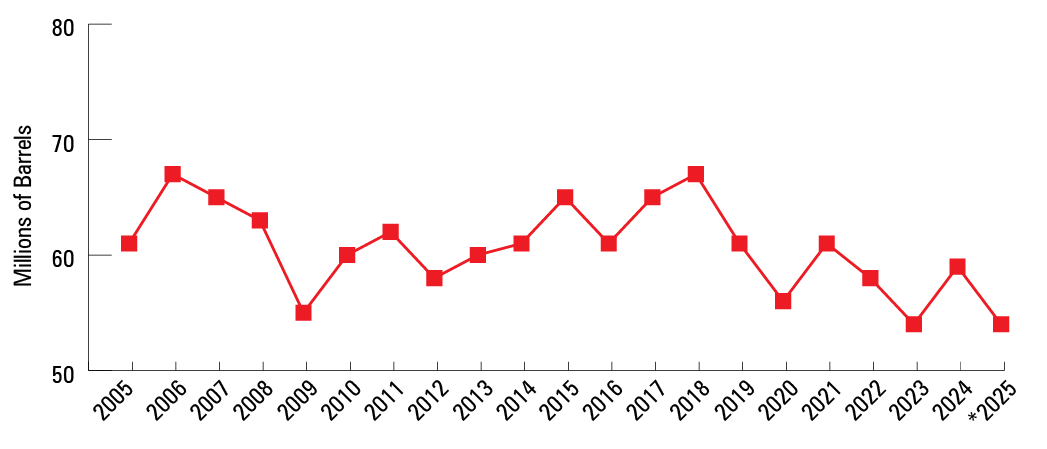

The U.S. and China are by far the world’s two biggest base oil producers. For the past two decades, U.S. output has varied from year to year but trended relatively level. From 2005-2009, production averaged 62.3 million barrels per year, and the annual average for the next two five-year periods was 60 million barrels (2010-2014) and 63.8 million barrels (2015-2019). For 2020-2024, however, the average dropped to 57.6 million barrels.

There is no sign of a rebound in 2025. According to data from the U.S. Energy Information Administration, American refiners made 27.2 million barrels from January through June. That was down from 29.2 million barrels in the same period of 2024 and was lower than any year in the past 20 save 2023 and 2009, during the Great Recession. EIA’s base oil production data only goes back to 2005.

As seen in Figure 1, if output for the second half of this year were to match the first six months, this year would fall to the very end of the line for the past 21 years of base oil productivity — slightly behind 2009 and 2023.

Figure 1. U.S. Virgin Base Oil Production

Source: U.S. Energy Information Administration

Notes: * Projected based on first six months

Amy Claxton, CEO of My Energy consulting firm of Hummelstown, Pennsylvania, cautioned against reading too much into data for this year’s first half. “Yes, January to June was down, but July and August were up and robust. I don’t like six-month snapshots.” She added that crude oil refining usually runs low during the first quarter, which would contribute to lower output of base oil feedstock.

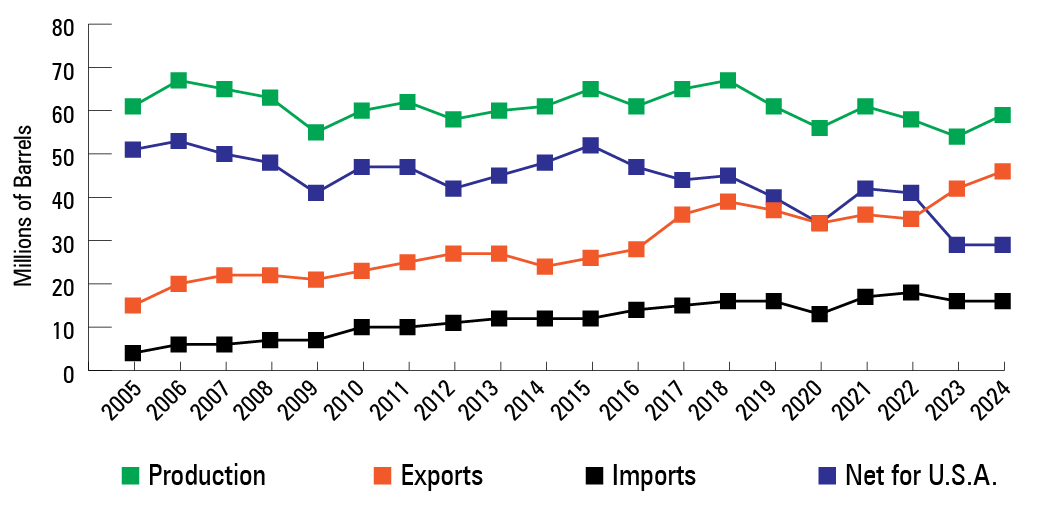

The market has undergone other big shifts the past two decades. Net virgin base oil consumption — as calculated by domestic production minus exports, plus imports but disregarding changes in inventory — fell more sharply than production since the start of the pandemic. (Fig. 2) After five-year averages of 48.5 million barrels, 45.8 million barrels and 45.3 million barrels from 2005 through 2019, net consumption averaged just 35 million barrels from 2020-2024.

Figure 2. U.S. Virgin Base Oil Production, Exports and Imports

Source: U.S. Energy Information Administration

Domestic base oil demand is clearly decreasing, said Geeta Agashe, of Geeta Agashe & Associates in Cedar Grove, New Jersey, citing factors such as extensions to drain intervals for passenger car motor oils and increasing sales of electric vehicles powered solely by battery, which do not use engine oil.

“There has been significant demand destruction, primarily in the PCMO segment,” she said. Claxton said virgin mineral base oils have also been pressured by rerefined base oils, production of which has risen in the U.S. EIA’s data does not include rerefined base oils.

While U.S. virgin base oil production has shrunk, it has decreased less than domestic consumption because producers were able to sell increased amounts into foreign markets. Exports rose steadily, tripling from 2005-2024. The biggest portion of oils sold abroad are Group II oils, the category that the U.S. makes the most of.

Mexico is by far the largest destination, receiving 19.9 million barrels last year, or 43% of total exports. Next came Brazil, Belgium — the main European Union entrance for U.S. base oils — and Canada, with 4.1 million, 3.9 million and 3.6 million barrels, respectively. Exports to Canada rose 58% since 2005, while those to Mexico more than quadrupled and those to Brazil and Belgium jumped 10-fold.

Claxton said U.S. refiners have exported because they could not sell all their oil domestically. “As massive Group II plant expansions were undertaken in North America, the envisioned [reduction] in Group I output didn’t occur. This has required massive Group II exportation to Mexico and other Latin American countries, sometimes at hefty discounts, leading to lower margins for North American Group II refiners.”

Imports also grew steadily throughout the period, due to growing demand for Group III base oils. As Claxton noted, rising PCMO performance demands have increased requirements for base stocks with high viscosity index and low NOACK volatility — meaning Group III and Group III+. U.S. investment in Group III capacity has not kept up with that demand. Chevron’s base oil plant in Richmond, California, is the only large source of virgin Group III, currently configured to make 2,500 barrels per day of that grade, or 912,000 barrels per year. Avista Oil has capacity to make 1,500 b/d of Group III at its Peachtree, Georgia, rerefinery, and a few other facilities can make small amounts.

So the U.S. imports mostly Group III oils. A combined 15.3 million barrels of last year’s imports came from South Korea, Canada, Qatar, the United Arab Emirates, Bahrain and Indonesia, all Group III exporters. That amounted to 95% of the year’s total base oil imports.

“We need Group III and Group III+ molecules to formulate low-viscosity PCMOs that meet the NOACK limits, so we are importing those from the Middle East and Southeast Asia,” Agashe said.

Two projects are likely to eat into U.S. demand for Group III imports. In March of this year, Chevron said it will upgrade its Pascagoula, Mississippi, plant to begin commercial production of Group III+ oils by the fourth quarter of 2026. Chevron did not disclose the capacity of that project, but ExxonMobil said in August that it aims to add 8,000 b/d of Group III capacity to its Baytown, Texas, plant by 2028. Canadian start-up Cerilon is trying to develop a North Dakota gas-to-liquids plant that would make 5,800 b/d of Group III+ base oils, but it has yet to make a final investment decision.

“The ExxonMobil and Chevron announcements were timed to coincide with next-generation ILSAC PCMO requirements, as original equipment manufacturers cannot promulgate specifications for which there are inadequate supplies,” Claxton said, adding that requirements for 13% NOACK volatility will force some existing Group III plants to increase the severity of their processes, which will reduce yields. “Thus ExxonMobil and Chevron decided it is time to make versus buy.” The Group III projects in Pascagoula and Baytown will without question reduce U.S. base oil imports, she said.

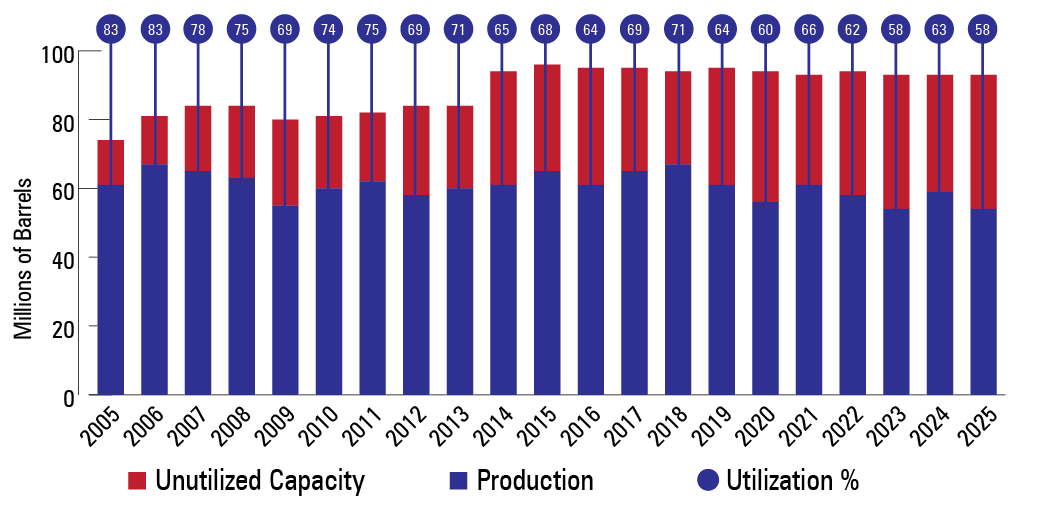

The other major trend in the U.S. base oil market has been decreasing plant utilization rates — partly due to the post-pandemic slip in production but owing more to increased capacity. From rates of 83% in 2005 and 2006, utilization declined fairly steadily, dropping below 70% three times between 2014 and 2019. In the first half of this year the rate was 62%, which would tie for lowest in the past two decades and be down from 67% last year. (Fig. 3)

Figure 3. U.S. Virgin Base Oil Plant Utilization

Source: U.S. Energy Information Administration

The drop in utilization may suggest a limit to how much base oil production refiners can shift to overseas sales. It also raises the prospect of plant closings. No U.S. virgin base oil plants have shuttered since Lyondell-Basell closed its plant in Houston in 2019.

Tim Sullivan is Executive Editor of Lubes’n’Greases. Contact him at Tim@LubesnGreases.com